遠心送風機の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Centrifugal Blower Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 300 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773249

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

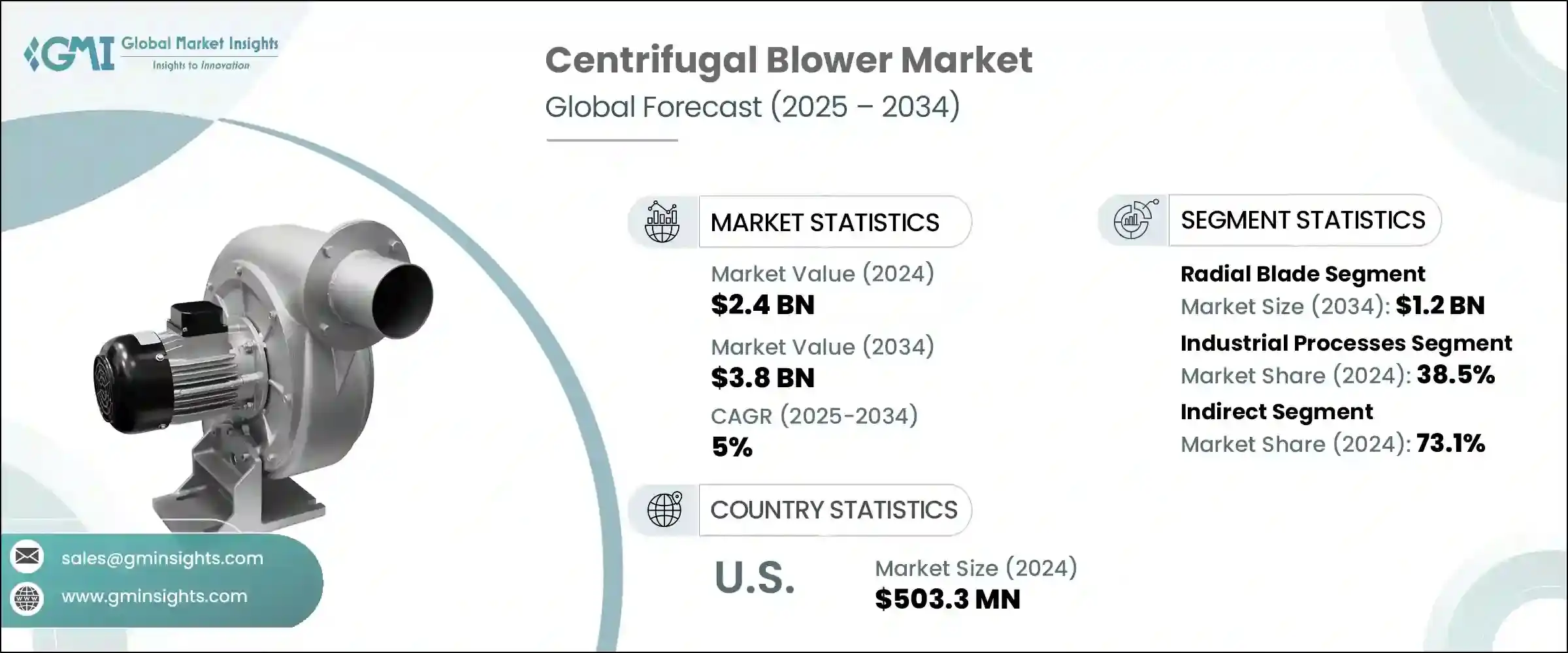

世界の遠心送風機の市場規模は、2024年に24億米ドルとなり、CAGR 5%で成長し、2034年には38億米ドルに達すると予測されています。

市場の成長軌道は、自動車、HVAC、化学処理、発電などの産業からの需要増加と密接に結びついています。遠心送風機がは、換気、冷却、空気輸送システムなど、空気やガスを移動させるシステムの主要部品です。

これらの送風機の採用が急増しているのは、エネルギー効率の向上、環境への影響の低減、運転寿命の延長を実現する技術革新によるものです。スマート技術で設計された先進的な送風機モデルの導入は、特に自動化、生産性、データ主導の効率性を重視するインダストリー4.0に沿った近代的な製造イニシアチブをサポートしています。産業界がエネルギー消費と二酸化炭素排出量を削減するソリューションを積極的に模索している中、エネルギー効率の高い送風機は事業戦略の中心となっています。このような送風機は、産業の持続可能性目標をサポートするだけでなく、エネルギー集約型部門における光熱費の削減にも役立ちます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 24億米ドル |

| 予測金額 | 38億米ドル |

| CAGR | 5% |

鉱業・発電などの分野では、遠心送風機の役割は気流制御にとどまらず、重要な安全機能にも及んでいます。遠心送風機は、危険な作業環境における清浄な空気ゾーンの維持や、繊細な機器のスムーズな動作の確保に役立っています。規制圧力が高まり、職場の安全や環境基準に対する意識が高まる中、信頼性と耐久性に優れた送風機に対する需要は加速しています。企業がコンプライアンス要件を満たし、リスク軽減戦略の強化に努める中で、遠心送風機は中核業務への統合が進んでいます。

飲食品分野も、遠心送風機の採用に大きく貢献しています。これらのシステムは、食品加工環境において極めて重要な高レベルの衛生をサポートします。包装・加工食品に対する世界の需要が高まり続ける中、加工ラインにおける空気ろ過と臭気制御システムのニーズが高まっています。遠心送風機は正確なエアフロー制御が可能で、食品製造に必要なクリーンルーム環境や空気清浄システムのサポートに最適です。食品製造における自動化とプログラム可能なシステムの継続的な拡大も、高度な送風機構成の市場を後押ししています。

タイプ別では、ラジアルブレード遠心送風機が2024年に7億8,850万米ドルの評価額で市場を席巻し、2034年には12億米ドルに達すると推定されます。このセグメントは、効果的なエアフロー性能、さまざまな分野への適応性、エネルギー消費を最適化する設計の継続的な改善により、依然としてトップの選択肢となっています。運転性能と省エネルギーを両立させるソリューションに対する産業界の要求が高まる中、ラジアルブレード構成は、用途を問わず支持を集め続けています。

用途別では、産業プロセスで使用される遠心送風機がが2024年の世界市場シェアの約38.5%を占め、2025~2034年までのCAGRは5.4%と予測されています。これらの送風機は、空気燃焼、マテリアルハンドリング、排気システムなど、いくつかの重要な機能に不可欠です。過酷な環境に耐え、安定した性能を発揮する送風機は、製造、精製、重工業に不可欠です。プロセス効率の向上とダウンタイムの短縮が重視されるようになったことで、産業用システムでの遠心送風機がの採用が広がっています。

流通チャネル別では、2024年には間接販売チャネルが約73.1%と圧倒的なシェアを占めています。販売代理店は市場拡大において極めて重要な役割を果たしており、メーカーに幅広い顧客層へのアクセスを提供し、地域間での製品の迅速な供給を可能にしています。こうした仲介業者は、販売後のサポート、技術支援、製品サービスを提供することが多く、顧客満足度を高め、リピーターを増やしています。メーカーと流通パートナーとの戦略的協力関係が市場を形成し続けており、この分野での間接販売の強さを強化しています。

地域別では、米国は2024年に5億330万米ドルの市場価値を記録し、予測期間中はCAGR 4.5%で成長すると予想されます。同国には製造業、石油化学、HVACなどの産業エコシステムが確立されており、遠心送風機需要の強固な基盤となっています。成熟した物流インフラと広範な流通網を利用することで、高度な送風機システムが全国で容易に入手できるようになり、国内消費の着実な増加を支えています。

遠心送風機市場には、著名な世界メーカーと地域に特化したサプライヤーが混在しています。同分野の主要企業には、Airmake Cooling Systems、Aerotech Equipment、Alfotech Fans、Atlas Copco、Atlantic Blowers LLC、Chuan-Fan Electric Co.Ltd.、Colfax Corporation、CLEANTEK、Elektror Airsystems、HIS Blower、Illinois Blower Inc、Ltd.、Kaeser Kompressoren、The New York Blower Company、Shandong Huadong Blower Co., Ltd.、The Spencer Turbine Company、Trimech India、Vishwakarma Air Systemsなどがあります。競合情勢は適度に細分化されており、継続的な技術革新と競争力のある価格戦略を後押ししています。技術的要件や設備投資による参入障壁はあるものの、新規参入企業や、特注品や地域特化型ソリューションに注力するニッチプレーヤーには好都合な環境が続いています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク・課題

- 機会

- 成長可能性分析

- 将来の市場動向

- 技術・イノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- タイプ別

- 規制の枠組み

- 規格・認証

- 環境規制

- 輸出入規制

- 貿易統計

- 主要輸入国

- 主要輸出国

- ポーターのファイブフォース分析

- PESTEL分析

- 消費者行動分析

- 購入パターン

- 嗜好分析

- 消費者行動の地域差

- eコマースが購買決定に与える影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021~2034年

- 主要動向

- ラジアルブレード

- 前傾型

- 後傾型

- 斜流型

- 軸流型

- 多段型

- その他

第6章 市場推計・予測:駆動機構別、2021~2034年

- 主要動向

- ダイレクト駆動

- ベルト駆動

第7章 市場推計・予測:圧力別、2021~2034年

- 主要動向

- 高圧

- 中圧

- 低圧

第8章 市場推計・予測:用途別、2021~2034年

- 主要動向

- HVAC

- 産業プロセス

- 発電

- 医薬品

- 食品加工

- 鉱業

- 農業

- その他

第9章 市場推計・予測:流通チャネル別、2021~2034年

- 主要動向

- 直接販売

- 間接販売

第10章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- マレーシア

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Aerotech Equipments and Projects Pvt. Ltd

- Airmake Cooling Systems

- Alfotech Fans

- Atlantic Blowers LLC

- Atlas Copco

- Chuan-Fan Electric Co., Ltd.

- CLEANTEK

- Colfax Corporation

- Elektror Airsystems

- EVG Engicon Airtech Pvt. Ltd.

- HIS Blower

- Illinois Blower Inc.

- Kaeser kompressoren

- Shandong Huadong Blower Co., Ltd.

- The New York Blower Company

- The Spencer Turbine Company

- Trimech India

- Vishwakarma Air Systems

目次

The Global Centrifugal Blower Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 5% to reach USD 3.8 billion by 2034. The market's growth trajectory is closely tied to rising demand from industries such as automotive, HVAC, chemical processing, and power generation. Centrifugal blowers are key components in systems that move air and gas, including ventilation, cooling, and pneumatic conveying systems.

The surge in the adoption of these blowers is largely attributed to innovations that enhance energy efficiency, reduce environmental impact, and extend operational life. The introduction of advanced blower models designed with smart technologies is supporting modern manufacturing initiatives, particularly those aligned with Industry 4.0, which emphasize automation, productivity, and data-driven efficiency. With industries actively seeking solutions to reduce their energy consumption and carbon footprint, energy-efficient blowers have become central to operational strategies. These blowers not only support industrial sustainability goals but also help lower utility expenses in energy-intensive sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $3.8 Billion |

| CAGR | 5% |

In sectors like mining and power generation, the role of centrifugal blowers extends beyond airflow control to include critical safety functions. They help maintain clean air zones in hazardous work environments and ensure the smooth operation of sensitive equipment. With increasing regulatory pressures and rising awareness about workplace safety and environmental standards, the demand for reliable and durable blowers is accelerating. Centrifugal blowers are being increasingly integrated into core operations as companies strive to meet compliance requirements and enhance risk mitigation strategies.

The food and beverage sector is another key contributor to centrifugal blower adoption. These systems support high levels of sanitation and hygiene, which are crucial in food processing environments. As global demand for packaged and processed foods continues to rise, the need for air filtration and odor control systems within processing lines is growing. Centrifugal blowers offer precise airflow control, making them ideal for supporting cleanroom environments and air purification systems required in food manufacturing. The continued expansion of automation and programmable systems within food production is also boosting the market for advanced blower configurations.

By type, radial blade centrifugal blowers dominated the market in 2024 with a valuation of USD 788.5 million and are estimated to reach USD 1.2 billion by 2034. This segment remains the top choice due to its effective airflow performance, adaptability across various sectors, and ongoing improvements in design that optimize energy consumption. As industries increasingly demand solutions that combine operational performance with energy savings, the radial blade configuration continues to gain traction across applications.

In terms of application, centrifugal blowers used in industrial processes accounted for approximately 38.5% of the global market share in 2024 and are projected to register a CAGR of 5.4% from 2025 to 2034. These blowers are vital to several key functions, such as air combustion, material handling, and exhaust systems. Their ability to withstand harsh environments and deliver consistent performance makes them indispensable in manufacturing, refining, and heavy industrial operations. The growing emphasis on improving process efficiency and reducing downtime has led to the wider adoption of centrifugal blowers in industrial systems.

Looking at the distribution landscape, the indirect sales channel held a dominant share of nearly 73.1% in 2024. Distributors play a pivotal role in market expansion, offering manufacturers access to a wider customer base and enabling faster product availability across regions. These intermediaries often provide post-sale support, technical assistance, and product servicing, which enhances customer satisfaction and fosters repeat business. Strategic collaborations between manufacturers and distribution partners continue to shape the market, reinforcing the strength of indirect sales in this sector.

Regionally, the United States recorded a market value of USD 503.3 million in 2024 and is expected to grow at a CAGR of 4.5% over the forecast period. The country's well-established industrial ecosystem, which includes manufacturing, petrochemical, and HVAC sectors, provides a solid foundation for centrifugal blower demand. Access to a mature logistics infrastructure and a broad network of distribution channels ensures that advanced blower systems are readily available nationwide, supporting a steady uptick in domestic consumption.

The centrifugal blower market features a mix of prominent global manufacturers and region-focused suppliers. Key players in the space include Airmake Cooling Systems, Aerotech Equipment, Alfotech Fans, Atlas Copco, Atlantic Blowers LLC, Chuan-Fan Electric Co., Ltd., Colfax Corporation, CLEANTEK, Elektror Airsystems, HIS Blower, Illinois Blower Inc., EVG Engicon Airtech Pvt. Ltd., Kaeser Kompressoren, The New York Blower Company, Shandong Huadong Blower Co., Ltd., The Spencer Turbine Company, Trimech India, and Vishwakarma Air Systems. The competitive landscape remains moderately fragmented, which encourages ongoing innovation and competitive pricing strategies. While some entry barriers exist due to technical requirements and capital investments, the environment remains conducive for new entrants and niche players focusing on custom or region-specific solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Driving mechanism

- 2.2.4 Pressure

- 2.2.5 Application

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's five forces analysis

- 3.10 PESTEL analysis

- 3.11 Consumer behavior analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behavior

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New Product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Radial blade

- 5.3 Forward-curved

- 5.4 Backwards curved

- 5.5 Mixed flow

- 5.6 Axial flow

- 5.7 Multi-stage

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Drive Mechanism, 2021 - 2034, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Direct drive

- 6.3 Belt drive

Chapter 7 Market Estimates & Forecast, By Pressure, 2021 - 2034, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 High

- 7.3 Medium

- 7.4 Low

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 HVAC

- 8.3 Industrial processes

- 8.4 Power generation

- 8.5 Pharmaceutical

- 8.6 Food processing

- 8.7 Mining

- 8.8 Agriculture

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 11.1 Aerotech Equipments and Projects Pvt. Ltd

- 11.2 Airmake Cooling Systems

- 11.3 Alfotech Fans

- 11.4 Atlantic Blowers LLC

- 11.5 Atlas Copco

- 11.6 Chuan-Fan Electric Co., Ltd.

- 11.7 CLEANTEK

- 11.8 Colfax Corporation

- 11.9 Elektror Airsystems

- 11.10 EVG Engicon Airtech Pvt. Ltd.

- 11.11 HIS Blower

- 11.12 Illinois Blower Inc.

- 11.13 Kaeser kompressoren

- 11.14 Shandong Huadong Blower Co., Ltd.

- 11.15 The New York Blower Company

- 11.16 The Spencer Turbine Company

- 11.17 Trimech India

- 11.18 Vishwakarma Air Systems

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 300 Pages

- 納期

- 2~3営業日