加齢黄斑変性の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Age-related Macular Degeneration Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 142 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766323

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

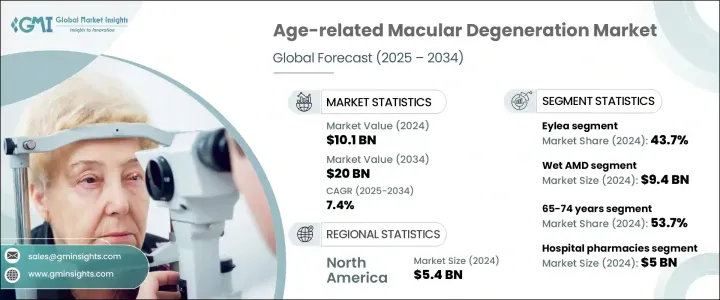

加齢黄斑変性(AMD)の世界市場規模は、2024年に101億米ドルとなり、CAGR 7.4%で成長し、2034年には200億米ドルに達すると推定されます。

市場成長の原動力は、AMDの有病率の上昇、世界人口の高齢化、認知度の向上と早期診断、治療オプションの継続的な革新です。AMDは、50歳以上の高齢者が罹患する進行性の眼疾患であり、中心視力の低下を招き、生活の質に大きな影響を与えます。AMDは、主に50歳以上の人が罹患する進行性の眼疾患であり、不可逆的な中心視力の低下を招き、読書、運転、顔の認識などの日常生活を著しく損ない、最終的には生活の質全体に影響を及ぼします。

病気が進行すると、網膜の黄斑部(シャープな中心視力をつかさどる部分)が侵され、視野がぼやけたり暗くなったりします。このような自立心の喪失は、特に高齢者において、不安、抑うつ、社会的孤立などの心理的影響を引き起こすことが多いです。AMDの負担増は世界の高齢化の動向と密接に関連しており、その有病率は65歳以上の人口で急激に増加しています。この疾患は、喫煙、高血圧、肥満、遺伝的素因、食生活の乱れといった他の危険因子とも関連しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 101億米ドル |

| 予測金額 | 200億米ドル |

| CAGR | 7.4% |

疾患タイプ別では、湿性AMDが2024年に94億米ドルの市場規模を占め、その原動力となったのは、疾患の進行を止め、網膜液貯留を最小限に抑え、視機能を維持する効果が実証されている抗VEGF療法の広範な採用でした。Eylea、Lucentis、Beovuのような薬剤の成功により、湿性AMDは最も積極的に治療される疾患として位置づけられています。一方、ドライ型AMDは、これまで承認された薬理学的介入がなかったが、現在、臨床的に再び注目されています。ドライ型AMDの重症型である地理的萎縮症に対する初のFDA承認治療薬であるSyfovreの発売は、補体経路阻害薬や遺伝子治療薬の有望なパイプラインとともに、この分野の治療における変革の兆しを示しています。

Eylea、Lucentis、Vabysmoなどの抗VEGF療法は、AMD治療の要となっています。このうち、注射間隔の延長と視力の維持に有効なEyleaのシェアは43.7%です。同剤の最新製剤であるアイリーアHDは、患者の服薬アドヒアランスを向上させ、治療負担を軽減する投与スケジュールの延長により、さらなる支持を集めています。Vabysmoのような新規参入企業は、二重経路阻害(VEGF-A+Ang-2)により急速に市場シェアを拡大し、血管の不安定性に対処し、臨床転帰を向上させています。

北米の加齢黄斑変性市場2025-2034年のCAGRは7%で、強固なヘルスケアインフラ、革新的な治療法の早期導入、支持的な規制の枠組みが市場を牽引します。高い診断率は、OCTのような高度な画像技術へのアクセスの普及と予防的眼科医療への関心の高まりによってさらに支えられています。乾燥AMDに対する光バイオモジュレーションなど、新規の非侵襲的治療法が最近FDAに承認されたことは、患者の嗜好に合致し、長期的なアドヒアランスを向上させる、より負担の少ない治療法への地域的なシフトを裏付けるものです。

加齢黄斑変性市場での地位を強化するため、Xbrane Biopharma AB、Pfizer Inc.、Formycon AG、Celltrion, Inc.、Novartis AG、Amgen Inc.、Sandoz Group AG、Apellis Pharmaceuticals, Inc.、STADA Arzneimittel AG、F. Hoffmann-La Roche Ltd.、Biocon Biologics Limited、Regeneron Pharmaceuticals Inc.、Bayer AG、Biogen, Inc.などの企業は、研究開発投資、バイオシミラー開発、長時間作用型製剤などの戦略的イニシアチブを採用しています。リジェネロンによるEylea HDの発売やロシュによるVabysmoの導入は、イノベーション主導の競合を実証しています。各社はまた、臨床試験のためのCROとの提携や、実データ収集のためのデジタルツールの活用を通じて事業を拡大しています。世界のマーケットリーダーは、ポートフォリオを多様化するために、遺伝子治療薬、二重経路阻害薬、補体標的薬に注力しています。さらに、価格戦略、戦略的ライセンシング、規制当局との提携により、より迅速な市場アクセスが可能となっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 加齢黄斑変性(AMD)の普及率の上昇

- 高齢化人口の増加

- 治療選択肢の進歩

- 意識の向上と早期診断

- 業界の潜在的リスク&課題

- 治療費が高め

- 硝子体内注射による合併症のリスク

- 促進要因

- 成長可能性分析

- 規制情勢

- 米国

- 欧州(英国を除く)

- 英国

- インド

- ブラジル

- 中国

- テクノロジーの情勢

- コア技術

- 隣接技術

- 将来の市場動向

- 特許分析

- パイプライン分析

- 臨床試験の情勢

- 承認された治療法

- 臨床試験中の新興バイオシミラー

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 競争市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- アイレア

- ルセンティス

- ベオヴ

- ヴァビスモ

- シフォヴレ

- アバスチン

- その他の製品

第6章 市場推計・予測:病気の種類別、2021年~2034年

- 主要動向

- 湿性AMD

- 乾燥AMD

第7章 市場推計・予測:年齢別、2021年~2034年

- 主要動向

- 50~64歳

- 65~74歳

- 75歳以上

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 病院薬局

- 専門薬局および小売薬局

- eコマース

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Amgen

- Apellis Pharmaceuticals

- Bayer

- Biocon Biologics

- Biogen

- Celltrion

- F. Hoffmann-La Roche

- Formycon

- Novartis

- Pfizer

- Regeneron Pharmaceuticals

- Sandoz Group

- STADA Arzneimittel

- Xbrane Biopharma

目次

The Global Age-related Macular Degeneration Market was valued at USD 10.1 billion in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 20 billion by 2034. The market growth is driven by a rising prevalence of AMD, an aging global population, increased awareness and early diagnosis, and ongoing innovations in treatment options. AMD is a progressive eye condition affecting individuals aged 50 and above, leading to central vision loss and significantly impacting quality of life. AMD is a progressive eye condition that primarily affects individuals aged 50 and above, leading to irreversible central vision loss and significantly impairing daily activities such as reading, driving, and recognizing faces, ultimately impacting the overall quality of life.

As the disease advances, it compromises the macula-the part of the retina responsible for sharp, central vision-resulting in blurred or dark spots in the visual field that cannot be corrected with glasses or contact lenses. This loss of independence often contributes to psychological effects such as anxiety, depression, and social isolation, especially among older adults. The growing burden of AMD is closely tied to the global aging trend, with its prevalence sharply increasing in populations over 65. The disease is also associated with other risk factors such as smoking, hypertension, obesity, genetic predisposition, and poor dietary habits-factors that are becoming more prevalent globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.1 Billion |

| Forecast Value | $20 Billion |

| CAGR | 7.4% |

By disease type, wet AMD dominated the market with USD 9.4 billion in 2024, driven by the widespread adoption of anti-VEGF therapies, which have proven effective in halting disease progression, minimizing retinal fluid accumulation, and preserving visual function. The success of agents like Eylea, Lucentis, and Beovu has positioned wet AMD as the most actively treated form of the disease. Meanwhile, dry AMD, historically lacking approved pharmacologic interventions, is now seeing renewed clinical focus. The launch of Syfovre, the first FDA-approved treatment for geographic atrophy (a severe form of dry AMD), along with a promising pipeline of complement pathway inhibitors and gene therapies, signals a transformative shift in managing this segment.

Anti-VEGF therapies such as Eylea, Lucentis, and Vabysmo have become the cornerstone of AMD treatment. Among these, the Eylea segment held 43.7% share owing to its efficacy in extending injection intervals and maintaining visual acuity. The drug's updated formulation, Eylea HD, is gaining further traction by offering extended dosing schedules that improve patient adherence and reduce treatment burden. New entrants like Vabysmo are rapidly gaining market share through dual-pathway inhibition (VEGF-A + Ang-2), addressing vascular instability and offering enhanced clinical outcomes.

North America Age-related Macular Degeneration Market will grow at a CAGR of 7% during 2025-2034, driven by robust healthcare infrastructure, early adoption of innovative therapies, and supportive regulatory frameworks. High diagnosis rates are further supported by widespread access to advanced imaging technologies such as OCT and an increasing focus on preventative eye care. Recent FDA approvals of novel, non-invasive therapies such as photobiomodulation for dry AMD underscore a regional shift toward less burdensome treatment modalities, aligning with patient preferences and improving long-term adherence.

To strengthen their position in the Age-related Macular Degeneration Market, companies like Xbrane Biopharma AB, Pfizer Inc., Formycon AG, Celltrion, Inc., Novartis AG, Amgen Inc., Sandoz Group AG, Apellis Pharmaceuticals, Inc., STADA Arzneimittel AG, F. Hoffmann-La Roche Ltd., Biocon Biologics Limited, Regeneron Pharmaceuticals Inc., Bayer AG, Biogen, Inc. are adopting strategic initiatives including R&D investments, biosimilar development, and long-acting formulations. Regeneron's launch of Eylea HD and Roche's introduction of Vabysmo demonstrate innovation-driven competition. Companies are also expanding through partnerships with CROs for clinical trials and leveraging digital tools for real-world data collection. Global market leaders focus on gene therapies, dual-pathway inhibitors, and complement-targeting drugs to diversify their portfolios. Additionally, pricing strategies, strategic licensing, and regulatory collaborations enable faster market access.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Market size estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.5 Forecast model

- 1.6 Data mining sources

- 1.6.1 Global

- 1.6.2 Regional/Country

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 End Use

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of age-related macular degeneration (AMD)

- 3.2.1.2 Growth in aging population

- 3.2.1.3 Advancements in treatment options

- 3.2.1.4 Increased awareness and early diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Risk of complications from intravitreal injections

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe (excluding UK)

- 3.4.3 UK

- 3.4.4 India

- 3.4.5 Brazil

- 3.4.6 China

- 3.5 Technology landscape

- 3.5.1 Core technologies

- 3.5.2 Adjacent technologies

- 3.6 Future market trends

- 3.7 Patent analysis

- 3.8 Pipeline analysis

- 3.9 Clinical trial landscape

- 3.9.1 Approved therapies

- 3.9.2 Emerging biosimilars under clinical trials

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Eylea

- 5.3 Lucentis

- 5.4 Beovu

- 5.5 Vabysmo

- 5.6 Syfovre

- 5.7 Avastin

- 5.8 Other products

Chapter 6 Market Estimates and Forecast, By Disease Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Wet AMD

- 6.3 Dry AMD

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 50–64 years

- 7.3 65–74 years

- 7.4 75 and above

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Specialty and retail pharmacies

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 China

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.4 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amgen

- 10.2 Apellis Pharmaceuticals

- 10.3 Bayer

- 10.4 Biocon Biologics

- 10.5 Biogen

- 10.6 Celltrion

- 10.7 F. Hoffmann-La Roche

- 10.8 Formycon

- 10.9 Novartis

- 10.10 Pfizer

- 10.11 Regeneron Pharmaceuticals

- 10.12 Sandoz Group

- 10.13 STADA Arzneimittel

- 10.14 Xbrane Biopharma

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 142 Pages

- 納期

- 2~3営業日