ホルター心電図の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Holter ECG Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773270

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

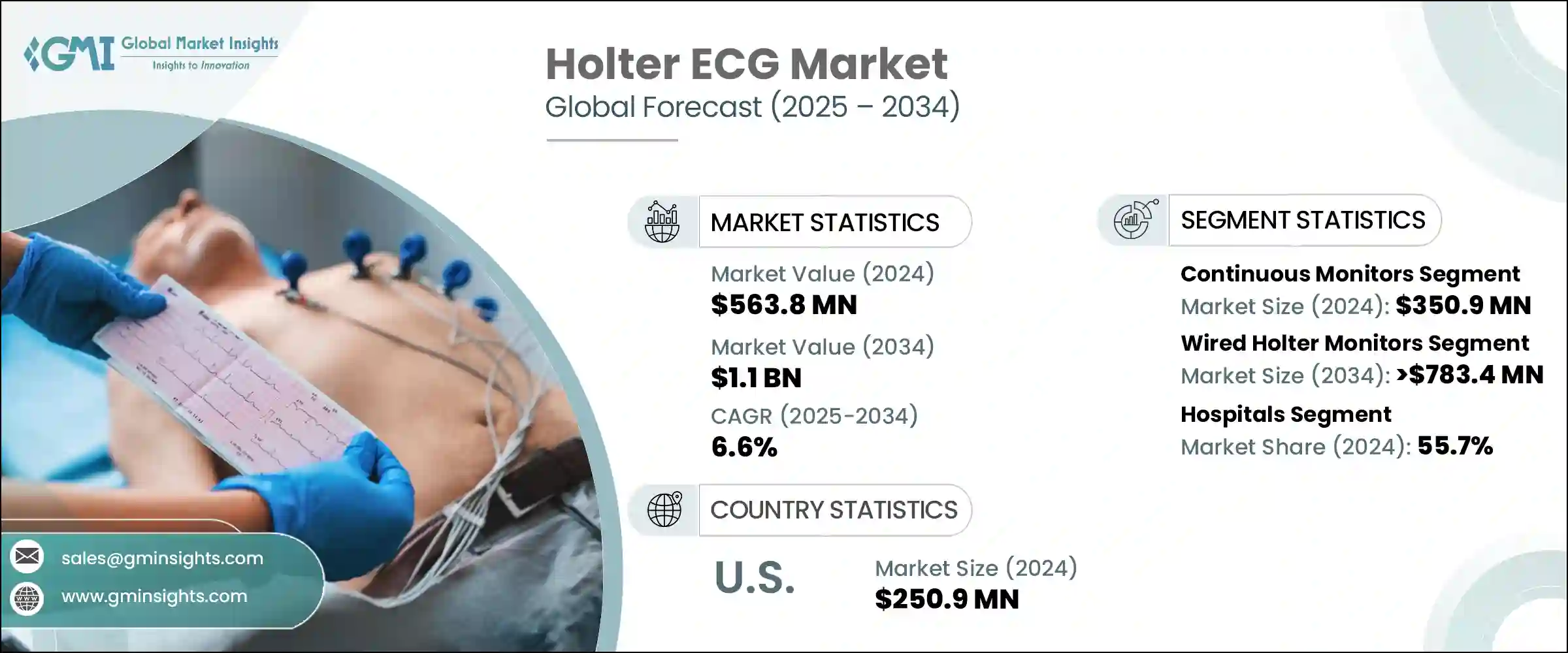

世界のホルター心電図市場は、2024年に5億6,380万米ドルと評価され、CAGR 6.6%で成長し、2034年には11億米ドルに達すると予測されています。

この成長は、心臓関連疾患の罹患率の上昇、侵襲性の低いモニタリング技術の受け入れ拡大、遠隔心臓診断の需要拡大が主な要因です。世界中で心血管疾患と診断される患者数が急増しており、高度な診断ソリューションに対するニーズが引き続き高まっています。心臓疾患は世界的な死亡率に大きく寄与しているため、早期かつ正確な診断が医療の重要な優先事項となっています。

ホルター心電図は、病院と自宅の両方で心臓の不整脈を特定するのに役立つため、需要は着実に増加しています。技術の進歩により、バッテリー寿命やワイヤレス機能が改善された小型で使いやすい機器が登場し、ヘルスケアプロバイダーと患者の双方にとって使い勝手が向上しています。このような技術向上により、間欠性不整脈の検出が容易になり、普及が進んでいます。遠隔患者モニタリングの動向とウェアラブル診断機器の増加により、積極的な健康管理に新たな扉が開かれました。より広範な意識とヘルスケア支出と相まって、これらの要因は世界市場全体でホルター心電図機器の需要を加速し続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 5億6,380万米ドル |

| 予測金額 | 11億米ドル |

| CAGR | 6.6% |

ホルター心電図は、心臓のリズムを一定期間追跡する小型の装着型システムです。電極は胸部と腹部の特定部位に取り付けられ、心臓の電気的活動を継続的に捕捉する携帯型モニターにリンクされます。新技術がヘルスケアの提供形態を変えるにつれ、これらの機器はクリニックだけでなく、家庭での心臓モニタリングセットアップにも急速に普及しています。センサー設計とマイクロエレクトロニクスの進歩により、衣服の下に隠れて目立たない、長時間装着可能なモニターが開発されています。このような特徴は、効果的な心拍評価に不可欠な患者の快適性とコンプライアンスを大幅に向上させます。これらの技術革新はまた、医師が捕捉しにくい不整脈を検出し、より効果的に治療を管理できるようサポートします。長時間使用機器の魅力は、使いやすさを向上させながら高いデータ品質を維持できる点にあり、現代の心臓治療において不可欠なツールとなっています。

2024年、連続モニターセグメントは3億5,090万米ドルをもたらし、市場を支配しました。連続ホルター心電図装置は、24~48時間、あるいはそれ以上の期間にわたって中断のないデータを提供し、医師が心臓の機能を観察するためのより詳細な情報を提供します。長時間の記録は、短時間の評価では気づかれないことが多い散発的なリズム障害を発見する可能性を高めます。その結果、多くのヘルスケア専門家は、徹底的な外来心臓評価にこの装置を好んでいます。不規則心拍の初期評価には、これらの装置が第一選択肢とされることが多くなっています。心臓専門医療と一般医療の両方で一貫して使用されているため、連続モニターは業界標準となっており、市場開拓に大きく貢献しています。

有線ホルターモニターは、2034年までのCAGRが6%で、市場評価額は7億8,340万米ドルに達すると予測されています。これらのシステムは、その堅牢な性能と一貫したデータ精度により、長い間心臓病学で信頼されてきました。メンテナンスの必要性が低く、病院のデジタルインフラとの互換性もあるため、多くのヘルスケア現場で定番となっています。これらの機器は、ECGソフトウェア、PACS、アーカイブネットワークなどの患者データシステムとシームレスに統合され、診断ワークフローを合理化します。医師は、データギャップの可能性を最小限に抑え、心拍リズムの問題をより明確に診断できる、その実証済みの信頼性に信頼を寄せています。より新しいワイヤレスオプションが登場する一方で、有線ソリューションは、その信頼性の高い出力と現在の病院IT環境への統合の容易さにより、依然として強い市場需要を維持しています。

米国のホルター心電図市場は、2024年に2億5,090万米ドル規模に達し、2025~2034年にかけてCAGR 5.5%で成長すると予測されています。特に高齢者層や慢性心疾患患者の導入が進んでいます。クラウドベースのプラットフォームとAIで強化されたデータ解釈ツールは、心疾患の遠隔監視方法に革命をもたらしました。これらのデジタル強化により、患者データのより良い管理と臨床転帰の改善が可能になります。加えて、有利な償還体系と現地企業による革新的製品の継続的な発売が、同国におけるホルター心電図の成長に寄与しています。予防医療への取り組み、特に心血管系の健康に焦点を当てた取り組みが市場の地位をさらに強化しています。

ホルター心電図市場で競合する主要企業には、GE HealthCare、SPACELABS HEALTHCARE、ScottCare、VIVALINK、PHILIPS、SCHILLER、iRHYTHM、FUKUDA、Bittium、Baxterなどがあります。ホルター心電図業界における地位を強化するため、主要企業は広範な製品革新、標的を絞った買収、技術統合などの戦略を実施しています。診断精度を高め、遠隔解析をサポートするために、AIを搭載したECG解釈ツールに投資している企業も多くなっています。また、ヘルスケアプロバイダーとの戦略的パートナーシップや提携を通じて、地理的なリーチを拡大しています。製品ポートフォリオも多様化しており、長時間装着型やワイヤレスのウェアラブルモニターなど、快適性や使いやすさに対する消費者の期待の高まりに対応できるように調整されています。さらにメーカーは、病院のITエコシステムとの互換性を合理化し、シームレスなデータ共有と解釈を実現するよう努めています。こうしたアプローチは、各ブランドが競争力を維持し、急速に進化する市場でより大きなシェアを獲得するのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 心臓疾患の有病率の増加

- 技術的進歩

- 低侵襲デバイスの採用拡大

- 遠隔患者心臓モニタリングへの関心の高まり

- 業界の潜在的リスク・課題

- 厳格な規制政策

- 高コストなホルター心電図

- 市場機会

- 遠隔患者モニタリング(RPM)・遠隔心臓病学の拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術・イノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格分析

- ギャップ分析

- ポーター分析

- 償還シナリオ

- PESTEL分析

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 地域別

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021~2034年

- 主要動向

- 連続モニター

- 間欠モニター

第6章 市場推計・予測:モダリティ別、2021~2034年

- 主要動向

- 有線ホルター心電図モニター

- 3誘導ホルター心電図モニター

- 12誘導ホルター心電図モニター

- その他

- ワイヤレスホルターモニター

第7章 市場推計・予測:最終用途別、2021~2034年

- 主要動向

- 病院

- 外来手術センター

- その他

第8章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Baxter

- Bittium

- FUKUDA

- GE HealthCare

- iRHYTHM

- PHILIPS

- SCHILLER

- ScottCare

- SPACELABS HEALTHCARE

- VIVALINK

目次

The Global Holter ECG Market was valued at USD 563.8 million in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 1.1 billion by 2034. This growth is largely fueled by the rising incidence of heart-related conditions, the increasing acceptance of less invasive monitoring technologies, and the growing demand for remote cardiac diagnostics. The surging number of individuals diagnosed with cardiovascular diseases worldwide continues to drive the need for sophisticated diagnostic solutions. With heart ailments contributing significantly to global mortality rates, early and accurate diagnosis has become a critical medical priority.

Demand for Holter ECGs is rising steadily as these devices help identify cardiac irregularities in both hospital and at-home settings. Technological progress has led to smaller, user-friendly devices with improved battery life and wireless features, enhancing usability for both healthcare providers and patients. These technological upgrades have made it easier to detect intermittent arrhythmia, increasing adoption. Remote patient monitoring trends and the availability of more wearable diagnostic devices have opened new doors for proactive health management. Combined with broader awareness and healthcare spending, these factors continue to accelerate the demand for Holter ECG devices across global markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $563.8 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 6.6% |

Holter ECGs are compact wearable systems that track heart rhythms for a defined duration. Electrodes are attached to specific parts of the chest and abdomen, linked to a portable monitor that continuously captures the heart's electrical activity. As newer technologies reshape healthcare delivery, these devices are seeing faster adoption not just in clinics but also in home-based cardiac monitoring setups. Advances in sensor design and microelectronics have led to discreet, long-wear monitors that remain hidden under clothing. These features significantly increase patient comfort and compliance, which are essential for effective cardiac rhythm assessment. These innovations also support physicians in detecting hard-to-catch arrhythmias and managing treatment more effectively. The appeal of extended-use devices lies in their ability to maintain high data quality while improving ease of use, making them an essential tool in modern cardiac care.

In 2024, the continuous monitoring segment brought in USD 350.9 million, dominating the Holter ECG landscape. Continuous Holter ECG devices deliver uninterrupted data for 24 to 48 hours or even longer, giving doctors an enhanced window to observe heart function. Their extended recording duration increases the likelihood of identifying sporadic rhythm disorders that would often go unnoticed in shorter evaluations. As a result, healthcare professionals often prefer them for thorough ambulatory cardiac assessment. These devices are often considered the primary option for initial evaluations of irregular heartbeat conditions. Due to their consistent use across both specialized cardiac practices and general medicine, continuous monitors have become an industry standard, contributing substantially to overall market development.

The wired Holter monitors segment is anticipated to witness a CAGR of 6% through 2034, reaching a market valuation of USD 783.4 million. These systems have long been trusted in cardiology for their robust performance and consistent data accuracy. Their low maintenance requirements and compatibility with digital hospital infrastructure make them a staple in many healthcare settings. These devices seamlessly integrate with patient data systems like ECG software, PACS, and archiving networks, which streamlines diagnostic workflows. Physicians rely on their proven reliability, which minimizes the chance of data gaps and ensures a clearer diagnosis of heart rhythm issues. While newer wireless options are emerging, wired solutions still retain strong market demand due to their dependable output and ease of integration into current hospital IT environments.

United States Holter ECG Market was worth USD 250.9 million in 2024 and is set to grow at a CAGR of 5.5% from 2025 to 2034. Adoption is especially robust among elderly populations and individuals living with chronic heart disease. Cloud-based platforms and AI-enhanced data interpretation tools have revolutionized the way cardiac conditions are monitored remotely. These digital enhancements allow for better management of patient data and improved clinical outcomes. Additionally, favorable reimbursement structures and the continuous launch of innovative products by local companies are contributing to the growth of Holter ECGs in the country. Preventive care initiatives, particularly those focusing on cardiovascular wellness, are further strengthening the market's position.

Major companies competing in the Holter ECG Market include GE HealthCare, SPACELABS HEALTHCARE, ScottCare, VIVALINK, PHILIPS, SCHILLER, iRHYTHM, FUKUDA, Bittium, and Baxter. To reinforce their position in the Holter ECG industry, key players are implementing strategies such as extensive product innovation, targeted acquisitions, and technology integration. Many are investing in AI-powered ECG interpretation tools to enhance diagnostic accuracy and support remote analysis. Companies are also expanding their geographic reach through strategic partnerships and collaborations with healthcare providers. Product portfolios are being diversified to include long-duration and wireless wearable monitors, tailored to meet rising consumer expectations for comfort and usability. Additionally, manufacturers are working to streamline compatibility with hospital IT ecosystems, ensuring seamless data sharing and interpretation. These approaches are helping brands to stay competitive and capture a larger share of this rapidly evolving market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Modality

- 2.2.4 End use

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of cardiac diseases

- 3.2.1.2 Technological advancements

- 3.2.1.3 Growing adoption of minimally invasive devices

- 3.2.1.4 Surging preference for remote patient cardiac monitoring

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory policies

- 3.2.2.2 High cost of the Holter ECG

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of remote patient monitoring (RPM) and telecardiology

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 Reimbursement scenario

- 3.10 PESTEL analysis

- 3.11 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 By region

- 4.3.1.1 North America

- 4.3.1.2 Europe

- 4.3.1.3 Asia Pacific

- 4.3.1 By region

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Continuous monitors

- 5.3 Intermittent monitors

Chapter 6 Market Estimates and Forecast, By Modality, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Wired Holter monitors

- 6.2.1 3 lead Holter monitors

- 6.2.2 12 lead Holter monitors

- 6.2.3 Other wired Holter monitors

- 6.3 Wireless Holter monitors

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Baxter

- 9.2 Bittium

- 9.3 FUKUDA

- 9.4 GE HealthCare

- 9.5 iRHYTHM

- 9.6 PHILIPS

- 9.7 SCHILLER

- 9.8 ScottCare

- 9.9 SPACELABS HEALTHCARE

- 9.10 VIVALINK

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日