ブルー水素市場のビジネスチャンス、成長要因、業界動向分析、および2026年~2035年の予測

Blue Hydrogen Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035- 発行日

- ページ情報

- 英文 123 Pages

- 納期

- 2~3営業日

- 商品コード

- 2061456

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

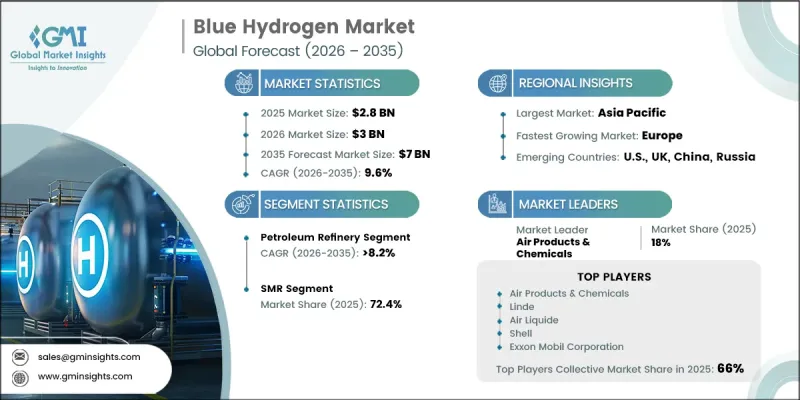

世界のブルー水素市場は、2025年に28億米ドルと評価され、CAGR 9.6%で成長し、2035年までに70億米ドルに達すると推定されています。

エネルギー安全保障への関心の高まりや水素供給源の多様化が、今後数年間でブルー水素産業の力強い拡大を支えると予想されます。ブルー水素の生産は、天然ガスを原料として利用しつつ、比較的低い炭素排出量で大規模な水素生成を可能にします。大手企業による低炭素水素インフラへの投資増加が、市場の発展をさらに加速させています。よりクリーンな代替エネルギーに対する世界の需要の高まりや、産業の脱炭素化戦略の採用拡大も、多岐にわたるセクターにおけるブルー水素の利用拡大に寄与しています。ブルー水素の生産プロセスへの炭素回収・貯留(CCS)技術の統合は、産業が炭素削減目標や持続可能性の目標に沿うことを支援しています。長期的な業界の成長は、拡張可能なインフラ開発と、炭素削減技術の継続的な進歩によって支えられると予想されます。さらに、クリーンエネルギーへの移行を促進する政府の支援政策と、天然ガス資源の供給が相まって、この技術のより広範な導入が後押しされています。既存のエネルギーインフラを活用して低炭素水素を生産できることは、排出削減が困難な産業部門において、排出量を削減するための経済的に実現可能な道筋を築いています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 28億米ドル |

| 予測額 | 70億米ドル |

| CAGR | 9.6% |

石油精製セグメントは、精製業務における低炭素水素ソリューションへの需要増加により、2035年までCAGR8.2%で成長すると予測されています。製油所は、脱炭素化の目標を支援し、厳格化する環境規制に準拠するため、よりクリーンな代替燃料への移行を着実に進めています。精製活動全般における産業排出量の削減と持続可能性の向上への注目が高まっていることから、今後数年間でブルー水素技術への需要がさらに強まると予想されます。

2025年時点で、水蒸気メタン改質セグメントは市場シェアの72.4%を占めました。このセグメントは、確立されたインフラ、コスト効率の高い生産能力、および高い水素収率効率により、引き続き業界をリードしています。水蒸気メタン改質施設と統合された炭素回収・貯留(CCS)システムへの投資拡大により、同セグメントの成長はさらに加速すると予想されます。さらに、製油および化学製造業界全体でのブルー水素の広範な活用が、世界の水蒸気メタン改質技術の普及を後押ししています。

米国のブルー水素市場は、2035年までに12億6,000万米ドルに達すると予測されています。北米は、低炭素水素インフラへの投資拡大と戦略的な産業連携に支えられ、2025年の世界のブルー水素市場シェアの約46.9%を占めました。水素・アンモニアの貿易ルートの拡大や、クリーンエネルギーパートナーシップへの注目の高まりが、同地域全体の市場成長に大きく寄与すると予想されます。脱炭素化技術への需要の高まりや、炭素削減イニシアチブに対する強力な政策支援も、北米における業界の見通しを強固なものにしています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム

- 天然ガスのサプライチェーン

- ブルー水素生産インフラ

- CCUSインフラの統合

- 流通・輸送ネットワーク

- エンドユーザーとの連携ポイント

- 規制情勢

- 炭素価格設定メカニズムおよび排出量取引制度

- クリーン水素の基準と認証制度

- CCUSに関する規制およびモニタリング要件

- 輸送・安全規制

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク・課題

- 成長ポテンシャル分析

- ポーターの分析

- PESTLE分析

- コスト構造分析

- 価格動向分析、2022年-2035年

- 過去の価格動向分析

- 価格戦略:事業者タイプ別

- 貿易データ分析

- 輸出入数量・金額の動向

- 主要貿易ルートと関税の影響

- 国境を越えるパイプラインインフラ

- 生産能力・生産情勢

- 設備容量:地域・主要生産者別

- 稼働率・拡張計画

- 新たな機会と動向

- デジタル化とIoTの統合

- 投資分析と将来の見通し

- AIおよび生成AIが市場に与える影響

- AIによる既存ビジネスモデルの変革

- セグメント別の生成AIのユースケースと導入ロードマップ

- リスク、制約、および規制上の考慮事項

第4章 競合情勢

- イントロダクション

- 地域別市場シェア

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

- 競合ポジショニング・マトリックス

- 主な発展

- 合併・買収

- パートナーシップ・提携

- 新製品の発売

- 事業拡大計画と資金調達

- 企業規模のベンチマーク

- ランク分類基準および選定基準

- 売上高、地域、イノベーション別ティア位置付けマトリックス

第5章 市場規模・予測:用途別、2022年-2035年

- 石油精製

- 化学品

- その他

第6章 市場規模・予測:技術別、2022年-2035年

- 水蒸気メタン改質

- オートサーマル改質

- 部分酸化

第7章 市場規模・予測:輸送モード別、2022年-2035年

- パイプライン

- 極低温液体タンカー

第8章 市場規模・予測:地域別、2022年-2035年

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- オマーン

- UAE

- クウェート

- カタール

- 南アフリカ

- ラテンアメリカ

第9章 企業プロファイル

- Air Products and Chemicals, Inc.

- Air Liquide

- Aker Solutions

- Bechtel Corporation

- BP

- CF Industries

- Eni

- Exxon Mobil Corporation

- Equinor

- John Wood Group

- Johnson Matthey

- Linde

- MaireTecnimont

- Saipem

- SK E&S

- Shell

- Saudi Aramco

- Technip Energies

- Topsoe

- thyssenkrupp Industrial Solutions

- Uniper

- Woodside

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 123 Pages

- 納期

- 2~3営業日