|

市場調査レポート

商品コード

1766339

大腸がん診断の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Colorectal Cancer Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 大腸がん診断の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月03日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

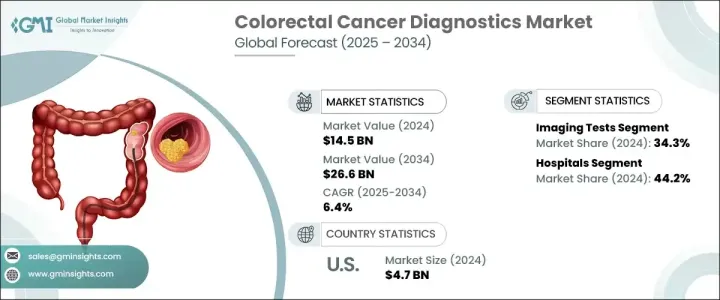

大腸がん診断の世界市場規模は、2024年に145億米ドルとなり、CAGR 6.4%で成長し、2034年には266億米ドルに達すると推定されます。

市場成長の原動力は、大腸がんの罹患率の増加、早期スクリーニングのための公衆衛生イニシアチブの高まり、診断モダリティにおける継続的な技術進歩です。リキッドバイオプシー、AI支援画像診断、便ベースのDNA検査などの革新は、大腸がん検出の展望を再構築し、侵襲性が低く、より正確で、患者に優しい診断オプションを提供しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 145億米ドル |

| 予測金額 | 266億米ドル |

| CAGR | 6.4% |

定期的なCRC検診の推奨年齢を45歳に引き下げるなど、啓発キャンペーンや検診ガイドラインの更新が進み、早期診断率に寄与しています。さらに、世界人口の高齢化と、座りがちな生活や食習慣といった生活習慣の要因が相まって、大腸がんの世界の負担が増大しており、効果的で利用しやすい診断法の緊急の必要性が浮き彫りになっています。世界中の政府やヘルスケア機関が、大腸がん検診へのアクセスを改善するための大規模なイニシアチブを開始する一方、非公開会社は次世代診断ツールを市場に投入するために研究開発に多額の投資を行っています。人工知能、次世代シーケンシング(NGS)、マイクロ流体技術は、診断精度と患者の転帰を大幅に向上させる態勢を整えています。

大腸がん診断市場は主に検査タイプ別に区分され、画像検査セグメントが2024年に34.3%のシェアを占める。CTコロノグラフィ、MRI、PETスキャンなどの画像検査モダリティは、早期発見、病期分類、治療計画のために依然として極めて重要です。AIを活用した画像診断の採用により検出精度が向上し、前がん病変の早期発見に役立っています。さらに、画像検査は非侵襲性または低侵襲性であるため、患者の受け入れと検診率の向上が続いています。

エンドユーザー別では、病院セグメントが2024年に44.2%のシェアを占め、大腸がん診断の主要エンドユーザーとしての地位を固めています。病院は大腸がんの発見、診断、病期分類、治療計画の主要なセンターであり、高度な画像診断システム、分子病理検査室、内視鏡機器、外科腫瘍学ユニットなどを含む包括的な診断インフラによって支えられています。腫瘍内科医、放射線科医、病理医、消化器内科医、外科医を結集した集学的アプローチにより、早期発見から治療後の経過観察まで、大腸がん患者のケアをシームレスにコーディネートすることが可能です。

北米大腸がん診断市場は2024年に35.2%のシェアを占めました。同地域の優位性は、強固なヘルスケアインフラ、スクリーニングプログラムの広範な実施、AI対応大腸内視鏡検査、リキッドバイオプシー、分子バイオマーカー検査などの高度診断技術の高い採用率に起因します。米国では、CDCによる大腸がん対策プログラム(CRCCP)のような取り組みが、特に十分なサービスを受けていない人々の早期検診率の向上に役立っています。

Abbott Laboratories、Exact Sciences Corporation、Siemens Healthineers AG、Guardant Health Inc.、F-Hoffmann-La Roche Ltd.、GE HealthCare Technologies, Inc.などの主要な市場プレーヤーは、リキッドバイオプシー、AI主導の画像診断、分子診断の革新を通じて診断ポートフォリオの拡大に多額の投資を行っています。戦略的パートナーシップ、M&A、新製品の規制当局による承認は、これらの企業が世界のプレゼンスを強化し、将来の市場成長を促進するために引き続き重要な戦略です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 大腸がんの発生率と有病率の増加

- がん検診に関する政府の取り組みと政策

- がん診断分野における技術の進歩

- 早期診断に関する意識の高まり

- 業界の潜在的リスク&課題

- 診断検査と処置の高コスト

- 診断検査に対する償還ポリシーの欠如

- 市場機会

- 非侵襲性およびAI駆動型診断技術の拡大と導入

- 新興地域における急速な市場成長

- 促進要因

- 将来の市場動向

- 償還シナリオ

- 消費者行動分析

- 成長可能性分析

- テクノロジーの情勢

- 規制情勢

- ギャップ分析

- 特許分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:検査タイプ別、2021年~2034年

- 主要動向

- 血液検査

- 便検査

- 便潜血検査(FOBT)

- 便中バイオマーカー検査

- CRC DNAスクリーニング検査

- 画像検査

- CT

- 超音波

- MRI

- PET

- 大腸内視鏡検査

- その他の画像検査

- 生検

- その他の検査タイプ

第6章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 画像診断センター

- がん研究センター

- その他の用途

第7章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- Abbott Laboratories

- Danaher Corporation

- DiaCarta

- Exact Sciences Corporation

- F-Hoffmann-La Roche

- GE HealthCare Technologies

- Geneoscopy

- Guardant Health

- H.U. Group Holdings

- New Day Diagnostics

- Olympus Corporation

- Phase Scientific International

- QIAGEN N.V.

- Siemens Healthineers

- Sysmex Corporation

- Thermo Fisher Scientific

The Global Colorectal Cancer Diagnostics Market was valued at USD 14.5 billion in 2024 and is estimated to grow at a CAGR of 6.4% to reach USD 26.6 billion by 2034.

The market growth is driven by the increasing incidence of colorectal cancer, rising public health initiatives for early screening, and continuous technological advancements in diagnostic modalities. Innovations such as liquid biopsy, AI-assisted imaging, and stool-based DNA tests are reshaping the landscape of colorectal cancer detection, offering less invasive, more accurate, and patient-friendly diagnostic options.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.5 Billion |

| Forecast Value | $26.6 Billion |

| CAGR | 6.4% |

Growing awareness campaigns and updated screening guidelines, such as lowering the recommended age for routine CRC screening to 45, contribute to early diagnosis rates. Furthermore, an aging global population, combined with lifestyle factors like sedentary behavior and dietary habits, has heightened the global burden of colorectal cancer, underscoring the urgent need for effective and accessible diagnostics. Governments and healthcare organizations worldwide are launching large-scale initiatives to improve access to colorectal cancer screening, while private companies are investing heavily in R&D to bring next-generation diagnostic tools to the market. Artificial intelligence, next-generation sequencing (NGS), and microfluidic technologies are poised to enhance diagnostic precision and patient outcomes significantly.

The colorectal cancer diagnostics market is primarily segmented by test type, with the imaging tests segment holding 34.3% share in 2024. Imaging modalities such as CT colonography, MRI, and PET scans remain crucial for early detection, staging, and treatment planning. Adopting AI-enhanced imaging has improved detection accuracy, helping to identify precancerous lesions at earlier stages. Moreover, imaging tests' non-invasive or minimally invasive nature continues to drive patient acceptance and screening rates.

In terms of end-use, the hospitals segment held 44.2% share in 2024, solidifying its position as the leading end-user for colorectal cancer diagnostics. Hospitals are the primary centers for colorectal cancer detection, diagnosis, staging, and treatment planning, supported by a comprehensive diagnostic infrastructure that includes advanced imaging systems, molecular pathology labs, endoscopic equipment, and surgical oncology units. Their multidisciplinary approach-bringing together oncologists, radiologists, pathologists, gastroenterologists, and surgeons-enables the seamless coordination of care for colorectal cancer patients, from early detection through post-treatment monitoring.

North America Colorectal Cancer Diagnostics Market held a 35.2% share in 2024. The region's dominance stems from a robust healthcare infrastructure, widespread implementation of screening programs, and high adoption rates of advanced diagnostic technologies, such as AI-enabled colonoscopy, liquid biopsies, and molecular biomarker testing. In the United States, initiatives like the Colorectal Cancer Control Program (CRCCP) by the CDC have been instrumental in increasing early screening rates, particularly among underserved populations.

Key market players such as Abbott Laboratories, Exact Sciences Corporation, Siemens Healthineers AG, Guardant Health Inc., F-Hoffmann-La Roche Ltd., and GE HealthCare Technologies, Inc. are heavily investing in expanding their diagnostic portfolios through innovations in liquid biopsy, AI-driven imaging, and molecular diagnostics. Strategic partnerships, mergers and acquisitions, and regulatory approvals for new products remain crucial strategies for these players to strengthen their global presence and drive future market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Test type

- 2.2.2 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence and prevalence of colorectal cancer

- 3.2.1.2 Government initiatives and policies associated with cancer screening tests

- 3.2.1.3 Technological advancements in field of cancer diagnostics

- 3.2.1.4 Growing awareness regarding early diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of diagnostic tests and procedures

- 3.2.2.2 Lack of reimbursement policies for diagnostic tests

- 3.2.3 Market Opportunities

- 3.2.3.1 Expansion and Adoption of Non-Invasive and AI-Driven Diagnostic Technologies

- 3.2.3.2 Rapid Market Growth in Emerging Regions

- 3.2.1 Growth drivers

- 3.3 Future market trends

- 3.4 Reimbursement scenario

- 3.5 Consumer behaviour analysis

- 3.6 Growth potential analysis

- 3.7 Technology landscape

- 3.8 Regulatory landscape

- 3.9 Gap analysis

- 3.10 Patent analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Blood tests

- 5.3 Stool tests

- 5.3.1 Fecal occult blood test (FOBT)

- 5.3.2 Fecal biomarker test

- 5.3.3 CRC DNA screening test

- 5.4 Imaging tests

- 5.4.1 CT

- 5.4.2 Ultrasound

- 5.4.3 MRI

- 5.4.4 PET

- 5.4.5 Colonoscopy

- 5.4.6 Other imaging tests

- 5.5 Biopsy

- 5.6 Other test types

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Diagnostic imaging centers

- 6.4 Cancer research centers

- 6.5 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott Laboratories

- 8.2 Danaher Corporation

- 8.3 DiaCarta

- 8.4 Exact Sciences Corporation

- 8.5 F-Hoffmann-La Roche

- 8.6 GE HealthCare Technologies

- 8.7 Geneoscopy

- 8.8 Guardant Health

- 8.9 H.U. Group Holdings

- 8.10 New Day Diagnostics

- 8.11 Olympus Corporation

- 8.12 Phase Scientific International

- 8.13 QIAGEN N.V.

- 8.14 Siemens Healthineers

- 8.15 Sysmex Corporation

- 8.16 Thermo Fisher Scientific