マタニティ用品の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Maternity Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773248

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

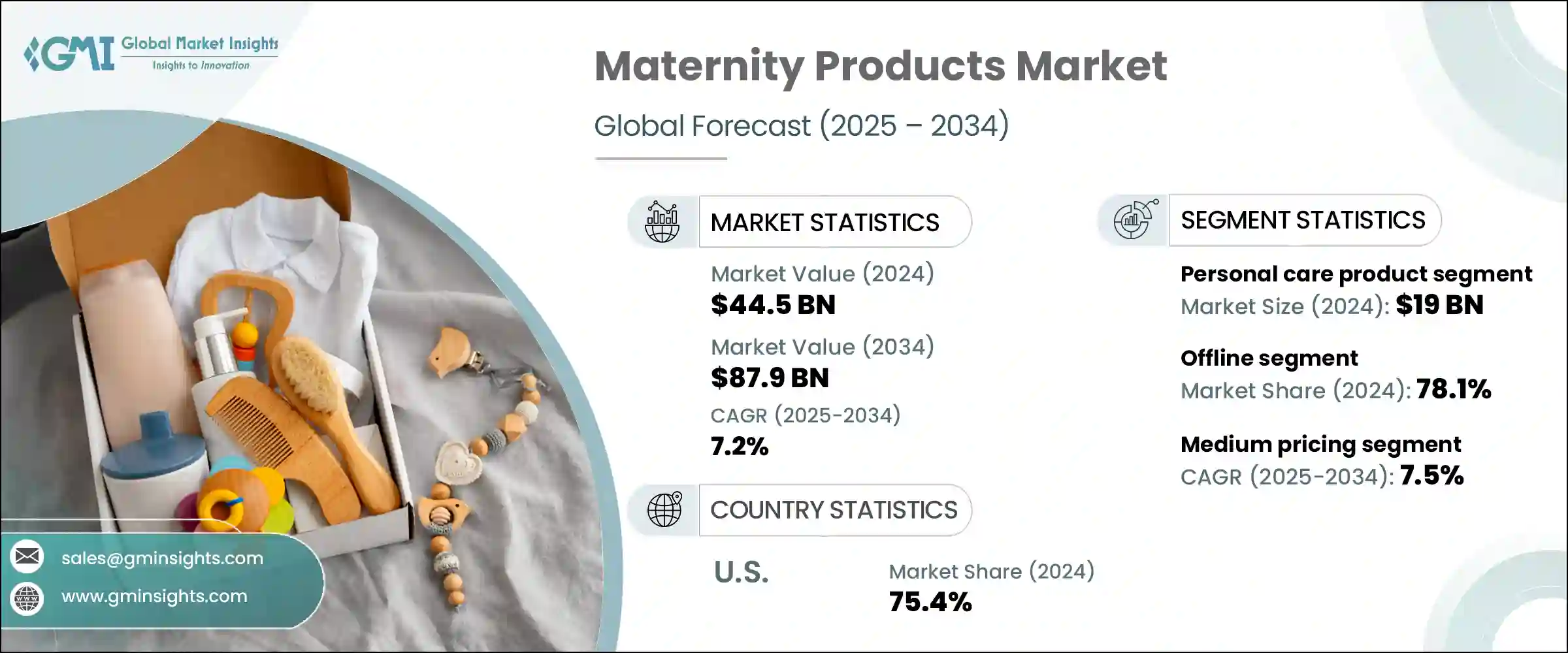

世界のマタニティ用品市場は、2024年には445億米ドルとなり、CAGR 7.2%で成長し、2034年には879億米ドルに達すると推定されています。

同市場は、妊産婦の健康に対する保護者の意識の高まりに後押しされ、力強い勢いを見せています。ヘルスケアへのアクセスの改善、消費者の期待の進化、政府の支援政策の影響を受け、妊産婦の健康への取り組み方に顕著な変化が見られます。主な成長要因のひとつは、妊娠中および妊娠後の心身の健康に対する消費者の関心が高まっていることです。妊産婦ケアにおけるテクノロジーの統合は成長を加速させており、デジタルツールはパーソナライズされた健康追跡、食事計画、活動推奨を提供します。

遠隔医療サービスによる遠隔診察も、妊産婦ケアへのアクセシビリティを向上させています。政府や保健機関は、既存のケア格差に対処するため、妊産婦向けデジタルソリューションを推進しています。可処分所得が世界的に増加するにつれて、両親は先進的で快適かつ安全なマタニティ用品に投資する傾向が強まっています。オンライン小売プラットフォームの急増も、アクセシビリティと利便性を一変させました。eコマースは、プライバシーの保護、製品の選択肢の拡大、製品比較の可能性により、母親としての成長をサポートする質の高いソリューションを求める、テクノロジーに精通した現代の親たちを魅了し続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 445億米ドル |

| 予測金額 | 879億米ドル |

| CAGR | 7.2% |

2024年、パーソナルケア製品は190億米ドルを生み出し、2034年までにCAGR 7.4%で成長すると予測されます。妊娠中や産後の女性の間でスキンケアや健康に対する意識が高まっていることが主因です。肌荒れ、色素沈着、妊娠線などの懸念が、クリーム、ジェル、オーガニックスキンケアラインなど幅広いソリューションへの需要を促しています。女性の社会進出が進んでいることに加え、自然で安全かつ高性能の製品を好む傾向が、この分野の成長を引き続き後押ししています。母親たちは利便性と効果の両方を優先しており、信頼できるエココンシャスなブランドへのシフトを支えています。

オフライン小売チャネルセグメントは2024年に78.1%のシェアを占め、2025~2034年のCAGRは7.1%を維持すると予測されます。実店舗が支配的な地位を占めているのは、製品を実際に手に取って評価できるからです。妊娠中の消費者は、購入前に商品に触れ、テストし、評価する機会を好みます。販売員は、顧客一人ひとりのニーズに基づいて案内することで付加価値を高め、ショッピング体験を向上させ、ブランドの信頼を築きました。また、オフラインのフォーマットは、特にウェアラブル、健康機器、スキンケアソリューションを購入する際に、より厳選された製品の比較をサポートします。

米国マタニティ用品市場は2024年に75.4%のシェアを占め、2025年から2034年にかけてCAGR 7.1%で成長する見込みです。米国の消費者は妊産婦の健康に対する意識が高く、安全性と革新性の両方を優先しています。働く母親の増加と所得水準の上昇が、プレミアム品質のマタニティ用品への支出拡大に寄与しています。さらに、持続可能で技術主導のイノベーションに焦点を当てた製品開発が、消費者の強い関心を集めています。市場の成熟と健康増進技術の急速な普及により、米国は引き続きこの分野のリーダーとして位置づけられています。

世界のマタニティ用品市場の主要企業には、Gap、Motherhood、H&M Mama、Seraphine、JoJo Maman Bebe、A Pea in the Pod、PinkBlush、HATCH、Old Navy、Cake、Frida、ASOS、Destination、Isabella Oliver、The Moms Co.などがあります。マタニティ用品業界の企業は、革新性、品質、オムニチャネル小売戦略に注力し、存在感を拡大しています。多くのブランドは、便利で控えめなショッピング体験への高まる需要に応えるため、デジタル店頭を強化し、eコマースチャネルを最適化しています。健康志向の消費者層に対応するため、オーガニック、皮膚科学的テスト済み、持続可能性認証製品など、製品ポートフォリオの多様化が進んでいます。ヘルスケア専門家やインフルエンサーとのコラボレーションは、ブランドの信頼性と消費者のエンゲージメントを高めるのに役立っています。パーソナライズされたカウンセリングサービスや厳選されたディスプレイにより、店舗での体験が向上しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 機会

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- タイプ別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

- 消費者行動分析

- 購入パターン

- 嗜好分析

- 消費者行動の地域差

- eコマースが購買決定に与える影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ航空

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021 -2034

- 主要動向

- マタニティウェア

- パーソナルケア製品

- 栄養補助食品

- マタニティアクセサリー

第6章 市場推計・予測:用途別、2021 -2034

- 主要動向

- 妊娠中

- 出産後

第7章 市場推計・予測:価格別、2021 -2034

- 主要動向

- 低

- 中

- 高

第8章 市場推計・予測:流通チャネル別、2021 -2034

- 主要動向

- オンライン販売

- eコマース

- 企業ウェブサイト

- オフライン販売

- 卸売業者/販売業者

- ハイパーマーケット/スーパーマーケット

- 専門店

- その他(セレクトショップなど)

第9章 市場推計・予測:地域別、2021 -2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第10章 企業プロファイル

- A Pea in the Pod

- ASOS

- Cake

- Destination

- Frida

- Gap

- H&M Mama

- Hatch

- Isabella Oliver

- JoJo Maman Bebe

- Motherhood

- Old Navy

- Pink Blush

- Seraphine

- The Moms Co.

目次

The Global Maternity Products Market was valued at USD 44.5 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 87.9 billion by 2034. The market is experiencing strong momentum, driven by rising awareness among parents regarding maternal wellness. There's a notable shift in how maternal health is approached, influenced by better healthcare access, evolving consumer expectations, and supportive government policies. One of the primary growth factors is increased consumer focus on both mental and physical health during and after pregnancy. Technology integration in maternal care is accelerating growth, with digital tools providing personalized health tracking, diet planning, and activity recommendations.

Remote consultations through telehealth services are also improving maternity care accessibility. Governments and health organizations are promoting digital maternal solutions to address existing care gaps. As disposable incomes rise globally, parents are more inclined to invest in advanced, comfortable, and safe maternity products. The surge in online retail platforms has also transformed accessibility and convenience. With greater privacy, wider product choices, and the ability to compare offerings, e-commerce continues to attract modern, tech-savvy parents who are looking for quality solutions to support the motherhood journey.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $44.5 Billion |

| Forecast Value | $87.9 Billion |

| CAGR | 7.2% |

In 2024, personal care products generated USD 19 billion and are forecasted to grow at a CAGR of 7.4% by 2034. These items dominate the global market, largely due to growing awareness of skincare and wellness among pregnant and postpartum women. Concerns such as skin irritation, pigmentation, and stretch marks are prompting demand for a broad spectrum of solutions, including creams, gels, and organic skincare lines. Increasing participation of women in the workforce, along with a preference for natural, safe, and high-performing products, continues to fuel growth in this segment. Mothers are prioritizing both convenience and effectiveness, supporting a shift toward trusted and eco-conscious brands.

The offline retail channels segment accounted for 78.1% share in 2024 and is projected to maintain a CAGR of 7.1% during 2025-2034. Physical retail stores hold a dominant position because they offer hands-on product assessment. Pregnant consumers prefer the opportunity to touch, test, and evaluate items before making a purchase-particularly when it comes to comfort, fit, quality, and size. Sales personnel add value by guiding customers based on their individual needs, which improves the shopping experience and builds brand trust. Offline formats also support a more curated product comparison, especially when purchasing wearables, health devices, or skin care solutions.

United States Maternity Products Market held 75.4% share in 2024 and is on track to grow at a CAGR of 7.1% during 2025-2034. Consumers in the US are highly attuned to maternal health and prioritize both safety and innovation. An increase in working mothers and rising income levels are contributing to greater spending on premium-quality maternity products. Additionally, product development focused on sustainable and tech-driven innovations is gaining strong consumer interest. The market's maturity and fast adoption of health-enhancing technologies continue to position the US as a leader in this space.

Leading companies in the Global Maternity Products Market include Gap, Motherhood, H&M Mama, Seraphine, JoJo Maman Bebe, A Pea in the Pod, PinkBlush, HATCH, Old Navy, Cake, Frida, ASOS, Destination, Isabella Oliver, and The Moms Co. Companies in the maternity products industry are focusing on innovation, quality, and omnichannel retail strategies to expand their presence. Many brands are enhancing their digital storefronts and optimizing e-commerce channels to meet rising demand for convenient, discreet shopping experiences. Product portfolios are being diversified with organic, dermatologically tested, and sustainability-certified offerings to cater to the health-conscious consumer base. Collaborations with healthcare professionals and influencers help boost brand credibility and consumer engagement. In-store experiences are being improved through personalized consultation services and curated displays.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 Pricing

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Consumer behaviour analysis

- 3.10.1 Purchasing patterns

- 3.10.2 Preference analysis

- 3.10.3 Regional variations in consumer behaviour

- 3.10.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 MEA

- 4.2.1.5 LATAM

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 – 2034, (USD Billion)(Thousand Units)

- 5.1 Key trends

- 5.2 Maternal apparel

- 5.3 Personal care products

- 5.4 Nutritional supplements

- 5.5 Maternity accessories

Chapter 6 Market Estimates & Forecast, By Application, 2021 – 2034, (USD Billion)(Thousand Units)

- 6.1 Key trends

- 6.2 Pregnancy

- 6.3 Postnatal

Chapter 7 Market Estimates & Forecast, By Pricing, 2021 – 2034, (USD Billion)(Thousand Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 – 2034, (USD Billion)(Thousand Units)

- 8.1 Key trends

- 8.2 Online sales

- 8.2.1 E-commerce

- 8.2.2 Company website

- 8.3 Offline sales

- 8.3.1 Wholesales/distributors

- 8.3.2 Hypermarkets/supermarkets

- 8.3.3 Specialty stores

- 8.3.4 Others(multi-brand stores, etc.)

Chapter 9 Market Estimates & Forecast, By Region, 2021 – 2034, (USD Billion)(Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 10.1 A Pea in the Pod

- 10.2 ASOS

- 10.3 Cake

- 10.4 Destination

- 10.5 Frida

- 10.6 Gap

- 10.7 H&M Mama

- 10.8 Hatch

- 10.9 Isabella Oliver

- 10.10 JoJo Maman Bebe

- 10.11 Motherhood

- 10.12 Old Navy

- 10.13 Pink Blush

- 10.14 Seraphine

- 10.15 The Moms Co.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日