|

市場調査レポート

商品コード

1766344

産業用油圧機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Industrial Hydraulic Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 産業用油圧機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月12日

発行: Global Market Insights Inc.

ページ情報: 英文 225 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

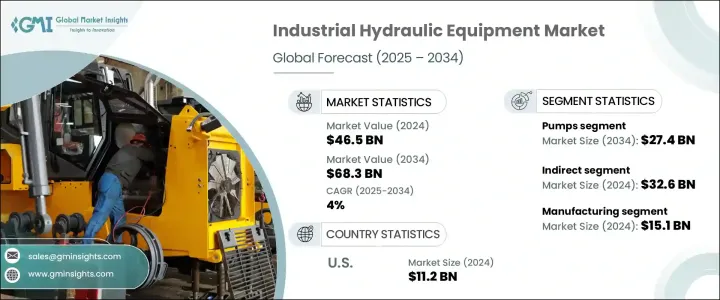

産業用油圧機器の世界市場規模は、2024年に465億米ドルとなり、CAGR 4%で成長し、2034年には683億米ドルに達すると予測されています。

産業施設全体でインダストリー4.0の採用が拡大していることで、油圧システムの統合方法や利用方法に顕著な変化が生じています。センサー、IoT対応モジュール、AIを活用した予測技術などのインテリジェントコンポーネントを組み込むことで、メーカーは油圧システムの運用能力を強化しています。これらの高度なソリューションにより、圧力、温度、流体流量などの重要なパラメータをリアルタイムで追跡できるようになり、予知保全戦略が大幅に改善され、ダウンタイムが最小限に抑えられ、全体的なエネルギー効率が向上します。その結果、最新の電気油圧システムは、完全に自動化された産業用フレームワークの中でシームレスに機能するようになり、油圧はスマート製造業の台頭に不可欠な柱として確立されました。

新興経済諸国では、急速な都市開発により、大型建設機械や土木機械の需要が急増しています。油圧システムはこれらの機械に不可欠であり、過酷な条件下での作業に必要なパワーと制御を提供します。インフラ・プロジェクトが世界的に拡大するにつれて、クレーン、掘削機、掘削システムなどの機器が継続的に必要とされています。これらの機械は、精度、信頼性、耐久性において高性能油圧システムに依存しています。これと並行して、産業界は、エネルギー消費の低減と環境安全性を促進する持続可能な代替手段にますます重点を置くようになっています。この動向は、環境効率の高い油圧ソリューションへの技術革新を促しており、今後数年間で新たな成長の道が開けると期待されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 465億米ドル |

| 予測金額 | 683億米ドル |

| CAGR | 4% |

製品タイプ別に見ると、市場はポンプ、シリンダー、モーター、バルブ、その他に区分されます。このうち、ポンプ分野が最大の金額シェアを占め、2024年には185億米ドルと推定され、2034年には274億米ドルに達すると予測されています。ポンプが広く使用されているのは、機械的エネルギーを油圧力に変換するという基本的な役割に起因しており、これはさまざまな産業用途で不可欠です。組立ラインからリフティングシステムや材料輸送作業に至るまで、ポンプは固定式と移動式の両方の産業機器で流体動力システムのバックボーンとして機能しています。高精度の計量と省エネルギーがますます求められるようになったため、効率と動的制御を改善した可変容量ポンプのような先進技術が開発されるようになりました。

油圧ポンプの安定した需要は、活発な産業環境における定期的なメンテナンスと部品交換サイクルによっても支えられています。古い部品が耐用年数を迎えるにつれて、企業は最新の性能基準に沿った、より新しく効率的な油圧ソリューションへの投資を続けています。ポンプ、シリンダー、モーター、バルブなどを含む広範な製品セグメントは、2024年に326億米ドルに達し、予測期間中にCAGR 3.4%で成長すると予測されています。

この市場の成長に寄与しているもう一つの要因は、間接的な流通チャネルの拡大です。正規ベンダー、専門ディーラー、デジタル・プラットフォームの増加により、多様な業界や地域で製品へのアクセスが向上しています。これらの販売業者は、中核となる油圧製品を、作動油状態監視、ろ過パッケージ、作動油管理システムなどの関連エンジニアリングサービスとバンドルすることが多いです。このオールインワンのアプローチは、調達を簡素化し、顧客との関係を強化します。さらに、現場での技術サポートとリアルタイムの製品デモンストレーションは、産業界のバイヤーの信頼をさらに強化し、販売業者が市場で弾力的かつ競争的なプレゼンスを維持することを可能にしています。

市場を最終用途産業別に分類すると、製造業、建設業、林業・農業、鉱業、石油・ガス、海洋、航空・宇宙、その他となります。製造業は2024年に151億米ドルを占め、2034年までCAGR 4.5%で成長すると予測されています。油圧機器は、特に材料成形、金属成形、高圧機械作業に使用される装置において、製造作業で重要な役割を果たしています。産業界が完全に自動化された生産ラインに移行するにつれ、油圧システムはより高いレベルの応答性、エネルギー管理、一貫性を提供する必要があります。自動化の推進により、正確な制御、サイクルタイムの短縮、運用コストの削減を実現する統合油圧ソリューションへの需要が高まっています。

地域別では、米国が北米産業用油圧機器市場をリードし、2024年の市場規模は112億米ドルで、2034年までのCAGRは3.8%で拡大すると予測されています。同国は強固な産業基盤とインフラ整備への一貫した投資により、地域市場の成長に大きく貢献しています。自動車製造、ビル建設、マテリアルハンドリングなどの業界では、信頼性とインテリジェントな自動化機能を提供する油圧システムへの強い需要が続いています。デジタル制御とスマート電動油圧への重点の高まりは、米国を拠点とする油圧機器サプライヤーの技術革新にさらに拍車をかけており、こうした需要に対応するために事業規模を拡大する動きが加速しています。

市場情勢全体において、各社は技術的に先進的でエネルギー効率が高く、カスタマイズ可能な油圧機器を導入することで、進化する顧客の期待に応えています。インテリジェントな制御機能、IoT接続、予知保全機能を統合することは、現代の産業需要を満たすための中心的な戦略となっています。同時に、世界のエネルギー・排出基準の厳格化により、メーカーはより環境に優しい設計原則の採用を迫られています。競争力を維持するため、企業は製品ラインを多様化するだけでなく、戦略的提携や買収を行い、モバイルや産業オートメーションの専門分野で存在感を高めています。この継続的なシフトは市場を再形成し、よりインテリジェントで効率的、かつ環境に配慮した油圧システムへと舵を切っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 機会

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 規制の枠組み

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーターのファイブフォース分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ航空

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- パンプス

- シリンダー

- モーター

- バルブ

- その他

第6章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 製造業

- 建設

- 林業と農業

- 鉱業

- 石油・ガス

- 海洋

- 航空宇宙および航空

- その他

第7章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接

- 間接

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第9章 企業プロファイル

- Bosch Rexroth

- Bucher Hydraulics

- Caterpillar

- Danfoss

- Eaton

- HAWE Hydraulik

- Hitachi Construction Machinery

- HYDAC International

- Kawasaki Heavy Industries

- Komatsu

- KTI Hydraulics

- KYB

- Liebherr-International

- Mitsubishi Heavy Industries

- Parker-Hannifin

The Global Industrial Hydraulic Equipment Market was valued at USD 46.5 billion in 2024 and is estimated to grow at a CAGR of 4% to reach USD 68.3 billion by 2034. The growing adoption of Industry 4.0 across industrial facilities is driving a notable shift in how hydraulic systems are integrated and utilized. By incorporating intelligent components such as sensors, IoT-enabled modules, and AI-powered predictive technologies, manufacturers are enhancing the operational capabilities of hydraulic systems. These advanced solutions enable real-time tracking of essential parameters, including pressure, temperature, and fluid flow, which significantly improves predictive maintenance strategies, minimizes downtime, and boosts overall energy efficiency. As a result, modern electro-hydraulic systems now function seamlessly within fully automated industrial frameworks, establishing hydraulics as an essential pillar in the rise of smart manufacturing.

In emerging economies, rapid urban development is fueling a surge in demand for heavy-duty construction and earth-moving machinery. Hydraulic systems are indispensable in these machines, delivering the power and control required for operations under extreme conditions. As infrastructure projects expand globally, there is a continuous need for equipment such as cranes, excavators, and drilling systems. These machines depend on high-performance hydraulic systems for precision, reliability, and durability. In parallel, industries are increasingly focusing on sustainable alternatives that promote lower energy consumption and environmental safety. This trend is prompting innovation toward eco-efficient hydraulic solutions, which is expected to unlock new growth avenues in the years ahead.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $46.5 Billion |

| Forecast Value | $68.3 Billion |

| CAGR | 4% |

By product type, the market is segmented into pumps, cylinders, motors, valves, and others. Among these, the pump segment held the largest value share, estimated at USD 18.5 billion in 2024, and is projected to reach USD 27.4 billion by 2034. The widespread use of pumps stems from their fundamental role in converting mechanical energy into hydraulic power, which is vital across a variety of industrial applications. From assembly lines to lifting systems and material transport operations, pumps serve as the backbone of fluid power systems in both fixed and mobile industrial equipment. The increasing push for high-precision metering and energy conservation has led to the development of advanced technologies such as variable displacement pumps, which offer improved efficiency and dynamic control.

Consistent demand for hydraulic pumps is also supported by routine maintenance and part replacement cycles in active industrial environments. As older components reach the end of their service lives, businesses continue to invest in newer, more efficient hydraulic solutions that align with modern performance standards. The broader product segment, encompassing pumps, cylinders, motors, valves, and others, reached USD 32.6 billion in 2024 and is anticipated to grow at a CAGR of 3.4% during the forecast period.

Another factor contributing to the growth of this market is the expansion of indirect distribution channels. A growing number of authorized vendors, specialized dealers, and digital platforms are enhancing product accessibility across diverse industries and geographies. These distributors often bundle core hydraulic products with related engineering services such as fluid condition monitoring, filtration packages, and hydraulic fluid management systems. This all-in-one approach simplifies procurement and strengthens customer relationships. Additionally, on-ground technical support and real-time product demonstrations further reinforce confidence among industrial buyers, enabling distributors to maintain a resilient and competitive market presence.

When segmented by end-use industry, the market includes manufacturing, construction, forestry and agriculture, mining, oil and gas, marine, aerospace and aviation, and others. The manufacturing sector accounted for USD 15.1 billion in 2024 and is projected to grow at a CAGR of 4.5% through 2034. Hydraulics play a critical role in manufacturing operations, particularly in equipment used for material forming, metal shaping, and high-pressure mechanical tasks. As industries move toward fully automated production lines, hydraulic systems must deliver higher levels of responsiveness, energy management, and consistency. The push for automation has increased the demand for integrated hydraulic solutions that provide precise control, reduced cycle times, and lower operational costs.

Regionally, the United States led the North America industrial hydraulic equipment market, which was valued at USD 11.2 billion in 2024 and is forecast to expand at a CAGR of 3.8% through 2034. The country's robust industrial base and consistent investment in infrastructure development have made it a key contributor to regional market growth. Industries such as automotive manufacturing, building construction, and material handling continue to generate strong demand for hydraulic systems that offer reliability and intelligent automation features. The growing emphasis on digital control and smart electro-hydraulics is further fueling innovation across U.S.-based hydraulic equipment suppliers, who are increasingly scaling their operations to meet this demand.

Across the market landscape, companies are responding to evolving customer expectations by introducing technologically advanced, energy-efficient, and customizable hydraulic equipment. Integrating intelligent control features, IoT connectivity, and predictive maintenance capabilities has become a central strategy for meeting modern industrial demands. At the same time, stricter global energy and emissions standards are compelling manufacturers to adopt greener design principles. To stay competitive, businesses are not only diversifying their product lines but also forming strategic partnerships and acquisitions to expand their presence in specialized segments of mobile and industrial automation. This ongoing shift is reshaping the market, steering it toward more intelligent, efficient, and environmentally responsible hydraulic systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 End use industry

- 2.2.4 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory framework

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's five forces analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 MEA

- 4.2.1.5 LATAM

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Pumps

- 5.3 Cylinder

- 5.4 Motors

- 5.5 Valves

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By End Use Industry, 2021-2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Manufacturing

- 6.3 Construction

- 6.4 Forestry & agriculture

- 6.5 Mining

- 6.6 Oil & Gas

- 6.7 Marine

- 6.8 Aerospace & aviation

- 6.9 Others

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021-2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Direct

- 7.3 Indirect

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034, ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 The U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 South Africa

Chapter 9 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 9.1 Bosch Rexroth

- 9.2 Bucher Hydraulics

- 9.3 Caterpillar

- 9.4 Danfoss

- 9.5 Eaton

- 9.6 HAWE Hydraulik

- 9.7 Hitachi Construction Machinery

- 9.8 HYDAC International

- 9.9 Kawasaki Heavy Industries

- 9.10 Komatsu

- 9.11 KTI Hydraulics

- 9.12 KYB

- 9.13 Liebherr-International

- 9.14 Mitsubishi Heavy Industries

- 9.15 Parker-Hannifin