|

市場調査レポート

商品コード

1773238

動物用皮膚科治療薬の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Veterinary Dermatology Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 動物用皮膚科治療薬の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月26日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

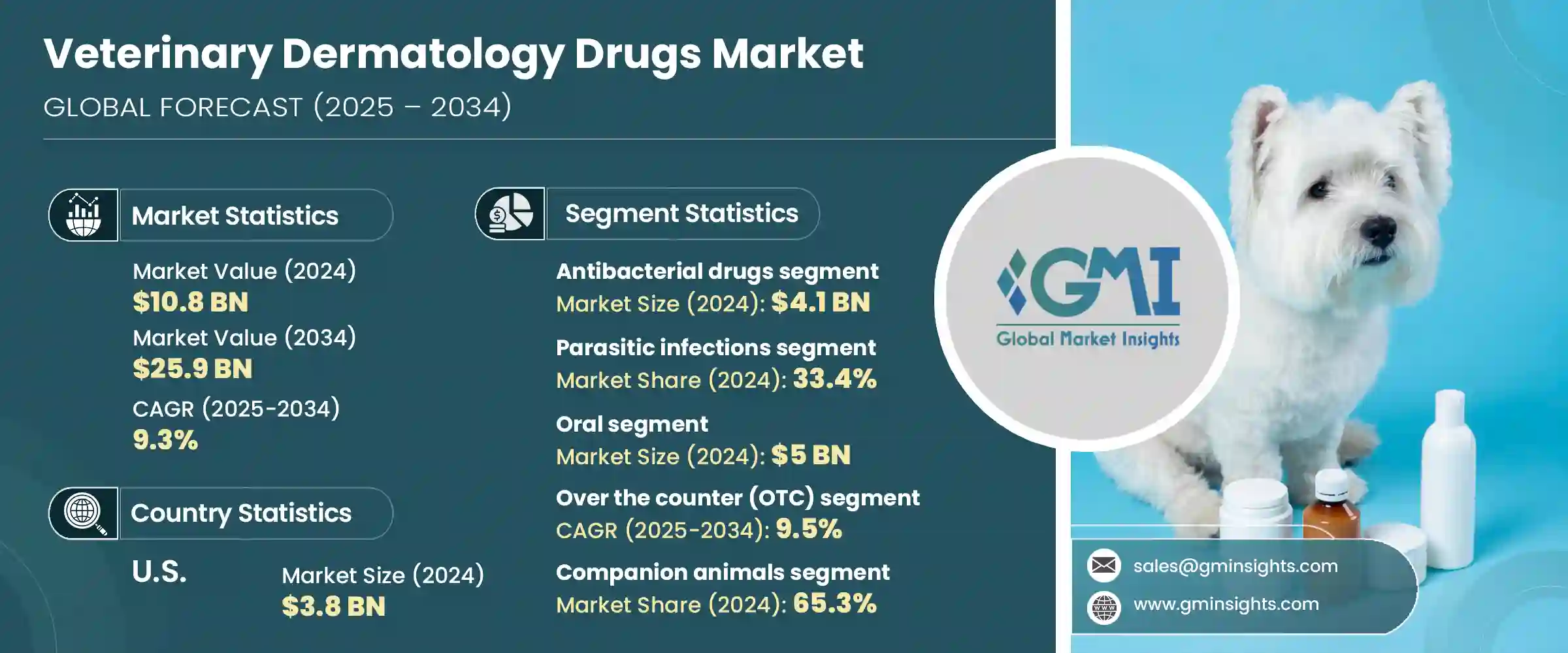

世界の動物用皮膚科治療薬市場は、2024年には108億米ドルと評価され、CAGR 9.3%で成長し、2034年には259億米ドルに達すると推定されています。

この成長を牽引しているのは、ペットの健康とウェルネスに対する意識の高まりと相まって、動物の皮膚疾患の発生率が急増していることです。ペットの飼育率が世界的に上昇を続ける中、皮膚病治療用の動物用医薬品の需要が急増しています。この需要は、特にコンパニオンアニマルが多く生息する都市部では、動物ヘルスケア支出の増加や医療化率の上昇によってさらに高まっています。動物ヘルスケアインフラへの投資は、特にアジア太平洋やラテンアメリカなどの新興経済圏で勢いを増しており、市場拡大の好条件を生み出しています。

市場開発のもう一つの要因は、治療効果を高めながら副作用の最小化を目指した先進的な皮膚科治療薬の開発です。製薬会社は、特に外用薬や経口薬など、投与のしやすさと有効性を向上させる新しい製剤に注力しています。皮膚病が動物の健康に与える影響に対する認識が高まり続けているため、市場では皮膚科に特化した薬剤の受け入れが拡大しています。さらに、家畜やコンパニオンアニマルの皮膚感染症の増加により、早期診断と早期治療の必要性が高まっており、動物病院全体で皮膚科治療薬の使用が広まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 108億米ドル |

| 予測金額 | 259億米ドル |

| CAGR | 9.3% |

動物用皮膚科治療薬には、感染症や炎症から自己免疫性皮膚疾患に至るまで、動物の皮膚疾患の管理や治療に用いられる幅広い治療が含まれます。これらの薬剤は通常、抗菌薬、抗真菌薬、抗寄生虫薬、抗炎症薬などいくつかの薬剤クラスに分類されます。これらの薬剤は、症状や治療に対する動物の反応に応じて、経口、外用、注射など複数の経路で投与されます。

薬剤クラス別では、抗菌薬が最大の市場シェアを占め、2024年には41億米ドルに達します。抗菌性動物用医薬品の需要は、特にコンパニオンアニマルの間で細菌性皮膚感染症の頻度が増加していることが大きな要因となっています。これらの感染症が一般的になるにつれ、獣医師は効果的な結果を出すために、より高度な抗菌製剤や併用療法に目を向けるようになっています。薬剤耐性株の出現も、より強力で標的を絞った抗菌製剤の必要性を加速させています。さらに、これらの疾患に対する認識の高まりと診断能力の向上により、早期発見が可能になったことも、このセグメントの安定した優位性に寄与しています。

適応症別では、寄生虫感染症が最大の市場シェアを占め、2024年には全体の33.4%を占める。寄生虫による皮膚疾患は、動物の皮膚科疾患として最も一般的なもの一つです。環境および気候条件の変化は、特に熱帯気候における寄生虫疾患の蔓延に一役買っています。これに対応するため、製薬会社は長時間作用型の抗寄生虫薬を外用剤と経口剤の両方で発売しています。これらの新しい製剤は、持続的な予防効果を発揮しながら、治療ルーチンを簡素化することに重点を置いています。抗寄生虫薬開発における継続的な研究と技術革新が、良好な規制条件と相まって、この分野の成長を支えています。流通網の拡大によるアクセスの向上も、このセグメントの好調な業績に寄与しています。

さまざまな投与経路の中で、経口薬は2024年に50億米ドルを占め、2034年までのCAGRは9%と予測されています。経口投与は、薬剤が血流を循環し、皮膚の問題の根本原因に取り組むことができる全身的アプローチのため、広く好まれています。また、動物は外用薬よりも経口薬を受け入れやすい傾向があるため、コンプライアンスも向上します。この高いコンプライアンス率は安定した治療結果につながり、このセグメントの需要を牽引しています。

地域別では、北米が世界の動物用皮膚科治療薬市場をリードし、2024年には38.6%のシェアを占めました。米国だけの市場規模は38億米ドルで、2023年の35億米ドルから増加しました。この地域の成長は、強固な研究開発能力の存在と、改良された製剤の着実な導入に起因しています。コンパニオンアニマルの数が多く、文化的にペットの世話が重視されていることが、この地域の圧倒的な市場地位の中心となっています。ペットの飼い主が動物のためのプレミアムヘルスケアソリューションへの投資を続ける中、皮膚科治療薬への需要もそれに追随しています。

市場内の競合は依然として激しく、多くの企業が的を絞った研究開発、製剤の革新、地理的拡大、進化する規制基準の遵守を通じて市場シェアの獲得に努めています。各社は、動物特有の皮膚科学的ニーズを満たす特化型製品の開発にますます注力し、急成長するこの分野で戦略的な位置づけを確立しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 皮膚疾患の発生率の上昇

- 技術的進歩

- 獣医皮膚科医の増加

- 動物ヘルスケア費の増加

- 業界の潜在的リスク&課題

- 副作用と安全性の懸念

- 治療費が高め

- 市場機会

- ペットの飼育数と支出の増加

- eコマースと小売チャネルの拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- テクノロジーの情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- 価格分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

第5章 市場推計・予測:薬剤クラス別、2021年~2034年

- 主要動向

- 抗菌薬

- 抗真菌薬

- 抗寄生虫薬

- その他の薬剤クラス

第6章 市場推計・予測:適応症別、2021年~2034年

- 主要動向

- 寄生虫感染症

- アレルギー感染症

- 自己免疫性皮膚疾患

- 皮膚がん

- その他の適応症

第7章 市場推計・予測:投与経路別、2021年~2034年

- 主要動向

- 経口

- 外用

- 注射剤

第8章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 処方箋

- 市販薬(OTC)

第9章 市場推計・予測:動物の種類別、2021年~2034年

- 主要動向

- コンパニオンアニマル

- 犬

- 猫

- 馬

- その他のペット

- 家畜

- 牛

- 豚

- その他の家畜

第10章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 動物病院薬局

- 小売薬局

- オンライン薬局

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- Bimeda

- Bioiberica

- Boehringer Ingelheim

- Ceva Sante Animale

- Dechra Pharmaceuticals

- Elanco Animal Health

- Indian Immunologicals

- Merck &Co.

- Vee Remedies

- Virbac

- Vetoquinol

- Vivaldis

- Zoetis

The Global Veterinary Dermatology Drugs Market was valued at USD 10.8 billion in 2024 and is estimated to grow at a CAGR of 9.3% to reach USD 25.9 billion by 2034. This growth is being driven by a sharp increase in the incidence of skin disorders among animals, coupled with rising awareness around pet health and wellness. As pet ownership continues to rise worldwide, demand for veterinary drugs designed to treat dermatological issues has surged. This demand is further amplified by an uptick in animal healthcare spending and an increasing medicalization rate, particularly in urban areas where companion animals are more prevalent. Investment in animal healthcare infrastructure is gaining momentum across emerging economies, especially in regions such as Asia-Pacific and Latin America, creating favorable conditions for market expansion.

Another factor contributing to the market's progress is the development of advanced dermatological drugs aimed at minimizing side effects while enhancing therapeutic outcomes. Pharmaceutical companies are focusing on new formulations, particularly topical and oral options, that improve ease of administration and efficacy. As awareness continues to grow about the impact of skin diseases on animal health, the market is witnessing greater acceptance of dermatology-specific medications. Additionally, the rise in skin infections among livestock and companion animals is pushing the need for early diagnosis and treatment, encouraging the widespread use of dermatology drugs across veterinary practices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.8 Billion |

| Forecast Value | $25.9 Billion |

| CAGR | 9.3% |

Veterinary dermatology drugs encompass a broad spectrum of treatments used to manage and cure skin disorders in animals, ranging from infections and inflammations to autoimmune skin conditions. These medications are typically categorized into several drug classes, including antibacterial, antifungal, antiparasitic, and anti-inflammatory drugs. These drugs are administered through multiple routes, such as oral, topical, and injectable, depending on the condition and the animal's response to treatment.

In terms of drug class, antibacterial medications held the largest market share, reaching a value of USD 4.1 billion in 2024. The demand for antibacterial veterinary drugs is largely fueled by the increasing frequency of bacterial skin infections, particularly among companion animals. As these infections become more common, veterinarians are turning to more advanced antibacterial formulations and combination therapies to deliver effective results. The emergence of drug-resistant strains has also accelerated the need for stronger and more targeted antibacterial products. Furthermore, the rising awareness of these conditions and improvements in diagnostic capabilities have enabled early detection, contributing to the consistent dominance of this segment.

By indication, parasitic infections accounted for the largest market share, capturing 33.4% of the total in 2024. Skin conditions caused by parasites are among the most common dermatological issues in animals. Changes in environmental and climatic conditions are playing a role in the increased spread of parasitic diseases, particularly in tropical climates. In response, pharmaceutical companies are introducing long-acting antiparasitic drugs in both topical and oral forms. These new formulations focus on simplifying treatment routines while delivering lasting protection. Ongoing research and innovation in antiparasitic drug development, combined with favorable regulatory conditions, are supporting segment growth. Enhanced access through expanded distribution networks has also contributed to the segment's strong performance.

Among the various routes of administration, oral drugs accounted for USD 5 billion in 2024 and are forecast to grow at a CAGR of 9% through 2034. Oral administration is widely preferred due to its systemic approach, which allows the drug to circulate through the bloodstream and tackle the root cause of skin issues. It also ensures better compliance, as animals tend to accept oral medications more readily than external applications. This high compliance rate contributes to consistent treatment results, which in turn drives demand in this segment.

Regionally, North America led the global veterinary dermatology drugs market, holding a 38.6% share in 2024. The market in the United States alone was valued at USD 3.8 billion that year, up from USD 3.5 billion in 2023. Growth in this region can be attributed to the presence of robust R&D capabilities and the steady introduction of improved drug formulations. The high volume of companion animals and the cultural emphasis on pet care are central to the region's dominant market position. As pet owners continue to invest in premium healthcare solutions for their animals, the demand for dermatology drugs has followed suit.

Competition within the market remains strong, with numerous players striving to gain market share through targeted R&D, innovation in drug formulations, geographic expansion, and compliance with evolving regulatory standards. Companies are increasingly focusing on creating specialized products that meet the unique dermatological needs of animals, positioning themselves strategically within this rapidly growing sector.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Drug class

- 2.2.3 Indication

- 2.2.4 Route of administration

- 2.2.5 Type

- 2.2.6 Animal type

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of dermatological diseases

- 3.2.1.2 Technological advancements

- 3.2.1.3 Increasing number of veterinary dermatology practitioners

- 3.2.1.4 Increased spending on animal healthcare

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Adverse side effects and safety concerns

- 3.2.2.2 High cost of treatment

- 3.2.3 Market opportunities

- 3.2.3.1 Rising pet ownership and spending

- 3.2.3.2 Expansion of e-commerce and retail channels

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Pricing analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Antibacterial drugs

- 5.3 Antifungal drugs

- 5.4 Antiparasitic drugs

- 5.5 Other drug classes

Chapter 6 Market Estimates and Forecast, By Indication, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Parasitic infections

- 6.3 Allergic infections

- 6.4 Autoimmune skin diseases

- 6.5 Skin cancer

- 6.6 Other indications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Topical

- 7.4 Injectable

Chapter 8 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Prescription

- 8.3 Over the counter (OTC)

Chapter 9 Market Estimates and Forecast, By Animal Type, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Companion animals

- 9.2.1 Dogs

- 9.2.2 Cats

- 9.2.3 Horses

- 9.2.4 Other companion animals

- 9.3 Livestock animals

- 9.3.1 Bovine

- 9.3.2 Swine

- 9.3.3 Other livestock animals

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Veterinary hospital pharmacies

- 10.3 Retail pharmacies

- 10.4 Online pharmacies

Chapter 11 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Bimeda

- 12.2 Bioiberica

- 12.3 Boehringer Ingelheim

- 12.4 Ceva Sante Animale

- 12.5 Dechra Pharmaceuticals

- 12.6 Elanco Animal Health

- 12.7 Indian Immunologicals

- 12.8 Merck & Co.

- 12.9 Vee Remedies

- 12.10 Virbac

- 12.11 Vetoquinol

- 12.12 Vivaldis

- 12.13 Zoetis