乳児用調製粉乳の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Infant Formula Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 245 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773232

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

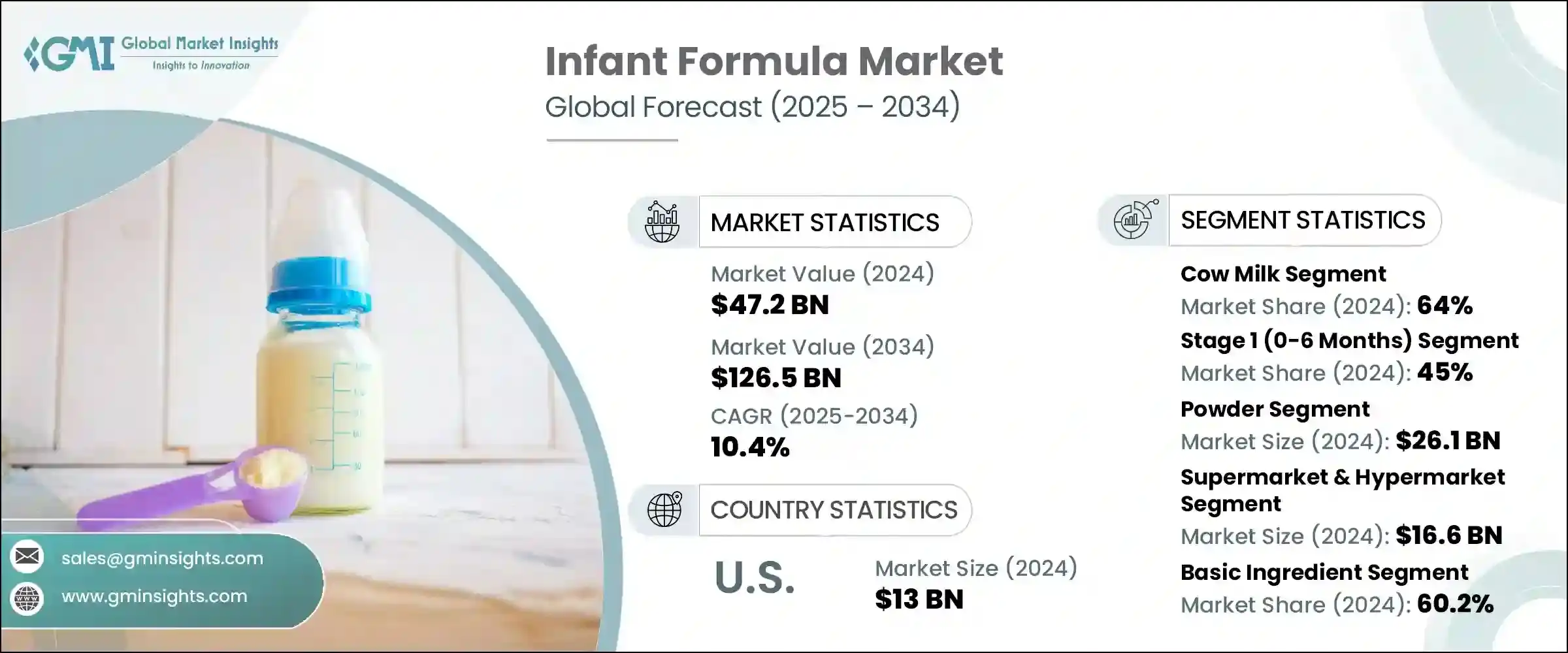

世界の乳児用調製粉乳市場は、2024年に472億米ドルと評価され、CAGR 10.4%で成長し、2034年には1,265億米ドルに達すると推定されています。

成長の主な要因は、乳幼児の栄養に関する意識の高まり、働く母親の増加、特に開発途上国における出生率の上昇です。都市化、可処分所得の増加、女性の労働参加率の上昇も市場拡大の要因です。さらに、保護者が製品の安全性、消化性、栄養価をより重視するようになり、オーガニック、無乳糖、低アレルギーなどの高級粉乳の需要が急増しています。

プレバイオティクス、プロバイオティクス、HMO(ヒトミルクオリゴ糖)、およびDHA/ARAを組み込んだような粉乳組成の技術的進歩は、これらの製品の受け入れをさらに後押ししています。しかし、これらの製品の高価格、複雑な規制、特に公衆衛生キャンペーンが普及している地域での母乳育児に対する強い文化的嗜好などの課題も残っています。また、一部の市場では、偽造粉乳に対する不安から消費者の信頼が得られていないことも、市場の成長を制限しています。親が合成添加物、遺伝子組み換え作物、人工甘味料を含まない製品を求めているため、クリーンラベル、オーガニック、植物由来のミルクへのシフトが顕著です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 472億米ドル |

| 予測金額 | 1,265億米ドル |

| CAGR | 10.4% |

2024年には、牛乳ベースの粉乳が64%のシェアを占め、2034年までのCAGRは10.4%と安定した成長を維持すると予想されます。この粉乳は、特にDHA、ARA、鉄分を強化した母乳のような栄養プロファイルのため、依然として最も好まれています。標準的な牛乳用調製粉乳は通常、母乳で育てていない健康な乳児に選ばれます。開発メーカーは、消化不良や軽度の牛乳不耐症の乳児のために、部分的加水分解粉乳や広範囲加水分解粉乳などの種類も開発しています。

ステージ別では、ステージ1(生後0~6ヵ月の乳児用)セグメントが最大のシェアを占め、2024年には45%を占めました。このセグメントは、2034年までのCAGRが10.6%で、急速な成長が見込まれています。乳児期のこの重要な段階では、消化器系がまだ成熟していないため、栄養補給は母乳か粉乳だけに頼っています。ステージ1用粉乳は胃にやさしく、DHA、ARA、プレバイオティクス、鉄分などの必須栄養素を含み、認知、免疫、消化器系の健康を促進するように設計されています。規制機関は、これらの製品の厳格な安全性と有効性の基準が満たされていることを保証し、それによって消費者の信頼を高めています。

2024年の米国の市場規模は130億米ドルで、2034年までにCAGR 8.4%で成長する見込みです。米国がリードしているのは、出生率の高さ、先進ヘルスケアシステム、乳児用調製粉乳の普及、ブランドロイヤルティの高さによるものです。この市場の特徴は、オーガニック、非遺伝子組換え、植物由来の選択肢、HMOやDHA/ARAを強化した製剤など、プレミアム製剤や特殊製剤の人気が高まっていることです。

この分野の主要企業には、Nestle、Abbott Nutrition、Arla Food、Bellamy's Organic、Bubs Australiaなどがあり、それぞれが市場での存在感を高めようと競い合っています。乳児用調製粉乳企業は、市場での地位を強化し、影響力を拡大するために、いくつかの戦略的イニシアチブを採用しています。特に粉乳の配合において、HMO、DHA、ARA、プレバイオティクスなど、母乳に含まれる栄養素に近いものを取り入れることで、技術革新に力を入れています。これらの改良は、乳児の認知発達、免疫、消化器系の健康を高めることを目的としています。さらに、これらの企業は研究開発への投資を大幅に増やし、無乳糖、オーガニック、低アレルギーのような特殊ミルクへの需要の高まりに対応する、より高度な新製品を生み出しています。

クリーンラベル、非遺伝子組み換え、植物由来の粉乳へのシフトも、健康志向の親の嗜好を満たすために受け入れられています。さらに、各社は流通網を強化し、小売店との提携を強化し、新興市場で事業を拡大することで、自社製品をより広く利用できるようにしています。大手ブランドはまた、最高の安全基準を遵守し、透明性のある製品表示を提供することで消費者の信頼を築くことに注力しており、これは今日の市場でますます重要になっています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査・検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク・課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- 技術・イノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- 栄養科学と製品開発

- 乳児の栄養所要量

- 主要栄養素の必要量

- タンパク質の必要量

- 炭水化物の必要量

- 脂肪の必要量

- 微量栄養素の必要量

- ビタミンの必要量

- ミネラルの必要量

- 年齢に応じた栄養ニーズ

- 特別な食事制限

- 主要栄養素の必要量

- 処方構成と基準

- 国際基準

- 地域による違い

- 品質仕様

- 安全パラメータ

- 機能性成分のイノベーション

- ヒトミルクオリゴ糖(HMO)

- プロバイオティクス・プレバイオティクス

- 長鎖多価不飽和脂肪酸

- ヌクレオチド・成長因子

- 製品開発プロセス

- 研究開発

- 臨床研究・試験

- 規制承認プロセス

- 商業発売

- 栄養成分表示とポジショニング

- 健康強調表示に関する規制

- 科学的根拠

- マーケティングコミュニケーション

- 消費者教育

- 将来の栄養動向

- パーソナライズされた栄養

- マイクロバイオーム研究

- 認知発達サポート

- 免疫システムの強化

- 乳児の栄養所要量

- 製造および品質管理

- 製造工程

- 原材料の準備

- 混合・調合

- 熱処理

- 噴霧乾燥

- 包装・密封

- 品質管理システム

- 適正製造規範(GMP)

- 危害分析重要管理点(HACCP)

- 品質保証テスト

- バッチテストプロトコル

- 安全・汚染管理

- 微生物学的安全性

- 化学汚染物質の制御

- 物理的危険の防止

- アレルゲン管理

- 設備・技術

- 処理装置

- 試験・分析機器

- 包装機械

- 自動化および制御システム

- サプライチェーンマネジメント

- 原材料調達

- サプライヤー資格

- 在庫管理

- コールドチェーン管理

- 規制遵守

- 製造基準

- 施設検査

- 文書化要件

- リコール手順

- 製造工程

- 消費者行動と市場力学

- 消費者の人口統計

- 親の年齢層

- 所得水準

- 教育レベル

- 地理的分布

- 購入決定要因

- 栄養上の利点

- ブランドの信頼と評判

- 価格感度

- ヘルスケア提供者の推奨事項

- 利便性要因

- 摂食パターンと好み

- 完全粉乳授乳

- 混合授乳(母乳+粉乳)

- 移行期授乳

- 文化的授乳習慣

- 情報源・影響

- ヘルスケア従事者

- オンラインリソース

- 家族・友人

- ソーシャルメディアの影響要因

- ブランドロイヤルティ・切り替え行動

- ブランドロイヤルティ要因

- 切り替えトリガー

- トライアルと採用のパターン

- 推奨行動

- 地域別の消費者の違い

- 北米の消費者

- 欧州の消費者

- アジア太平洋の消費者

- その他の地域

- 消費者の人口統計

- マーケティング・流通戦略

- マーケティング戦略

- ブランドポジショニング

- プレミアムポジショニング

- 価値ポジショニング

- 専門分野ポジショニング

- ターゲットオーディエンスのセグメンテーション

- マーケティングチャネル

- ヘルスケア専門家の関与

- デジタルマーケティング

- 従来のメディア

- 教育プログラム

- ブランドポジショニング

- 流通戦略

- マルチチャネル配信

- チャネルパートナー管理

- 地理的拡大

- 市場浸透戦略

- 価格戦略

- プレミアム価格

- 競争力のある価格

- 価値に基づく価格設定

- 地域による価格差

- プロモーション活動

- ヘルスケア専門家向けプログラム

- 消費者教育キャンペーン

- サンプリングプログラム

- ロイヤルティプログラム

- デジタル変革

- Eコマース戦略

- デジタル顧客エンゲージメント

- データ分析と洞察

- オムニチャネル統合

- 規制上のマーケティング上の考慮事項

- WHOコード準拠

- 広告制限

- 健康強調表示規制

- 倫理的なマーケティング慣行

- マーケティング戦略

- イノベーションと将来の動向

- 現在のイノベーションの動向

- 機能性成分

- オーガニック&クリーンラベル

- パーソナライズされた栄養

- 持続可能な包装

- 新興技術

- 精密栄養

- マイクロカプセル化

- 新しい処理技術

- スマートパッケージ

- 研究開発の重点

- 腸内細菌叢研究

- 認知発達

- 免疫システムのサポート

- アレルギー予防

- 持続可能性への取り組み

- 持続可能な調達

- 二酸化炭素排出量の削減

- 循環型経済の原則

- 環境影響の緩和

- デジタルイノベーション

- スマート授乳ソリューション

- モバイルアプリ

- IoT統合

- AIを活用した推奨事項

- 将来の市場動向

- 市場の統合

- プレミアムセグメントの成長

- 新興市場の拡大

- 規制の進化

- 現在のイノベーションの動向

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021~2034年

- 主な傾向

- 牛乳ベースの粉乳

- 標準的牛乳配合

- 部分加水分解配合

- 完全加水分解配合

- 大豆ベースの粉乳

- タンパク質加水分解物配合

- 特殊配合

- 未熟児用調製粉乳

- 逆流防止処方

- 乳糖不使用

- アミノ酸ベース配合

- その他

- オーガニック粉乳

- ヤギミルクベースの粉乳

第6章 市場推計・予測:ステージ別、2021~2034年

- 主な傾向

- ステージ1(0~6か月)

- ステージ2(6~12か月)

- ステージ3(12~24か月)

- ステージ4(24か月以上)

第7章 市場推計・予測:形態別、2021~2034年

- 主な傾向

- 粉末

- 液体濃縮物

- すぐに飲める

第8章 市場推計・予測:流通チャネル別、2021~2034年

- 主な傾向

- スーパーマーケット・ハイパーマーケット

- 薬局・ドラッグストア

- オンライン小売

- eコマースプラットフォーム

- 消費者直販ウェブサイト

- ベビー用品専門店

- 病院・クリニック

- コンビニエンスストア

- その他

第9章 市場推計・予測:成分別、2021~2034年

- 主な傾向

- 基本的な材料

- タンパク質

- ホエイプロテイン

- カゼイン

- 大豆タンパク質

- 炭水化物

- 乳糖

- コーンシロップ固形物

- その他

- 脂肪・油

- 植物油

- DHA・ARA

- タンパク質

- 機能性成分

- プレバイオティクス

- プロバイオティクス

- ヒトミルクオリゴ糖(HMO)

- ヌクレオチド

- ビタミン・ミネラル

- ビタミン

- ミネラル

第10章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東およびアフリカ

第11章 企業プロファイル

- Abbott Nutrition

- Arla Food

- Bellamy's Organic

- BUBS Australia

- Hero Group

- Mead Johnson Nutrition

- Nestle

- Nutricia

- The Kraft Heinz Company

- Danone S.A.

- Reckitt Benckiser Group plc(Mead Johnson)

- Perrigo Company plc

目次

The Global Infant Formula Market was valued at USD 47.2 billion in 2024 and is estimated to grow at a CAGR of 10.4% to reach USD 126.5 billion by 2034. The growth is largely attributed to rising awareness around infant nutrition, the increasing number of working mothers, and higher birth rates, especially in developing nations. Urbanization, an increase in disposable income, and higher female workforce participation are also contributing factors to the market expansion. Additionally, parents are becoming more concerned with product safety, digestibility, and nutritional value, leading to a surge in demand for premium formulas, including organic, lactose-free, and hypoallergenic options.

Technological advancements in formula composition, like incorporating prebiotics, probiotics, HMOs (human milk oligosaccharides), and DHA/ARA, are further boosting the acceptance of these products. However, challenges remain, including the high cost of these products, complex regulations, and strong cultural preferences for breastfeeding, particularly in regions where public health campaigns are prevalent. Market growth is also limited by a lack of consumer trust in some markets due to fears about counterfeit formulas. There is a noticeable shift towards clean-label, organic, and plant-based formulas, as parents demand products free of synthetic additives, GMOs, and artificial sweeteners.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $47.2 Billion |

| Forecast Value | $126.5 Billion |

| CAGR | 10.4% |

In 2024, the cow milk-based formula segment commanded a 64% share and is expected to maintain steady growth with a CAGR of 10.4% through 2034. This formula remains the most preferred due to its nutritional profile, which is like breast milk, especially when fortified with DHA, ARA, and iron. Standard cow's milk formula is typically chosen for healthy, full-term infants who are not breastfed. Manufacturers have also developed varieties like partially and extensively hydrolyzed formulas to cater to infants with digestive issues or mild cow's milk intolerance.

Among different stages, the Stage 1 (for infants aged 0-6 months) segment holds the largest share, accounting for 45% in 2024. This segment is expected to see rapid growth, driven by a CAGR of 10.6% through 2034. At this critical stage of infancy, babies rely solely on breast milk or formula for nourishment as their digestive systems are still maturing. Stage 1 formulas are designed to be gentle on the stomach, containing essential nutrients like DHA, ARA, prebiotics, and iron to promote cognitive, immune, and digestive health. Regulatory bodies ensure that strict safety and efficacy standards are met for these products, thereby enhancing consumer confidence.

U.S. Infant Formula Market generated USD 13 billion in 2024 and is set to grow at a CAGR of 8.4% by 2034. The U.S. leads due to its high birth rates, advanced healthcare systems, widespread availability of infant formula, and strong brand loyalty. The market here is characterized by the increasing popularity of premium and speciality formulas, including organic, non-GMO, and plant-based options, as well as formulas enriched with HMOs and DHA/ARA.

Leading companies in this space include Nestle, Abbott Nutrition, Arla Food, Bellamy's Organic, and Bubs Australia, each vying for a stronger market presence. Infant formula companies have been adopting several strategic initiatives to strengthen their market position and expand their influence. They are focusing heavily on innovation, particularly in formula composition, by incorporating nutrients that closely mimic those found in breast milk, such as HMOs, DHA, ARA, and prebiotics. These improvements aim to enhance cognitive development, immunity, and digestive health for infants. Moreover, these companies are significantly increasing their investments in research and development to create new, more advanced products that cater to the growing demand for speciality formulas, such as lactose-free, organic, and hypoallergenic varieties.

The shift toward clean-label, non-GMO, and plant-based formulas is also being embraced to meet the preferences of health-conscious parents. Additionally, companies are enhancing their distribution networks, strengthening retail partnerships, and expanding in emerging markets to ensure the wider availability of their products. Leading brands are also focusing on building consumer trust by adhering to the highest safety standards and offering transparent product labeling, which is increasingly important in today's market.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Stage

- 2.2.4 Form

- 2.2.5 Distribution channel

- 2.2.6 Ingredient

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Nutritional Science & product development

- 3.13.1 Nutritional Requirements for Infants

- 3.13.1.1 Macronutrient requirements

- 3.13.1.1.1 Protein requirements

- 3.13.1.1.2 Carbohydrate requirements

- 3.13.1.1.3 Fat requirements

- 3.13.1.2 Micronutrient requirements

- 3.13.1.2.1 Vitamin requirements

- 3.13.1.2.2 Mineral requirements

- 3.13.1.3 Age-Specific nutritional needs

- 3.13.1.4 Special dietary requirements

- 3.13.1.1 Macronutrient requirements

- 3.13.2 Formula composition & standards

- 3.13.2.1 International standards

- 3.13.2.2 Regional variations

- 3.13.2.3 Quality specifications

- 3.13.2.4 Safety parameters

- 3.13.3 Functional ingredients innovation

- 3.13.3.1 Human Milk Oligosaccharides (HMO)

- 3.13.3.2 Probiotics & prebiotics

- 3.13.3.3 Long-Chain Polyunsaturated Fatty Acids

- 3.13.3.4 Nucleotides & growth factors

- 3.13.4 Product development process

- 3.13.4.1 Research & development

- 3.13.4.2 Clinical studies & trials

- 3.13.4.3 Regulatory approval process

- 3.13.4.4 Commercial launch

- 3.13.5 Nutritional claims & positioning

- 3.13.5.1 Health claims regulations

- 3.13.5.2 Scientific substantiation

- 3.13.5.3 Marketing communications

- 3.13.5.4 Consumer education

- 3.13.6 Future nutritional trends

- 3.13.6.1 Personalized nutrition

- 3.13.6.2 Microbiome research

- 3.13.6.3 Cognitive development support

- 3.13.6.4 Immune system enhancement

- 3.13.1 Nutritional Requirements for Infants

- 3.14 Manufacturing & quality control

- 3.14.1 Manufacturing process

- 3.14.1.1 Raw material preparation

- 3.14.1.2 Blending & mixing

- 3.14.1.3 Heat treatment

- 3.14.1.4 Spray drying

- 3.14.1.5 Packaging & sealing

- 3.14.2 Quality control systems

- 3.14.2.1 Good Manufacturing Practices (GMP)

- 3.14.2.2 Hazard Analysis Critical Control Points (HACCP)

- 3.14.2.3 Quality assurance testing

- 3.14.2.4 Batch testing protocols

- 3.14.3 Safety & contamination control

- 3.14.3.1 Microbiological safety

- 3.14.3.2 Chemical contaminant control

- 3.14.3.3 Physical hazard prevention

- 3.14.3.4 Allergen management

- 3.14.4 Equipment & technology

- 3.14.4.1 Processing equipment

- 3.14.4.2 Testing & analysis equipment

- 3.14.4.3 Packaging machinery

- 3.14.4.4 Automation & control systems

- 3.14.5 Supply chain management

- 3.14.5.1 Raw material sourcing

- 3.14.5.2 Supplier qualification

- 3.14.5.3 Inventory management

- 3.14.5.4 Cold chain management

- 3.14.6 Regulatory compliance

- 3.14.6.1 Manufacturing standards

- 3.14.6.2 Facility inspections

- 3.14.6.3 Documentation requirements

- 3.14.6.4 Recall procedures

- 3.14.1 Manufacturing process

- 3.15 Consumer behavior & market dynamics

- 3.15.1 Consumer demographics

- 3.15.1.1 Parental age groups

- 3.15.1.2 Income levels

- 3.15.1.3 Education levels

- 3.15.1.4 Geographic distribution

- 3.15.2 Purchase decision factors

- 3.15.2.1 Nutritional benefits

- 3.15.2.2 Brand trust & reputation

- 3.15.2.3 Price sensitivity

- 3.15.2.4 Healthcare provider recommendations

- 3.15.2.5 Convenience factors

- 3.15.3 Feeding patterns & preferences

- 3.15.3.1 Exclusive formula feeding

- 3.15.3.2 Mixed feeding (breast + formula)

- 3.15.3.3 Transitional feeding

- 3.15.3.4 Cultural feeding practices

- 3.15.4 Information sources & influences

- 3.15.4.1 Healthcare professionals

- 3.15.4.2 Online resources

- 3.15.4.3 Family & friends

- 3.15.4.4 Social media influence

- 3.15.5 Brand loyalty & switching behavior

- 3.15.5.1 Brand loyalty factors

- 3.15.5.2 Switching triggers

- 3.15.5.3 Trial & adoption patterns

- 3.15.5.4 Recommendation behavior

- 3.15.6 Regional consumer variations

- 3.15.6.1 North American consumers

- 3.15.6.2 European consumers

- 3.15.6.3 Asia-Pacific consumers

- 3.15.6.4 Other regional patterns

- 3.15.1 Consumer demographics

- 3.16 Marketing & distribution strategies

- 3.16.1 Marketing strategies

- 3.16.1.1 Brand positioning

- 3.16.1.1.1 Premium positioning

- 3.16.1.1.2 Value positioning

- 3.16.1.1.3 Specialty positioning

- 3.16.1.2 Target audience segmentation

- 3.16.1.3 Marketing channels

- 3.16.1.3.1 Healthcare professional engagement

- 3.16.1.3.2 Digital marketing

- 3.16.1.3.3 Traditional media

- 3.16.1.3.4 Educational programs

- 3.16.1.1 Brand positioning

- 3.16.2 Distribution strategies

- 3.16.2.1 Multi-channel distribution

- 3.16.2.2 Channel partner management

- 3.16.2.3 Geographic expansion

- 3.16.2.4 Market penetration strategies

- 3.16.3 Pricing strategies

- 3.16.3.1 Premium pricing

- 3.16.3.2 Competitive pricing

- 3.16.3.3 Value-based pricing

- 3.16.3.4 Regional pricing variations

- 3.16.4 Promotional activities

- 3.16.4.1 Healthcare professional programs

- 3.16.4.2 Consumer education campaigns

- 3.16.4.3 Sampling programs

- 3.16.4.4 Loyalty programs

- 3.16.5 Digital transformation

- 3.16.5.1 E-commerce strategies

- 3.16.5.2 Digital customer engagement

- 3.16.5.3 Data analytics & insights

- 3.16.5.4 Omnichannel integration

- 3.16.6 Regulatory marketing considerations

- 3.16.6.1 WHO code compliance

- 3.16.6.2 Advertising restrictions

- 3.16.6.3 Health claims regulations

- 3.16.6.4 Ethical marketing practices

- 3.16.1 Marketing strategies

- 3.17 Innovation & future trends

- 3.17.1 Current innovation trends

- 3.17.1.1 Functional ingredients

- 3.17.1.2 Organic & clean label

- 3.17.1.3 Personalized nutrition

- 3.17.1.4 Sustainable packaging

- 3.17.2 Emerging technologies

- 3.17.2.1 Precision nutrition

- 3.17.2.2 Microencapsulation

- 3.17.2.3 Novel processing technologies

- 3.17.2.4 Smart packaging

- 3.17.3 Research & development focus

- 3.17.3.1 Gut microbiome research

- 3.17.3.2 Cognitive development

- 3.17.3.3 Immune system support

- 3.17.3.4 Allergy prevention

- 3.17.4 Sustainability initiatives

- 3.17.4.1 Sustainable sourcing

- 3.17.4.2 Carbon footprint reduction

- 3.17.4.3 Circular economy principles

- 3.17.4.4 Environmental impact mitigation

- 3.17.5 Digital innovation

- 3.17.5.1 Smart feeding solutions

- 3.17.5.2 Mobile applications

- 3.17.5.3 IoT integration

- 3.17.5.4 AI-Powered recommendations

- 3.17.6 Future market trends

- 3.17.6.1 Market consolidation

- 3.17.6.2 Premium segment growth

- 3.17.6.3 Emerging market expansion

- 3.17.6.4 Regulatory evolution

- 3.17.1 Current innovation trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trend

- 5.2 Cow's milk-based formula

- 5.2.1 Standard cow's milk formula

- 5.2.2 Partially hydrolyzed formula

- 5.2.3 Extensively hydrolyzed formula

- 5.3 Soy-based formula

- 5.4 Protein hydrolysate formula

- 5.5 Specialty formula

- 5.5.1 Premature infant formula

- 5.5.2 Anti-reflux formula

- 5.5.3 Lactose-free formula

- 5.5.4 Amino acid-based formula

- 5.5.5 Other specialty formulas

- 5.6 Organic formula

- 5.7 Goat milk-based formula

Chapter 6 Market Estimates & Forecast, By Stage, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trend

- 6.2 Stage 1 (0–6 months)

- 6.3 Stage 2 (6–12 months)

- 6.4 Stage 3 (12–24 months)

- 6.5 Stage 4 (24+ months)

Chapter 7 Market Estimates & Forecast, By Form, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trend

- 7.2 Powder

- 7.3 Liquid concentrate

- 7.4 Ready-to-feed

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trend

- 8.2 Supermarkets & Hypermarkets

- 8.3 Pharmacies & Drug Stores

- 8.4 Online Retail

- 8.4.1 E-commerce Platforms

- 8.4.2 Direct-to-Consumer Websites

- 8.5 Specialty Baby Stores

- 8.6 Hospitals & Clinics

- 8.7 Convenience Stores

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Ingredient, 2021-2034 (USD Million) (Kilo Tons)

- 9.1 Key trend

- 9.2 Basic Ingredients

- 9.2.1 Proteins

- 9.2.1.1 Whey Protein

- 9.2.1.2 Casein

- 9.2.1.3 Soy Protein

- 9.2.2 Carbohydrates

- 9.2.2.1 Lactose

- 9.2.2.2 Corn Syrup Solids

- 9.2.2.3 Other Carbohydrates

- 9.2.3 Fats & Oils

- 9.2.3.1 Vegetable Oils

- 9.2.3.2 DHA & ARA

- 9.2.1 Proteins

- 9.3 Functional Ingredients

- 9.3.1 Prebiotics

- 9.3.2 Probiotics

- 9.3.3 Human Milk Oligosaccharides (HMO)

- 9.3.4 Nucleotides

- 9.4 Vitamins & Minerals

- 9.4.1 Vitamins

- 9.4.2 Minerals

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East & Africa

Chapter 11 Company Profiles

- 11.1 Abbott Nutrition

- 11.2 Arla Food

- 11.3 Bellamy's Organic

- 11.4 BUBS Australia

- 11.5 Hero Group

- 11.6 Mead Johnson Nutrition

- 11.7 Nestle

- 11.8 Nutricia

- 11.9 The Kraft Heinz Company

- 11.10 Danone S.A.

- 11.11 Reckitt Benckiser Group plc (Mead Johnson)

- 11.12 Perrigo Company plc

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 245 Pages

- 納期

- 2~3営業日