電気自動車用断熱材の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Electric Vehicle Insulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773255

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

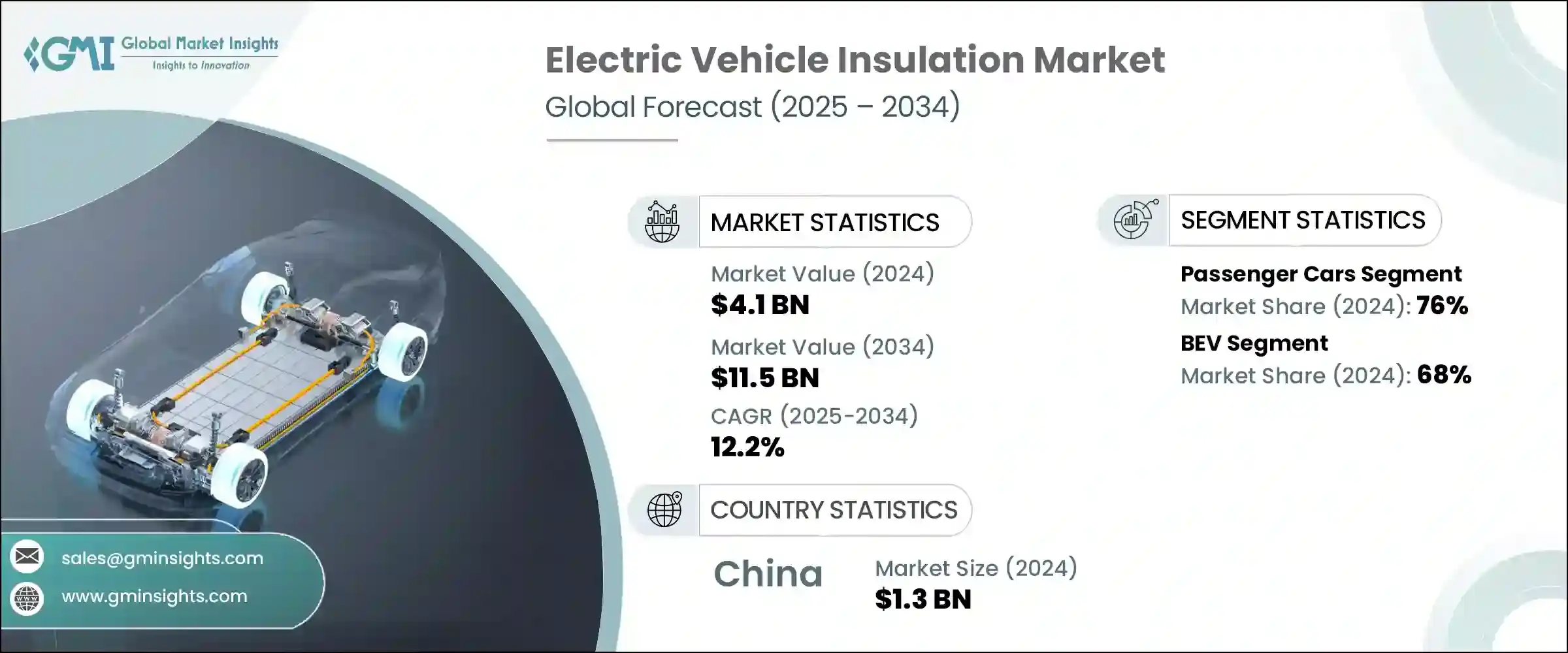

世界の電気自動車用断熱材市場は2024年に41億米ドルと評価され、CAGR 12.2%で成長し、2034年には115億米ドルに達すると予測されています。

電動モビリティへのシフトが進み、充電ネットワークが世界的に急拡大していることが、高度な断熱材の需要に大きな影響を与えています。EVが主流になるにつれて、断熱材は従来の自動車よりもはるかに中心的な役割を果たすようになっています。電気ドライブトレインの複雑化とコンパクト化に伴い、高熱に耐えるだけでなく、高電圧環境でも電気的分離を維持する材料が必要とされています。バッテリー温度の制御から電子部品のシールドに至るまで、絶縁は自動車の効率、信頼性、および長期的な安全性を高める上で不可欠となっています。

特にメーカーがバッテリーの高容量化と充電サイクルの高速化を推進する中、熱管理はEVエンジニアリングの中核的な優先事項となっています。このような要求を満たすため、市場では高い耐熱性と軽量設計の両方を提供する材料に強い関心が寄せられています。電気ドライブトレインは最大800Vの電圧で作動することが多いため、絶縁体は極端な熱勾配に耐えるだけでなく、繰り返される熱サイクルの下でも安定した性能を維持する必要があります。より多くの自動車メーカーが航続距離、耐久性、およびドライバー体験の向上を競う中、絶縁は単なる障壁としてではなく、バッテリーモジュール、電気モーター、およびパワーエレクトロニクス全体に統合された性能を実現するものとして設計されています。新しいEVプラットフォームの開発では、コンパクトな設計と効果的な熱・騒音制御のバランスがますます重視されるようになっており、断熱材は自動車の安全性と性能基準の中心に位置付けられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 41億米ドル |

| 予測金額 | 115億米ドル |

| CAGR | 12.2% |

推進力では、バッテリー電気自動車(BEV)が2024年に市場をリードし、世界シェアの約68%を占める。この分野は、2025年から2034年にかけてCAGR 13.1%以上で拡大すると予測されます。BEVは完全に電力に依存しているため、すべての高電圧部品と熱に敏感な部品にわたる包括的な絶縁の必要性が高まっています。BEVには大型のバッテリーパックが搭載され、運転中や充電中にかなりの熱が発生するため、安定した温度を維持し、エネルギー損失を防ぐことができる材料に対する需要は増加の一途をたどっています。BEVの絶縁は、電界を絶縁して電磁干渉を低減する役割も果たし、電気システムの効率と安全性をさらに向上させる。OEMがよりコンパクトで高エネルギー密度のバッテリー構成を模索する中、絶縁ソリューションは、緊密な統合、最小限の重量、高性能のために最適化されています。

製品別では、断熱材セグメントが2024年に圧倒的なシェアを占め、予測期間中もリードを維持すると予想されます。断熱材は、重要なシステム全体の温度均一性を管理するためにEVに不可欠です。過熱のリスクとエネルギー効率の低下は、車両の安全性とバッテリー寿命の両方を損なう可能性があるため、高性能の断熱材が広く採用されるようになりました。これらの材料は現在、バッテリーを熱蓄積から保護し、パワーエレクトロニクスの最適性能を維持し、過酷な運転条件下で乗客の安全を維持するための基本となっています。EV技術の成熟に伴い、断熱材は急速充電システムやますます小型化するバッテリーアセンブリからの熱需要の増加に対応しなければならないです。

地域別では、中国が2024年のアジア太平洋EV断熱材市場の約68.3%を占め、約13億米ドルの収益に貢献しました。同国は、高度に発達した現地サプライチェーンとEV技術への積極的な投資により、世界のEV生産の最前線に位置しています。その製造規模と旺盛な内需が相まって、中国は断熱材の技術革新と大量展開を推進する圧倒的な力となっています。この地域のメーカーが生産能力の拡大と製品性能の向上に注力する一方で、世界企業もまた、国内市場と輸出市場の両方をサポートするためにこの地域に投資しています。自動車のアーキテクチャが進化し、性能基準が厳しくなるにつれて、あらゆるタイプの電気自動車に対応する特殊な絶縁材料の需要が大幅に増加すると予想されます。

電気自動車用断熱材市場は、車両アーキテクチャの変遷とエネルギー効率と乗客の快適性に対する期待の高まりに対応して急速に変貌しています。EVがより複雑化するにつれて、絶縁システムは単に部品を保護するだけでなく、熱を積極的に管理し、ノイズを低減し、密集したパワートレイン環境内の電流を絶縁する必要があります。断熱材は、高電圧ドライブトレイン、モジュール式バッテリーシステム、静かなキャビン体験など、次世代のEV機能をサポートする上で重要な役割を果たすようになっています。現在では、エネルギー消費を改善し、走行距離を延ばすために、軽量で高耐久性の材料が開発されています。これらのソリューションは、EVの構造設計にシームレスに統合できるように設計されており、自動車メーカーが性能、安全性、規制目標を達成するのに役立っています。電動モビリティが世界中で加速するなか、断熱材は今後も持続可能で効率的な車両システムを実現する重要な要素であり続けると思われます。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 電気自動車の生産増加

- EV充電インフラの拡張

- 材料技術の進歩

- 政府のインセンティブと投資の増加

- 業界の潜在的リスク&課題

- 複雑なカスタマイズニーズ

- 統合熱管理ソリューションとの競合

- 市場機会

- バッテリーの安全性と防火に重点を置く

- 軽量素材の需要の高まり

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV

- 商用車

- 軽作業

- 中型

- ヘビーデューティー

- 二輪車

第6章 市場推計・予測:推進力別、2021年~2034年

- 主要動向

- 電気自動車

- PHEV

- ハイブリッド車

- 燃料電池自動車

第7章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 断熱材

- 防音

- 電気絶縁

- ハイブリッド

第8章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 熱インターフェース

- 発泡プラスチック

- セラミック材料

- グラスウール/グラスファイバー

- シリコンおよびゴムベース

- その他

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- バッテリーパックとハウジング

- 電気モーター

- パワーエレクトロニクス

- 客室

- ボンネットの下/熱管理システム

- 充電ポートとシステム

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- 3M

- Aerofoam(Hira Industries)

- Armacell International

- Autoneum

- BASF SE

- Covestro AG

- DuPont

- Flex

- ITW Formex

- Johns Manville(Berkshire Hathaway)

- L&L Products

- Morgan Advanced Materials

- Parker Hannifin

- Polymer Technologies

- Rogers Corporation

- Saint-Gobain

- Toray Industries

- UBE Corporation

- Unifrax(Alkegen)

- Zotefoams

目次

The Global Electric Vehicle Insulation Market was valued at USD 4.1 billion in 2024 and is estimated to grow at a CAGR of 12.2% to reach USD 11.5 billion by 2034. The increasing shift toward electric mobility and the global ramp-up of charging networks are significantly influencing the demand for advanced insulation materials. As EVs become more mainstream, insulation is playing a far more central role than in traditional vehicles-it is now critical to managing heat, ensuring electrical integrity, and supporting quieter cabin environments. The growing complexity and compactness of electric drivetrains require materials that not only resist high heat but also maintain electrical separation in high-voltage environments. From controlling battery temperatures to shielding electronic components, insulation is becoming essential in enhancing vehicle efficiency, reliability, and long-term safety.

Thermal management is a core priority in EV engineering, especially as manufacturers push for higher battery capacities and faster charging cycles. To meet these demands, the market is seeing strong interest in materials that offer both high thermal resistance and lightweight design. With electric drivetrains often operating at voltages up to 800V, insulation must not only withstand extreme thermal gradients but also maintain stable performance under repeated thermal cycling. As more automakers compete to improve range, durability, and driver experience, insulation is being engineered not just as a barrier but as a performance enabler integrated across battery modules, electric motors, and power electronics. The development of new EV platforms is increasingly focused on balancing compact design with effective heat and noise control, which places insulation at the center of vehicle safety and performance standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 12.2% |

In terms of propulsion, Battery Electric Vehicles (BEVs) led the market in 2024, accounting for approximately 68% of the global share. This segment is projected to expand at a CAGR of more than 13.1% from 2025 to 2034. BEVs rely entirely on electric power, which intensifies the need for comprehensive insulation across all high-voltage and thermally sensitive components. Since BEVs contain large battery packs and generate considerable heat during operation and charging, the demand for materials capable of maintaining stable temperatures and preventing energy loss continues to grow. Insulation in BEVs also serves to isolate electric fields and reduce electromagnetic interference, which further improves the efficiency and safety of electric systems. As OEMs explore more compact and high-energy-density battery configurations, insulation solutions are being optimized for tight integration, minimal weight, and high performance.

By product, the thermal insulation segment held the dominant share in 2024 and is expected to maintain its lead through the forecast period. Thermal insulation is essential in EVs to manage temperature uniformity across critical systems. Overheating risks and energy inefficiencies can compromise both vehicle safety and battery life, which has led to widespread adoption of high-performance thermal barriers. These materials are now fundamental to shielding batteries from heat buildup, preserving optimal performance of power electronics, and maintaining passenger safety under extreme operating conditions. As EV technology matures, thermal insulation must keep pace with rising thermal demands from fast-charging systems and increasingly compact battery assemblies.

Regionally, China represented about 68.3% of the Asia-Pacific EV insulation market in 2024, contributing approximately USD 1.3 billion in revenue. The country remains at the forefront of global EV production, with a highly developed local supply chain and aggressive investment in EV technologies. Its scale of manufacturing, combined with strong domestic demand, has made China a dominant force in driving innovation and mass deployment of insulation materials. While regional manufacturers are focused on expanding capacity and improving product performance, global companies are also investing in the region to support both local and export markets. As vehicle architectures evolve and performance standards grow more stringent, the demand for specialized insulation materials across all types of electric vehicles is expected to rise significantly.

The electric vehicle insulation market is transforming rapidly in response to shifting vehicle architectures and rising expectations for energy efficiency and passenger comfort. As EVs grow more complex, insulation systems must do more than just protect components-they must actively manage heat, reduce noise, and isolate electrical currents within tightly packed powertrain environments. Insulation has become instrumental in supporting next-generation EV features, including high-voltage drivetrains, modular battery systems, and quiet cabin experiences. Lightweight, high-durability materials are now being developed to improve energy use and extend driving range. These solutions are designed for seamless integration into the structural design of EVs, helping automakers meet performance, safety, and regulatory targets. With electric mobility accelerating worldwide, insulation will continue to be a key enabler of sustainable and efficient vehicle systems.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 – 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Product

- 2.2.5 Material

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising electric vehicle production

- 3.2.1.2 Expansion of EV charging infrastructure

- 3.2.1.3 Advancements in material technology

- 3.2.1.4 Rising government incentives and investments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex customization needs

- 3.2.2.2 Competition from integrated thermal management solutions

- 3.2.3 Market opportunities

- 3.2.3.1 Focus on battery safety and fire protection

- 3.2.3.2 Rising demand for light weight materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Sedans

- 5.2.2 Hatchbacks

- 5.2.3 SUV

- 5.3 Commercial vehicles

- 5.3.1 Light duty

- 5.3.2 Medium duty

- 5.3.3 Heavy duty

- 5.4 Two-wheelers

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 BEV

- 6.3 PHEV

- 6.4 HEV

- 6.5 FCEV

Chapter 7 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Thermal insulation

- 7.3 Acoustic insulation

- 7.4 Electric insulation

- 7.5 Hybrid

Chapter 8 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Thermal interface

- 8.3 Foamed plastics

- 8.4 Ceramic materials

- 8.5 Glass wool/Fiberglass

- 8.6 Silicon and Rubber-based

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Battery pack and housing

- 9.3 Electric motor

- 9.4 Power electronics

- 9.5 Passenger cabin

- 9.6 Under the hood/thermal management system

- 9.7 Charging port & system

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 3M

- 11.2 Aerofoam (Hira Industries)

- 11.3 Armacell International

- 11.4 Autoneum

- 11.5 BASF SE

- 11.6 Covestro AG

- 11.7 DuPont

- 11.8 Flex

- 11.9 ITW Formex

- 11.10 Johns Manville (Berkshire Hathaway)

- 11.11 L&L Products

- 11.12 Morgan Advanced Materials

- 11.13 Parker Hannifin

- 11.14 Polymer Technologies

- 11.15 Rogers Corporation

- 11.16 Saint-Gobain

- 11.17 Toray Industries

- 11.18 UBE Corporation

- 11.19 Unifrax (Alkegen)

- 11.20 Zotefoams

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日