|

市場調査レポート

商品コード

1766322

動物用人工授精の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Animal Artificial Insemination Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 動物用人工授精の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月12日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

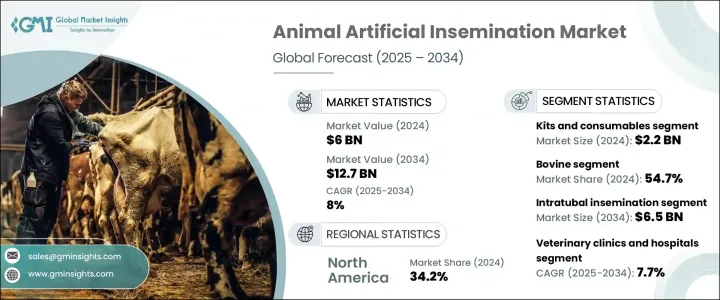

世界の動物用人工授精市場は、2024年には60億米ドルと評価され、CAGR 8%で成長し、2034年には127億米ドルに達すると推定されています。

この成長の原動力となっているのは、遺伝的改良への注目の高まり、より高品質な家畜への需要の高まり、発展途上地域における高度な繁殖ソリューションの普及です。世界人口が増加の一途をたどるなか、食肉や乳製品の需要増に対応するために効率的な家畜生産が必要とされています。人工授精(AI)は生殖補助法のひとつであり、家畜の繁殖能力と生産性を向上させることで、こうしたニーズに応える上でますます重要になってきています。

世界の多くの地域で、畜産家は牛群の質を向上させるためだけでなく、繁殖関連コストを削減し、生産性を高めるためにもAIに注目しています。選択的育種を可能にすることで、AIは耐病性、乳量、肉質といった望ましい遺伝形質を高めるのに役立ち、現代の家畜管理に不可欠な要素となっています。市場の拡大は、獣医ヘルスケア産業への投資の増加や、管理された育種技術の長期的な利点に対する農家の意識の高まりによってさらに影響を受けています。さらに、人工授精と獣医学的サービスの統合は、精密育種ツールの継続的な開発とともに、人工授精手順の有効性と信頼性を高め、種や地域を問わずその普及を促しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 60億米ドル |

| 予測金額 | 127億米ドル |

| CAGR | 8% |

製品タイプ別では、2024年にキット・消耗品分野が22億米ドルの評価額で市場をリードしました。人工授精用ピペット、ストロー、手袋、カテーテルなどの消耗品は頻繁に使用されるため、すべてのAIサイクルに不可欠な部品となり、旺盛な需要を牽引しています。資本集約的な機器とは異なり、これらの製品は一貫した補充を必要とするため、市場全体の収益に大きく貢献しています。これらの製品は回転率が高く、臨床と牧場の両方で必要であるため、市場での優位性がさらに強化されています。

動物の種類別では、ウシ・セグメントが2024年の総市場シェアの54.7%を占め、トップシェアに浮上しました。このセグメントは、乳製品と牛肉製品に対する世界の大きな需要から利益を得ており、これが牛の繁殖における人工授精技術の大規模な導入につながっています。牛群の遺伝子を改善し、乳量や耐病性などの形質を向上させることに一貫して重点が置かれているため、人工授精はこの分野で好まれる手法となっています。大規模な牛の個体数と組織化された酪農事業が、このセグメントのトップシェアにさらに貢献しています。

技術別では、卵管内人工授精の分野が力強い成長を遂げ、2034年までに65億米ドルに達すると予測されています。この技術では、精液を卵管に直接注入するため、特に従来のアプローチが有効でない場合に受精の成功率が向上します。カテーテルの設計と人工授精用具の進歩により、この方法の利用しやすさと精度が向上しており、高い繁殖効率を目指す育種家による採用が増加しています。

最終用途別に分析すると、2024年には動物病院とクリニックが最大のシェアを占め、2034年までCAGR 7.7%で成長すると予想されます。これらの施設は生殖に特化したサービスを提供しており、最新の医療機器と熟練した獣医スタッフに助けられ、複雑な処置にも対応できることから、AIエコシステムの重要な一部となっています。不妊治療に対する意識の高まりと、専門家による治療に対する嗜好の高まりも、こうした施設の存在感を高めています。

地域別では、北米が2024年の世界市場を34.2%のシェアでリードしています。米国だけが2024年に18億7,000万米ドルを占め、2023年の17億9,000万米ドルから成長しました。この成長は、同国の高度な獣医学インフラと、高い家畜生産性を支える近代的育種技術の強力な導入を反映しています。

競合情勢は、確立された世界企業と小規模な地域企業が混在していることが特徴です。IMV Technologies、Genus Plc、URUS Group、CRV Holdings B.V.の大手4社は、2024年時点で世界市場の約48%を占めています。これらの企業は、競争力を維持するため、製品革新、技術アップグレード、戦略的提携に多額の投資を行っています。一方、現地メーカーは、コスト効率の高いソリューションを提供し、合併や製品投入を通じて地理的プレゼンスを拡大することで、競合の激化を続けています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 自然交配に比べて高い繁殖効率を求める声が高まる

- 家畜とペットの両方における遺伝子強化の需要の増加

- 精液採取および保存技術の技術的進歩

- 動物における性感染症の蔓延

- 業界の潜在的リスク&課題

- 手術の失敗や合併症のリスク

- 熟練技術者の不足

- 規制と倫理上の懸念

- セットアップと設備のコストが高め

- 市場機会

- 家畜の遺伝的改良に対する需要の高まり

- 新興諸国における人工知能の導入拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- サービス

- 精液

- 正常な精液

- 性別判定精液

- 機器

- キットと消耗品

第6章 市場推計・予測:動物の種類別、2021年~2034年

- 主要動向

- 牛

- 豚

- 羊

- ヤギ

- 馬

- その他の動物の種類

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 卵管内人工授精

- 子宮内人工授精

- 子宮頸管内授精

- 子宮内卵管腹膜授精

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 獣医クリニックと病院

- 動物飼育センター

- 調査機関および大学

- その他の用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Bovine Elite

- CRV Holdings

- Geno SA

- Genus Plc

- IMV Technologies

- Minitube Group

- SEMEX

- Select Sires

- Swine Genetics International

- Shipley Swine Genetics

- Stallion AI Services

- STgenetics

- URUS Group

- VikingGenetics

The Global Animal Artificial Insemination Market was valued at USD 6 billion in 2024 and is estimated to grow at a CAGR of 8% to reach USD 12.7 billion by 2034. This growth is being driven by a rising focus on genetic improvement, increased demand for higher quality livestock, and the widespread adoption of advanced reproductive solutions across developing regions. As the global population continues to grow, so does the need for efficient livestock production to meet escalating demands for meat and dairy products. Artificial insemination (AI), as a method of assisted reproduction, is becoming increasingly important in meeting these needs by enhancing the reproductive performance and productivity of animals.

In many parts of the world, livestock breeders are turning to AI not only to improve herd quality but also to reduce breeding-related costs and boost productivity. By enabling selective breeding, AI helps increase desirable genetic traits such as disease resistance, milk yield, and meat quality, which makes it a vital component of modern livestock management practices. Market expansion is further influenced by the rising investments in the veterinary healthcare industry and the growing awareness among farmers about the long-term benefits of controlled breeding techniques. Additionally, the integration of AI with veterinary services, along with the continuous development of precision breeding tools, is enhancing the effectiveness and reliability of artificial insemination procedures, encouraging its widespread use across species and regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6 Billion |

| Forecast Value | $12.7 Billion |

| CAGR | 8% |

In terms of product type, in 2024, the kits and consumables segment led the market with a valuation of USD 2.2 billion. The frequent use of consumables like insemination pipettes, straws, gloves, and catheters makes them essential components in every AI cycle, driving strong demand. Unlike capital-intensive equipment, these products require consistent replenishment, thereby contributing significantly to overall market revenue. Their high turnover rate and necessity in both clinical and farm settings further reinforce their dominant position in the market.

By animal type, the bovine segment emerged as the top contributor, accounting for 54.7% of the total market share in 2024. This segment benefits from the substantial global demand for dairy and beef products, which has led to the large-scale adoption of artificial insemination techniques in cattle breeding. The consistent emphasis on improving herd genetics and enhancing traits like milk production and disease resistance has made AI a preferred method in this segment. Large cattle populations and organized dairy operations further contribute to the segment's leading share.

Based on technique, the intratubal insemination segment is projected to witness strong growth, reaching USD 6.5 billion by 2034. This technique involves placing semen directly into the fallopian tubes, allowing for improved fertilization success, especially in cases where conventional approaches may not be as effective. Advances in catheter design and insemination tools are enhancing the accessibility and precision of this method, increasing its adoption among breeders aiming for high reproductive efficiency.

When analyzed by end use, in 2024, veterinary clinics and hospitals held the largest share and are expected to grow at a 7.7% CAGR through 2034. These facilities provide specialized reproductive services, and their ability to handle complex procedures, aided by modern medical equipment and skilled veterinary staff, makes them an essential part of the AI ecosystem. Increased awareness of fertility management and the rising preference for professional care also contribute to their strong market presence.

Regionally, North America led the global market in 2024 with a 34.2% share. The United States alone accounted for USD 1.87 billion in 2024, growing from USD 1.79 billion in 2023. This growth reflects the country's advanced veterinary infrastructure and its strong adoption of modern breeding technologies, which support high livestock productivity.

The competitive landscape of the animal artificial insemination market is characterized by the presence of a mix of established global companies and smaller regional firms. Four leading players- IMV Technologies,Genus Plc, URUS Group, and CRV Holdings B.V.-collectively held around 48% of the global market in 2024. These companies are heavily investing in product innovation, technological upgrades, and strategic collaborations to maintain their competitive edge. Meanwhile, local manufacturers continue to intensify competition by offering cost-effective solutions and expanding their geographic presence through mergers and product launches.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Animal type

- 2.2.4 Technique

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for higher reproductive efficiency compared to natural mating

- 3.2.1.2 Increasing demand for enhanced genetics in both livestock and companion animals

- 3.2.1.3 Technological advancements in semen collection and preservation techniques

- 3.2.1.4 Rising prevalence of sexually transmitted diseases among animals

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of procedural failures and complications

- 3.2.2.2 Lack of skilled technicians

- 3.2.2.3 Regulatory and ethical concerns

- 3.2.2.4 High set-up and equipment cost

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for genetic improvement in livestock

- 3.2.3.2 Growing adoption of artificial intelligence in developing countries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Services

- 5.3 Semen

- 5.3.1 Normal semen

- 5.3.2 Sexed semen

- 5.4 Instruments

- 5.5 Kits and consumables

Chapter 6 Market Estimates and Forecast, By Animal Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Bovine

- 6.3 Swine

- 6.4 Ovine

- 6.5 Caprine

- 6.6 Equine

- 6.7 Other animal types

Chapter 7 Market Estimates and Forecast, By Technique, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Intratubal insemination

- 7.3 Intrauterine insemination

- 7.4 Intracervical insemination

- 7.5 Intrauterine tuboperitoneal insemination

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary clinics and hospitals

- 8.3 Animal breeding centers

- 8.4 Research institutes and universities

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bovine Elite

- 10.2 CRV Holdings

- 10.3 Geno SA

- 10.4 Genus Plc

- 10.5 IMV Technologies

- 10.6 Minitube Group

- 10.7 SEMEX

- 10.8 Select Sires

- 10.9 Swine Genetics International

- 10.10 Shipley Swine Genetics

- 10.11 Stallion AI Services

- 10.12 STgenetics

- 10.13 URUS Group

- 10.14 VikingGenetics