|

市場調査レポート

商品コード

1773223

ガス焚き型不動産用発電機の市場機会、成長促進要因、産業動向分析、2025~2034年予測Gas Fired Real Estate Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ガス焚き型不動産用発電機の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年06月16日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

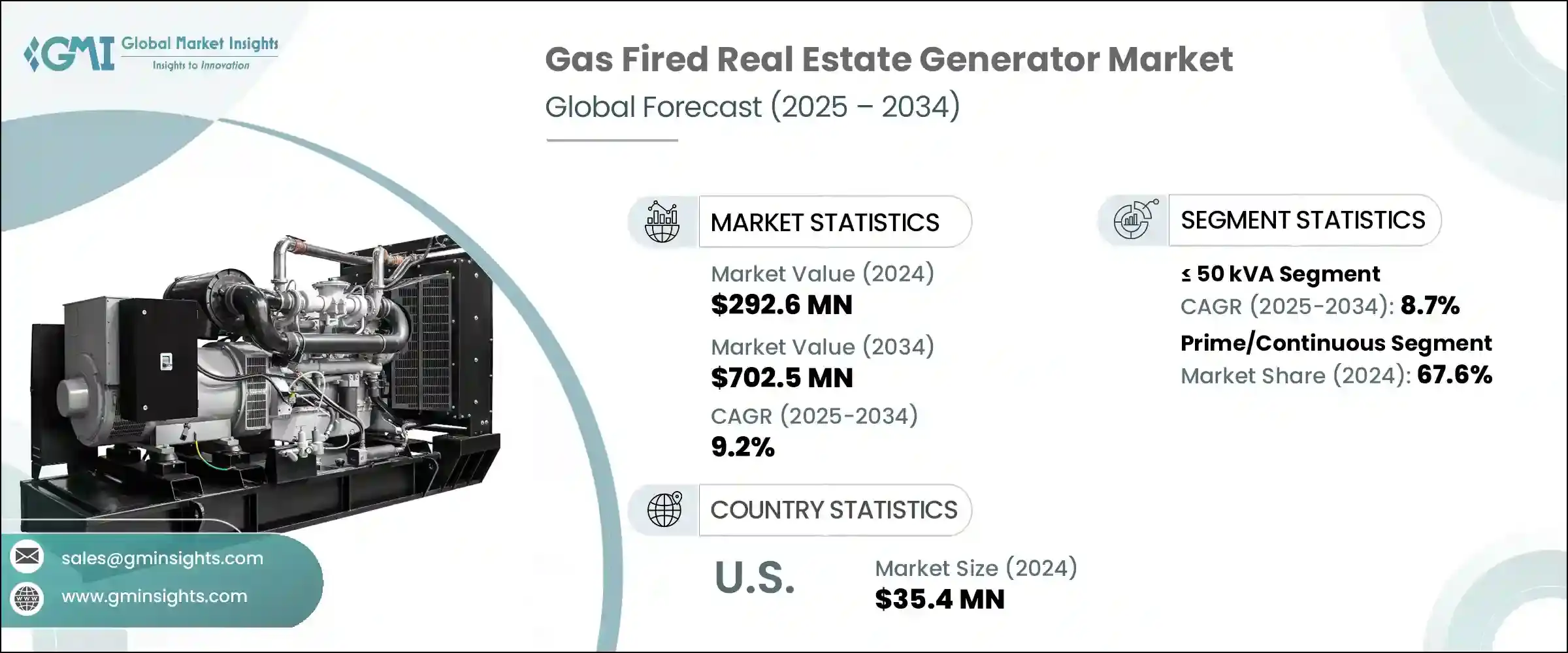

世界のガス焚き型不動産用発電機の市場規模は、2024年に2億9,260万米ドルとなり、CAGR 9.2%で成長し、2034年には7億250万米ドルに達すると予測されています。

新興経済諸国におけるインフラプロジェクトの拡大と相まって、都市開発のペースが高まっており、この分野全体の需要を押し上げています。住宅地や商業地では頻繁に電力が途絶え、送電網の性能が不安定になるため、開発業者は継続的な電力を保証するためにガス焚き発電機を導入しています。これらのユニットは、一貫したユーティリティの供給がない地域で信頼性を高めるため、ハイブリッドマイクログリッドに統合されています。不動産開発は、建設段階だけでなく、信頼性の高いバックアップシステムとして完成後も発電機の恩恵を受け、全体的な資産価値と経営の安定性を高めています。

排出量の多いディーゼル発電機を段階的に廃止する規制が強化される中、よりクリーンなガス発電機への関心が高まっています。持続可能なインフラを促進する規制上の優遇措置や、環境に優しい建物への関心の高まりに後押しされ、これらの発電機は急速に普及しつつあります。高層住宅から商業施設に至るまで、近代的な不動産への導入は、信頼性の高い低排出電力の需要によって推進されています。騒音低減、燃費向上、自動負荷管理などの機能強化と相まって、新興経済諸国と先進地域の両方で、政府による義務付けが採用を加速しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 2億9,260万米ドル |

| 予測金額 | 7億250万米ドル |

| CAGR | 9.2% |

出力別では、2024年、50kVA~125kVA以上セグメントは7,090万米ドルを占めました。これらのシステムは、最新の環境基準を満たしながら、送電網が不安定な地域でも信頼性の高い電力を供給できることから好まれています。より静かな運転や燃料性能の向上など、設計の継続的な強化が引き続き投資を呼び込むと予想されます。

用途別では、スタンバイセグメントは、2034年までCAGR 9%で成長すると予測されます。この成長を支えているのは、排出量削減に焦点を当てた規制基準の進化と、自動負荷最適化のようなスマート機能によるエネルギー効率の重視の高まりです。

アジア太平洋地域のガス焚き型不動産用発電機市場は、2034年までに2億6,000万米ドルに達すると予想されます。アジア太平洋地域市場は、急速な都市拡大と地域のガス配給インフラの大幅な改善に支えられています。都市開発プロジェクトのためのクリーンで安定したエネルギーへの顕著なシフトは、この地域の成長する建設セクター全体でガスベースの発電機の必要性を強化しています。

ガス焚き型不動産用発電機市場で事業を展開する主要企業には、Mitsubishi Heavy Industries、Atlas Copco、Caterpillar、Rolls-Royce、Aggreko、Ashok Leyland、Cummins、HIMOINSA、Generac Power Systems、Mahindra Powerol、J.C. Bamford Excavators、PR Industrial、Rehlko、Kirloskar、Yanmar Holdingsなどがあります。主要企業は、低公害のバックアップソリューションに対する需要の高まりに対応するため、環境に優しく高効率の発電機モデルでポートフォリオを拡大することに注力しています。メーカーは、自動負荷分散、リアルタイム監視、騒音低減システムなどのスマート技術を統合し、ユーザーエクスペリエンスと環境基準への準拠を強化しています。多くの企業は、都市化する地域全体でタイムリーに製品を入手できるよう、サプライチェーンと流通網を強化しています。不動産開発業者や政府が支援するインフラ構想との提携は、長期契約を確保するための中核戦略となりつつあります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク・課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:出力別、2021~2034年

- 主要動向

- 50kVA以下

- 50kVA~125kVA以上

- 125kVA~200kVA以上

- 200kVA~350kVA以上

- 350kVA~500kVA以上

- 500kVA以上

第6章 市場規模・予測:用途別、2021~2034年

- 主要動向

- スタンドバイ

- プライム/連続

第7章 市場規模・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ロシア

- 英国

- ドイツ

- フランス

- スペイン

- オーストリア

- イタリア

- アジア太平洋地域

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- インドネシア

- マレーシア

- タイ

- ベトナム

- フィリピン

- 中東

- サウジアラビア

- アラブ首長国連邦

- カタール

- トルコ

- イラン

- オマーン

- アフリカ

- エジプト

- ナイジェリア

- アルジェリア

- 南アフリカ

- アンゴラ

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- チリ

第8章 企業プロファイル

- Aggreko

- Ashok Leyland

- Atlas Copco

- Caterpillar

- Cummins

- Generac Power Systems

- HIMOINSA

- J.C. Bamford Excavators

- Kirloskar

- Rehlko

- Mahindra Powerol

- Mitsubishi Heavy Industries

- PR Industrial

- Rolls-Royce

- Yanmar Holdings

The Global Gas Fired Real Estate Generator Market was valued at USD 292.6 million in 2024 and is estimated to grow at a CAGR of 9.2% to reach USD 702.5 million by 2034. The increasing pace of urban development, combined with expanding infrastructure projects across emerging economies, is boosting demand across the sector. Frequent power interruptions and unstable grid performance in residential and commercial zones are prompting developers to deploy gas-fired gensets to guarantee continuous electricity. These units are being integrated into hybrid microgrids for better reliability in regions lacking consistent utility coverage. Real estate developments benefit from these gensets not only during construction phases but also post-completion as reliable backup systems, thereby enhancing overall property value and operational stability.

With stricter regulations phasing out high-emission diesel gensets, interest is shifting toward cleaner gas-powered alternatives. Backed by regulatory incentives promoting sustainable infrastructure and growing interest in eco-friendly buildings, these generators are gaining rapid traction. Their deployment in modern real estate-from residential high-rises to commercial complexes-is being driven by demands for reliable, low-emission power. Government mandates, coupled with enhanced features such as reduced noise, better fuel economy, and automated load management, are accelerating adoption across both developing and developed regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $292.6 Million |

| Forecast Value | $702.5 Million |

| CAGR | 9.2% |

In 2024, the > 50 kVA - 125 kVA generator segment accounted for USD 70.9 million. These systems are preferred for their ability to deliver reliable power in areas with grid instability while meeting updated environmental standards. Ongoing enhancements in design, such as quieter operations and improved fuel performance, are expected to continue drawing investment.

The standby segment within the gas-fired real estate generator market is forecast to grow at a CAGR of 9% through 2034. This growth is underpinned by evolving regulatory standards focused on cutting emissions and an increased emphasis on energy efficiency through smart features like automatic load optimization.

Asia Pacific Gas Fired Real Estate Generator Market is expected to reach USD 260 million by 2034, supported by fast-paced urban expansion and significant improvements in regional gas distribution infrastructure. A marked shift toward clean, stable energy for urban development projects is reinforcing the need for gas-based generators across the region's growing construction sector.

Major players operating in the Gas Fired Real Estate Generator Market include Mitsubishi Heavy Industries, Atlas Copco, Caterpillar, Rolls-Royce, Aggreko, Ashok Leyland, Cummins, HIMOINSA, Generac Power Systems, Mahindra Powerol, J.C. Bamford Excavators, PR Industrial, Rehlko, Kirloskar, and Yanmar Holdings. Leading companies are focusing on expanding their portfolios with eco-friendly and high-efficiency generator models to address the growing demand for low-emission backup solutions. Manufacturers are integrating smart technologies such as automated load balancing, real-time monitoring, and noise-reduction systems to enhance user experience and compliance with environmental norms. Many firms are strengthening their supply chain and distribution networks to ensure timely product availability across urbanizing regions. Partnerships with real estate developers and government-backed infrastructure initiatives are becoming a core strategy to secure long-term contracts.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Rating, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 ≤ 50 kVA

- 5.3 > 50 kVA - 125 kVA

- 5.4 > 125 kVA - 200 kVA

- 5.5 > 200 kVA - 350 kVA

- 5.6 > 350 kVA - 500 kVA

- 5.7 > 500 kVA

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Standby

- 6.3 Prime/continuous

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Russia

- 7.3.2 UK

- 7.3.3 Germany

- 7.3.4 France

- 7.3.5 Spain

- 7.3.6 Austria

- 7.3.7 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.4.6 Indonesia

- 7.4.7 Malaysia

- 7.4.8 Thailand

- 7.4.9 Vietnam

- 7.4.10 Philippines

- 7.5 Middle East

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Turkey

- 7.5.5 Iran

- 7.5.6 Oman

- 7.6 Africa

- 7.6.1 Egypt

- 7.6.2 Nigeria

- 7.6.3 Algeria

- 7.6.4 South Africa

- 7.6.5 Angola

- 7.7 Latin America

- 7.7.1 Brazil

- 7.7.2 Mexico

- 7.7.3 Argentina

- 7.7.4 Chile

Chapter 8 Company Profiles

- 8.1 Aggreko

- 8.2 Ashok Leyland

- 8.3 Atlas Copco

- 8.4 Caterpillar

- 8.5 Cummins

- 8.6 Generac Power Systems

- 8.7 HIMOINSA

- 8.8 J.C. Bamford Excavators

- 8.9 Kirloskar

- 8.10 Rehlko

- 8.11 Mahindra Powerol

- 8.12 Mitsubishi Heavy Industries

- 8.13 PR Industrial

- 8.14 Rolls-Royce

- 8.15 Yanmar Holdings