沈降シリカの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Precipitated Silica Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773265

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

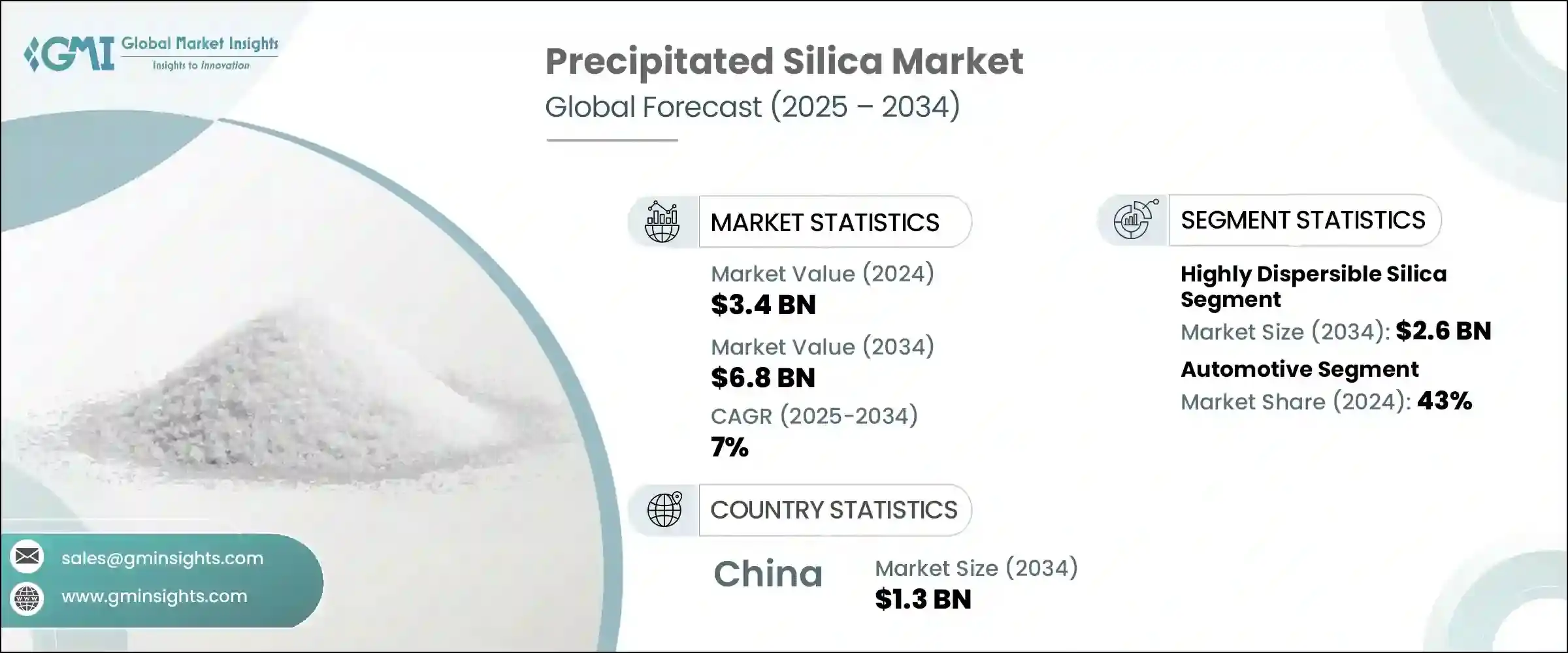

沈降シリカの世界市場は、2024年には34億米ドルと評価され、CAGR 7%で成長し、2034年には68億米ドルに達すると推定されています。

この市場成長の原動力となっているのは、沈降シリカのユニークな物理的・化学的特性であり、これによって様々な産業で汎用性の高い成分となっています。過去10年間、沈降シリカの需要は着実に伸びており、特にゴム、口腔ケア製品、コーティング剤における性能向上添加剤として注目されています。急速な都市化、自動車生産の増加、環境に優しい技術の重視といった継続的な動向が、市場を引き続き前進させています。

沈降シリカは、持続可能性の目標に沿いながら製品性能を向上させることができるため、継続的な採用が期待できます。アジア太平洋地域の新興経済諸国は、産業開拓の加速、自動車部門の拡大、消費財市場の活況により、この成長の大部分を後押ししています。中国やインドなどの国々は、大規模な消費者であるだけでなく、主要な生産拠点としても発展しており、この分野におけるこの地域の優位性をさらに確固たるものにしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 34億米ドル |

| 予測金額 | 68億米ドル |

| CAGR | 7% |

タイヤ・ゴム産業は、依然として沈降シリカ用途の要です。沈降シリカは、トラクションの強化、転がり抵抗の低減、燃費の向上において重要な役割を果たすため、特に電気自動車や高性能車向けの最新のタイヤ配合に欠かせないものとなっています。タイヤだけでなく、沈降シリカの用途は、医薬品、食品加工、パーソナルケア製品にも広がっており、固結防止剤、増粘剤、洗浄剤として活躍しています。

高分散性シリカ(HDS)は2024年に13億米ドルを占め、2034年には26億米ドルに達し、CAGR 7.1%で成長すると予想されています。この変種は、優れた補強能力とタイヤ用ゴムコンパウンドとの適合性で支持されています。HDSは転がり抵抗、ウェット・トラクション、燃費を大幅に向上させるため、特にハイブリッド車や電気自動車向けの環境に優しい高性能タイヤの製造に不可欠です。これは、世界の環境規制の高まりと、OEM(相手先ブランド製造)による低燃費製品の需要に合致しています。低排出ガス車と環境に優しいタイヤ・ソリューションへのシフトがHDSの採用を後押しし、将来のタイヤ技術における主要材料としての地位を強化しています。

2024年には、自動車分野が43%のシェアを占める。シリカは転がり抵抗の低減を通じてタイヤのグリップ力、耐摩耗性、燃費効率を向上させる。世界のエネルギー効率の高い低公害車の台頭により、メーカーは規制基準や顧客の嗜好を満たすために、シリカ強化タイヤの採用を増やしています。電気自動車やハイブリッド車の生産台数の急増は、トラクション強化と走行距離の延長を実現するために沈降シリカに大きく依存する高性能タイヤの需要を促進しています。自動車メーカーが持続可能で高品質なタイヤ素材を優先しているため、この動向は今後も続くと予想されます。

米国の沈降シリカ市場は2034年までCAGR 6.7%で成長します。この成長の主な要因はタイヤとゴムの用途であり、特に電気自動車向けのタイヤの販売が増加しています。さらに、パーソナルケア、医薬品、コーティング剤、接着剤への用途の多様化が、市場の裾野を広げる一助となっています。環境問題への関心の高まりと環境に優しい材料を推進する規制が、メーカーに持続可能なシリカ生産技術の採用を促しています。主要企業は、より環境に優しい材料やプロセスを革新するために、生産能力の拡大や研究開発に多額の投資を行っており、米国市場における持続可能性と長期的な技術革新に対する業界の明確な焦点が浮き彫りになっています。

沈降シリカ業界の主要企業には、PPG Industries、Evonik Industries、Oriental Silicas Corporation、W.R. Grace &Co.、Solvay S.A.などがあります。沈降シリカ市場での足場を固めるため、主要企業は多様な業界のニーズに合わせた特殊で持続可能なシリカグレードを開発し、製品ポートフォリオの拡大に注力しています。研究開発への重点的な投資により、環境に優しい生産方法と材料性能の向上に関する技術革新が可能になり、グリーンで効率的なソリューションに対する需要の高まりに応えています。戦略的パートナーシップや協力関係は、新たな地理的市場へのアクセスや流通網の拡大を目的として形成されています。各社はまた、技術サポート・サービスやカスタマイズ・ソリューションを通じて顧客との関係を強化し、より強固な顧客関係を育んでいます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品タイプ別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 高分散性シリカ

- 従来の沈降シリカ

- 表面処理シリカ

- 専門分野沈降シリカ

第6章 市場推計・予測:グレード別、2021年~2034年

- 主要動向

- 工業用グレード

- 食品グレード

- 医薬品グレード

- 化粧品グレード

- その他

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- ゴム

- タイヤの用途

- 乗用車用タイヤ

- 商用車用タイヤ

- オフロードタイヤ

- その他

- タイヤ以外のゴム用途

- 履物

- 工業用ゴム製品

- その他

- タイヤの用途

- 口腔ケア

- 歯磨き粉

- その他のオーラルケア製品

- 食品および飼料添加物

- 固結防止剤

- キャリア

- その他

- 産業用途

- 塗料とコーティング

- プラスチック

- 接着剤とシーラント

- その他

- パーソナルケアと化粧品

- スキンケア製品

- ヘアケア製品

- その他

- 医薬品

- 錠剤賦形剤

- その他

- 農業

- その他

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 自動車

- 消費財

- 食品と飲料

- ヘルスケアと医薬品

- 産業

- 建設

- 農業

- その他

第9章 市場推計・予測:製造工程別、2021年~2034年

- 主要動向

- 湿式プロセス

- 乾式プロセス

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第11章 企業プロファイル

- Anten Chemical Co., Ltd.

- Evonik Industries AG

- Gujarat Multi Gas Base Chemicals Pvt. Ltd.

- Huber Engineered Materials

- Madhu Silica Pvt. Ltd.

- Oriental Silicas Corporation

- PPG Industries, Inc.

- PQ Corporation

- Quechen Silicon Chemical Co., Ltd.

- Shandong Link Silica Co., Ltd.

- Solvay S.A.

- Tata Chemicals Ltd.

- Tosoh Silica Corporation

- W. R. Grace &Co.

- Wacker Chemie AG

目次

The Global Precipitated Silica Market was valued at USD 3.4 billion in 2024 and is estimated to grow at a CAGR of 7% to reach USD 6.8 billion by 2034. This market growth is driven by precipitated silica's unique physical and chemical properties, which make it a versatile ingredient across various industries. Over the past decade, its demand has steadily increased, particularly as a performance-enhancing additive in rubber, oral care products, and coatings. The ongoing trends of rapid urbanization, growing automotive production, and the increasing emphasis on environmentally friendly technologies continue to propel the market forward.

Precipitated silica's ability to improve product performance while aligning with sustainability goals positions it well for continued adoption. Emerging economies in the Asia Pacific region are fueling much of this growth, thanks to accelerated industrial development, expanding automotive sectors, and booming consumer goods markets. Countries such as China and India are not only large consumers but are also evolving as major production hubs, further solidifying the region's dominance in this sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.4 Billion |

| Forecast Value | $6.8 Billion |

| CAGR | 7% |

The tire and rubber industry remains the cornerstone of precipitated silica applications. Its vital role in enhancing traction, lowering rolling resistance, and boosting fuel efficiency has made it indispensable in modern tire formulations, especially for electric and high-performance vehicles. Beyond tires, precipitated silica's uses are broadening into pharmaceuticals, food processing, and personal care products, where it acts as an anti-caking agent, thickener, and detergent.

Highly dispersible silica (HDS) accounted for USD 1.3 billion in 2024 and is expected to reach USD 2.6 billion by 2034, growing at a CAGR of 7.1%. This variant is favored for its superior reinforcement capabilities and compatibility with tire rubber compounds. HDS significantly enhances rolling resistance, wet traction, and fuel economy, making it essential in the manufacture of green and high-performance tires, particularly for hybrid and electric vehicles. This aligns well with increasing global environmental regulations and original equipment manufacturers' (OEMs) demand for fuel-efficient products. The shift toward low-emission vehicles and eco-friendly tire solutions is boosting HDS adoption, reinforcing its position as a key material in future tire technologies.

In 2024, the automotive segment held a 43% share. This leadership is attributed to its widespread use in tire production, where silica improves tire grip, wear resistance, and fuel efficiency through reduced rolling resistance. With the global rise of energy-efficient, low-emission vehicles, manufacturers are increasingly incorporating silica-reinforced tires to meet regulatory standards and customer preferences. The surge in electric and hybrid vehicle production is driving demand for high-performance tires that depend heavily on precipitated silica to deliver enhanced traction and extended driving range. This trend is expected to continue as automotive manufacturers prioritize sustainable and high-quality tire materials.

U.S. Precipitated Silica Market will grow at a CAGR of 6.7% through 2034. This growth is primarily fueled by tire and rubber applications, especially with the rising sales of tires tailored for electric vehicles. Additionally, the diversification of applications into personal care, pharmaceuticals, coatings, and adhesives is helping broaden the market base. Increasing environmental concerns and regulations promoting eco-friendly materials are encouraging manufacturers to adopt sustainable silica production techniques. Leading companies are investing heavily in capacity expansion and research & development to innovate greener materials and processes, highlighting a clear industry focus on sustainability and long-term innovation in the U.S. market.

Key players in the Precipitated Silica Industry include PPG Industries, Evonik Industries, Oriental Silicas Corporation, W.R. Grace & Co., and Solvay S.A. To strengthen their foothold in the precipitated silica market, leading companies are focusing on expanding their product portfolios by developing specialized and sustainable silica grades tailored to diverse industry needs. Heavy investment in R&D is enabling innovation around eco-friendly production methods and enhanced material performance, which meets the growing demand for green and efficient solutions. Strategic partnerships and collaborations are being formed to access new geographic markets and broaden distribution networks. Companies are also enhancing customer engagement through technical support services and customized solutions, fostering stronger client relationships.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 End use industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1.1 Mergers & acquisitions

- 4.6.1.2 Partnerships & collaborations

- 4.6.1.3 New Product Launches

- 4.7 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Highly dispersible silica

- 5.3 Conventional precipitated silica

- 5.4 Surface-treated silica

- 5.5 Specialty precipitated silica

Chapter 6 Market Estimates and Forecast, By Grade, 2021 - 2034 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Industrial grade

- 6.3 Food Grade

- 6.4 Pharmaceutical grade

- 6.5 Cosmetic grade

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Rubber

- 7.2.1 Tire applications

- 7.2.1.1 Passenger car tires

- 7.2.1.2 Commercial vehicle tires

- 7.2.1.3 Off-road tires

- 7.2.1.4 Others

- 7.2.2 Non-tire rubber applications

- 7.2.2.1 Footwear

- 7.2.2.2 Industrial rubber products

- 7.2.2.3 Others

- 7.2.1 Tire applications

- 7.3 Oral care

- 7.3.1 Toothpaste

- 7.3.2 Other oral care products

- 7.4 Food and feed additives

- 7.4.1 Anti-caking agents

- 7.4.2 Carriers

- 7.4.3 Others

- 7.5 Industrial applications

- 7.5.1 Paints and coatings

- 7.5.2 Plastics

- 7.5.3 Adhesives and sealants

- 7.5.4 Others

- 7.6 Personal care and cosmetics

- 7.6.1 Skin care products

- 7.6.2 Hair care products

- 7.6.3 Others

- 7.7 Pharmaceuticals

- 7.7.1 Tablet excipients

- 7.7.2 Others

- 7.8 Agriculture

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Consumer goods

- 8.4 Food and beverage

- 8.5 Healthcare and pharmaceuticals

- 8.6 Industrial

- 8.7 Construction

- 8.8 Agriculture

- 8.9 Others

Chapter 9 Market Estimates and Forecast, By Manufacturing Process, 2021 - 2034 (USD Billion) (Tons)

- 9.1 Key trends

- 9.2 Wet process

- 9.3 Dry process

- 9.4 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Anten Chemical Co., Ltd.

- 11.2 Evonik Industries AG

- 11.3 Gujarat Multi Gas Base Chemicals Pvt. Ltd.

- 11.4 Huber Engineered Materials

- 11.5 Madhu Silica Pvt. Ltd.

- 11.6 Oriental Silicas Corporation

- 11.7 PPG Industries, Inc.

- 11.8 PQ Corporation

- 11.9 Quechen Silicon Chemical Co., Ltd.

- 11.10 Shandong Link Silica Co., Ltd.

- 11.11 Solvay S.A.

- 11.12 Tata Chemicals Ltd.

- 11.13 Tosoh Silica Corporation

- 11.14 W. R. Grace & Co.

- 11.15 Wacker Chemie AG

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日