中電力電気自動車用バスバーの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Medium Power Electric Vehicle Busbar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773268

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

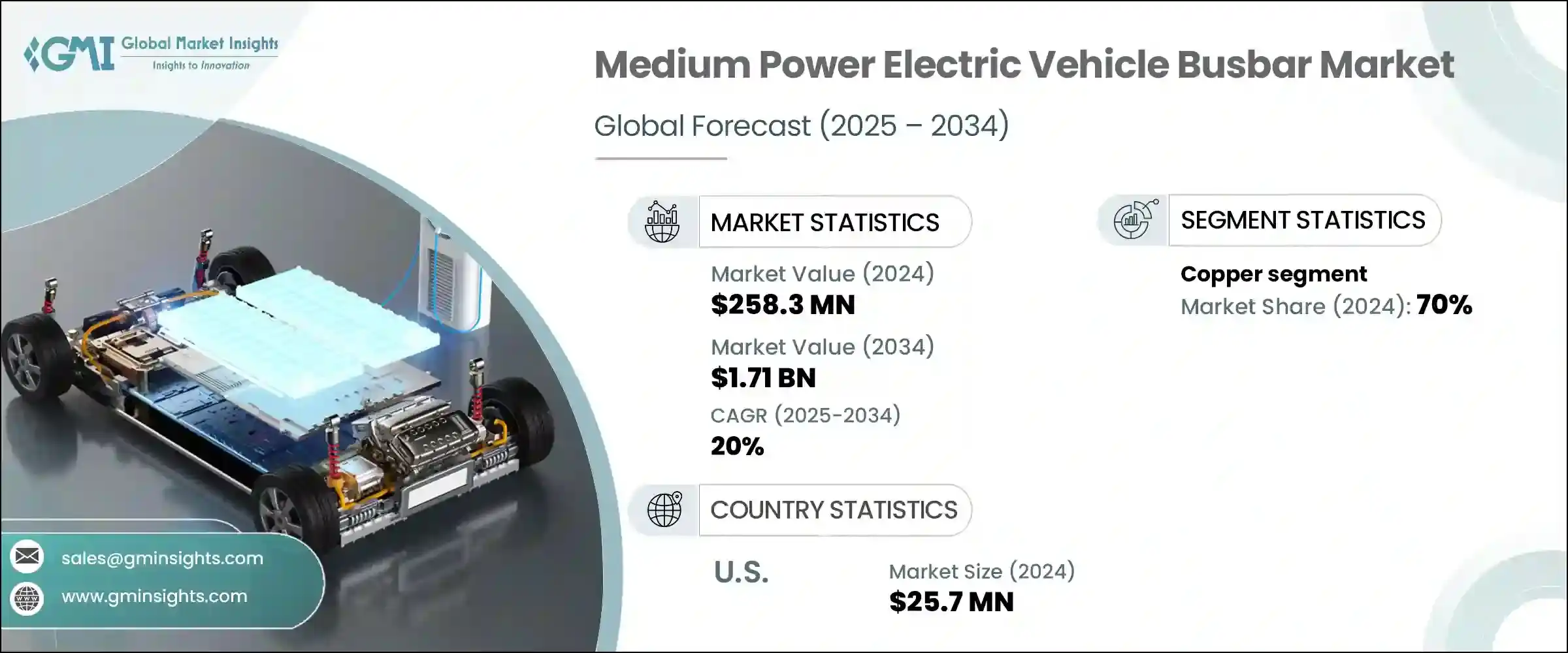

世界の中電力電気自動車用バスバーの市場規模は、2024年に2億5,830万米ドルとなり、CAGR20%で成長し、2034年には17億1,000万米ドルに達すると予測されています。

この目覚しい成長軌道は、電動モビリティへの投資の増加、有利な規制状況、配電技術の大幅な進歩によって後押しされています。電気自動車が主流になり続ける中、戦略的提携、材料科学における革新、進化する生産技術により、これらの自動車内でのエネルギー経路が再構築されつつあります。市場の勢いは、自動車の航続距離と性能を最適化するために調整された、軽量で高効率なシステムへのシフトとますます結びついています。

素材の進化は市場促進要因のひとつです。銅はその比類のない電気伝導性から、依然として主流ですが、かなりの重量を増すため、メーカーは代わりの材料を探すようになりました。コストを下げ、エネルギー効率を上げるために、アルミのような軽い素材が使われるようになってきました。先進的な複合材を使ったカスタムメイドのソリューションは、その優れた熱制御と機械的耐久性で人気を集めており、さまざまなEVアプリケーションのパフォーマンスを向上させています。さらに、カスタマイズされたバスバーシステムは、メーカーが材料の無駄を最小限に抑え、車両アーキテクチャを最適化するのに役立っています。スマートな技術統合、次世代生産ライン、進化するOEM仕様の融合により、バリューチェーン全体で市場拡大とイノベーションの新たな扉が開かれつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 2億5,830万米ドル |

| 予測金額 | 17億1,000万米ドル |

| CAGR | 20% |

2024年現在、中電力電気自動車用バスバー市場の銅セグメントは、その優れた導電性と熱管理によって70%のシェアを占めています。エネルギーロスを最小限に抑える銅の特性は、電気自動車のバッテリーの性能を高め、航続距離を延ばし、システムの完全性を維持するために不可欠なものです。これらの特性は、自動車の効率、安全性、電力供給のバランスを取ろうとする自動車メーカーにとって、引き続き重要です。

米国の2024年の市場規模は、2,570万米ドルとなりました。EVの普及を加速させる連邦および州主導の政策と、高度なグリッドインフラに対する需要の高まりが、メーカーの事業拡大を後押ししています。中電力バスバーは、EV配電ネットワークの最適化に不可欠であり、充電効率と負荷分散の両方を確保します。EVの生産規模が拡大するにつれ、信頼性が高く、コンパクトで熱効率の高いバスバーシステムに対する需要が急速に高まっています。

中電力電気自動車用バスバーの世界市場における主要企業には、Amphenol Corporation、Infineon Technologies AG、Blar Elettromeccanica SpA、Littelfuse, Inc.、Mersen SA、Siemens、EMS Group、Legrand、Rogers Corporation、Mitsubishi Electric Corporation、TE Connectivity、Schneider Electric、EAE Group、EG Electronics、Weidmuller Interface GmbH &Co.KGです。この分野の大手企業は、材料の革新、設計の最適化、世界的な製造の拡大を組み合わせることで、市場拡大を進めています。その多くは、次世代EVの進化する効率基準を満たすために、軽量で高性能な合金や複合材料の開発を優先しています。自動車メーカーやバッテリーメーカーとの戦略的合弁事業は、長期供給契約の確保に役立っています。企業はまた、複雑な車両固有のバスバーアセンブリをスケーラブルかつコスト効率よく生産できるように、自動化と精密ツールへの投資を強化しています。これと並行して、放熱、スマート診断、システム統合に重点を置いた研究開発活動を拡大し、OEMの要件に合わせた付加価値の高いソリューションを提供しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク・課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- 技術・イノベーションの情勢

第5章 市場規模・予測:材料別、2021~2034年

- 主要動向

- 銅

- アルミニウム

第6章 市場規模・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ノルウェー

- ドイツ

- フランス

- オランダ

- 英国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第7章 企業プロファイル

- Amphenol Corporation

- Brar Elettromeccanica SpA

- EAE Group

- EG Electronics

- EMS Group

- Infineon Technologies AG

- Legrand

- Littelfuse, Inc.

- Mersen SA

- Mitsubishi Electric Corporation

- Rogers Corporation

- Schneider Electric

- Siemens

- TE Connectivity

- Weidmuller Interface GmbH &Co. KG

目次

The Global Medium Power Electric Vehicle Busbar Market was valued at USD 258.3 million in 2024 and is estimated to grow at a CAGR of 20% to reach USD 1.71 billion by 2034. This impressive growth trajectory is being fueled by rising investments in electric mobility, favorable regulatory landscapes, and significant advancements in power distribution technologies. As electric vehicles continue gaining mainstream traction, strategic collaborations, innovations in material sciences, and evolving production technologies are reshaping how energy is routed within these vehicles. Market momentum is increasingly tied to the shift toward lightweight, high-efficiency systems tailored to optimize vehicle range and performance.

Material evolution is a key market driver. While copper remains dominant due to its unmatched electrical conductivity, it adds considerable weight-leading manufacturers to explore alternative materials. Lighter options like aluminum are now being integrated to reduce cost and improve energy efficiency. Custom-engineered solutions using advanced composites are gaining popularity for their superior thermal control and mechanical durability, offering a performance boost across various EV applications. Additionally, tailored busbar systems are helping manufacturers minimize material waste and optimize vehicle architecture. The convergence of smart technology integration, next-gen production lines, and evolving OEM specifications is opening new doors for market expansion and innovation across the value chain.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $258.3 Million |

| Forecast Value | $1.71 Billion |

| CAGR | 20% |

As of 2024, the copper segment in the medium-power electric vehicle busbar market held a 70% share due to its superior conductivity and thermal management. Its ability to minimize energy loss makes it vital for enhancing EV battery performance, ensuring better range, and maintaining system integrity. These characteristics remain critical for automakers striving to balance vehicle efficiency, safety, and power delivery.

United States Medium Power Electric Vehicle Busbar Market USD 25.7 million in 2024. Federal and state-led policies to accelerate EV adoption, coupled with rising demand for advanced grid infrastructure, are pushing manufacturers to scale up. Medium power busbars are essential in optimizing EV power distribution networks, ensuring both charging efficiency and load balancing. As EV production scales, the demand for reliable, compact, and heat-efficient busbar systems is increasing rapidly.

Key companies in the Global Medium Power Electric Vehicle Busbar Market include Amphenol Corporation, Infineon Technologies AG, Brar Elettromeccanica SpA, Littelfuse, Inc., Mersen SA, Siemens, EMS Group, Legrand, Rogers Corporation, Mitsubishi Electric Corporation, TE Connectivity, Schneider Electric, EAE Group, EG Electronics, and Weidmuller Interface GmbH & Co. KG. Leading players in this space are advancing their market footprint through a combination of material innovation, design optimization, and global manufacturing expansion. Many are prioritizing the development of lightweight, high-performance alloys and composites to meet the evolving efficiency standards of next-generation EVs. Strategic joint ventures with automakers and battery manufacturers are helping secure long-term supply agreements. Companies are also boosting investments in automation and precision tooling to enable scalable, cost-effective production of complex, vehicle-specific busbar assemblies. In parallel, they are expanding R&D efforts focused on heat dissipation, smart diagnostics, and system integration to deliver value-added solutions tailored to OEM requirements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Material, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Copper

- 5.3 Aluminum

Chapter 6 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.3 Europe

- 6.3.1 Norway

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Netherlands

- 6.3.5 UK

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.4.4 South Korea

- 6.4.5 Australia

- 6.5 Middle East & Africa

- 6.5.1 Saudi Arabia

- 6.5.2 UAE

- 6.5.3 South Africa

- 6.6 Latin America

- 6.6.1 Brazil

- 6.6.2 Argentina

Chapter 7 Company Profiles

- 7.1 Amphenol Corporation

- 7.2 Brar Elettromeccanica SpA

- 7.3 EAE Group

- 7.4 EG Electronics

- 7.5 EMS Group

- 7.6 Infineon Technologies AG

- 7.7 Legrand

- 7.8 Littelfuse, Inc.

- 7.9 Mersen SA

- 7.10 Mitsubishi Electric Corporation

- 7.11 Rogers Corporation

- 7.12 Schneider Electric

- 7.13 Siemens

- 7.14 TE Connectivity

- 7.15 Weidmuller Interface GmbH & Co. KG

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日