ラボ技能試験の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Laboratory Proficiency Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766314

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

世界のラボ技能試験市場は、2024年には14億米ドルと評価され、CAGR 5.8%で成長し、2034年には25億米ドルに達すると推定されています。

この市場拡大の大きな原動力となっているのは、検査室環境における強固な品質管理に対する需要の高まりと、さまざまな分野における技能試験の利用拡大です。規制当局の監視が強まり、認定を求める検査室が増えていることから、市場参入企業が増加しています。臨床診断ラボの拡大と、慢性疾患や感染症を管理するための精密検査への注目の高まりは、市場の勢いをさらに強めています。

慢性的な健康問題や感染症が急増し続ける中、正確な診断への信頼は大幅に高まっています。国際基準を守り、誤診のリスクを低減するために、技能試験プログラムがより広く採用されるようになっています。これらの品質保証プログラムは、遺伝子検査や分子検査のような高度な診断技術の広範な応用により、極めて重要になってきています。官民を問わず利害関係者は、このような進化する基準を満たすために検査施設のインフラ強化に投資しています。CLIA、ISO、CAPのような組織からのコンプライアンス要件は、現在、認証を維持し、世界な品質ベンチマークを満たすために、日常的な技能評価を義務付けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 14億米ドル |

| 予測金額 | 25億米ドル |

| CAGR | 5.8% |

臨床診断分野は2024年に4億6,200万米ドルに達し、市場で最大のシェアを占めました。この優位性は、正確な診断検査が患者の健康転帰を管理する上で重要な役割を果たしていることに起因します。慢性疾患の負担が増大する中、診断精度への依存度が高まっており、そのため大量の検査を実施するラボにとって技能試験は譲れないものとなっています。微生物学、分子検査、血液学において広範なパネルを実施している施設は、ISO 15189のような国際的な枠組みとの整合性をさらに重視しています。先進的な診断法が医療機関全体で採用されるにつれ、厳格な熟練度評価の必要性は高まり続け、エラー率の低減と患者転帰の改善を確実なものにしています。

細胞培養検査分野はCAGR 5.3%で成長し、2034年には6億8,870万米ドルに達します。細胞培養は、生物製剤、ワクチン、様々な細胞ベースの治療薬の製造に不可欠です。一貫性を維持し汚染を防ぐため、ラボは熟練度試験を通じて定期的に技術と材料を評価しなければならないです。GMPガイドラインの下で運営されている研究室、特に生物製剤や再生医療の研究室は、プロセスの信頼性と規制遵守を保証するために、これらの評価に依存しています。さらに、幹細胞治療や組織工学のような新しい治療が勢いを増すにつれて、熟練度試験を通じて標準化されたラボの実務と信頼できる結果に対する需要が高まることが予想されます。

米国のラボ技能試験2024年の市場規模は4億7,630万米ドルで、2025年から2034年にかけてCAGR 4.9%で成長すると予測されています。同国は強力な規制基盤と強固な診断インフラにより世界市場をリードしています。戦略的な資金調達イニシアティブが、検査精度の進歩をさらに後押ししています。特に感染症検出と分子診断の分野で、合計17億米ドルの投資が検査能力の拡大に充てられました。連邦政府の保健プログラムも、2024年時点で公衆衛生ラボをほぼ完全にカバーする技能評価への参加拡大を推進しており、この地域の市場参入企業の成長を大きく後押ししています。

ラボ技能試験市場における著名な業界企業は、Aashvi PT、BIO-RAD、LGC、American Proficiency Institute、COLLEGE of AMERICAN PATHOLOGISTS、QACS LAB、FAPAS、FLUXANA、AOAC INTERNATIONAL、RANDOX、MERCK、Trilogy、WEQAS、Waters、ABSOLUTE STANDARDSなどです。これには、分子生物学、微生物学、毒物学などの専門検査分野への拡大によるサービスポートフォリオの強化も含まれます。企業はまた、技能試験結果の提出を合理化し、データ分析を自動化するためのデジタルプラットフォームに投資しています。新たな診断技術に合わせたカスタム設計のPTスキームが中心的な焦点となっている一方、規制機関とのパートナーシップは、これらの企業が進化する世界品質基準に適合するのに役立っています。さらに、戦略的合併、診断ラボとの提携、新興国への地理的拡大は、競争力を高め、認定試験サービスに対する需要の高まりに対応するのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 食品および医薬品に対する厳格な安全性と品質規制

- 水質検査の需要増加

- 熟練度テストは、研究室の運用の卓越性にとって必須の前提条件です

- 医療用大麻の合法化と大麻検査機関の増加

- 業界の潜在的リスク&課題

- 熟練した専門家の不足

- 高度な試験施設への多額の資本投資の必要性

- 市場機会

- 試験業界における技術の進歩

- 食品の偽装を防ぐための技能試験の導入拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 米国

- 欧州

- テクノロジーの情勢

- ギャップ分析

- ポーター分析

- PESTEL分析

- 政策の情勢

- 将来の市場動向

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 地域別

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新サービスの開始

- 拡張計画

第5章 市場推計・予測:産業別、2021年~2034年

- 主要動向

- 臨床診断

- 微生物学

- 医薬品

- 飲食品

- 生物学的製剤

- その他の産業

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 細胞培養

- 免疫測定

- ポリメラーゼ連鎖反応

- 分光分析

- クロマトグラフィー

- その他の技術

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 病原体検出

- 分子感染症検査

- 血液化学検査および血液学検査

- 無菌性の保証

- エンドトキシンおよび発熱物質検査

- 残留溶媒および汚染物質分析

- その他の用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Aashvi PT

- ABSOLUTE STANDARDS

- American Proficiency Institute

- AOAC INTERNATIONAL

- BIO-RAD

- COLLEGE of AMERICAN PATHOLOGISTS

- FAPAS

- FLUXANA

- LGC

- MERCK

- QACS LAB

- RANDOX

- Trilogy

- Waters

- WEQAS

目次

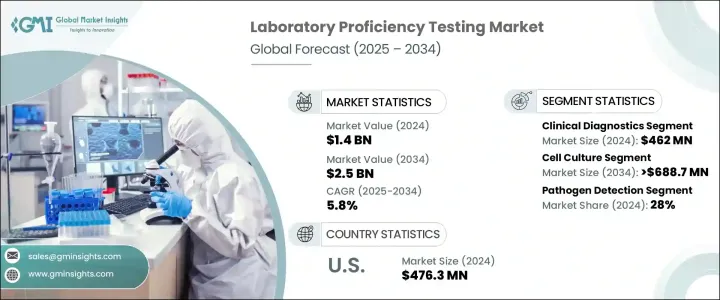

The Global Laboratory Proficiency Testing Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 2.5 billion by 2034. A significant driver behind this expansion is the rising demand for robust quality control in laboratory settings, as well as increased usage of proficiency testing across a range of sectors. With growing regulatory scrutiny and more laboratories seeking accreditation, the market is experiencing a boost in participation. The expansion of clinical diagnostics labs and heightened focus on precision testing to manage chronic and infectious diseases are further strengthening market momentum.

As chronic health issues and communicable diseases continue to surge, the reliance on accurate diagnostics has grown substantially. To uphold international standards and reduce the risk of misdiagnosis, proficiency testing programs are being adopted more widely. These quality assurance programs are becoming critical due to the broader application of advanced diagnostic technologies like genetic and molecular testing. Public and private stakeholders alike are investing in strengthening laboratory infrastructure to meet these evolving standards. Compliance requirements from organizations such as CLIA, ISO, and CAP now mandate routine proficiency evaluations to sustain certifications and meet global quality benchmarks.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.5 Billion |

| CAGR | 5.8% |

The clinical diagnostics segment reached USD 462 million in 2024, accounting for the largest share in the market. This dominance stems from the critical role accurate diagnostic testing plays in managing patient health outcomes. With the growing burden of chronic illness, there is a higher dependency on diagnostic accuracy, which makes proficiency testing non-negotiable for high-volume labs. Facilities conducting extensive panels in microbiology, molecular testing, and hematology are placing an even greater emphasis on alignment with international frameworks like ISO 15189. As advanced diagnostics see greater adoption across medical institutions, the need for rigorous proficiency assessment continues to rise, ensuring reduced error rates and improved patient outcomes.

The cell culture testing segment is set to grow at a CAGR of 5.3%, reaching USD 688.7 million by 2034. Cell culture is foundational to the production of biologics, vaccines, and various cell-based therapeutics. To maintain consistency and prevent contamination, laboratories must regularly assess their techniques and materials through proficiency testing. Labs operating under GMP guidelines, particularly those in biologics and regenerative medicine, depend on these evaluations to ensure process reliability and regulatory compliance. Furthermore, as new therapies like stem cell treatments and tissue engineering gain momentum, demand for standardized lab practices and reliable results through proficiency testing is expected to escalate.

United States Laboratory Proficiency Testing Market was valued at USD 476.3 million in 2024 and is forecast to grow at a CAGR of 4.9% from 2025 to 2034. The country leads the global market due to its strong regulatory foundation and robust diagnostics infrastructure. Strategic funding initiatives have further fueled progress in lab accuracy. Investments totaling USD 1.7 billion were dedicated to expanding testing capacity, particularly in the areas of infectious disease detection and molecular diagnostics. Federal health programs are also pushing for higher participation in proficiency evaluations, with nearly full coverage of public health labs as of 2024, which significantly supports market growth in the region.

Prominent industry players in the Laboratory Proficiency Testing Market include Aashvi PT, BIO-RAD, LGC, American Proficiency Institute, COLLEGE of AMERICAN PATHOLOGISTS, QACS LAB, FAPAS, FLUXANA, AOAC INTERNATIONAL, RANDOX, MERCK, Trilogy, WEQAS, Waters, and ABSOLUTE STANDARDS. This include strengthening their service portfolios through expansion into specialized testing areas such as molecular biology, microbiology, and toxicology. Firms are also investing in digital platforms to streamline proficiency test result submissions and automate data analysis. Custom-designed PT schemes tailored to emerging diagnostic technologies have become a central focus, while partnerships with regulatory bodies are helping these companies align with evolving global quality standards. Additionally, strategic mergers, collaborations with diagnostic laboratories, and geographic expansion into emerging economies help increase their competitive footprint and meet the growing demand for accredited testing services.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Industry trends

- 2.2.3 Technology trends

- 2.2.4 Application trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent safety and quality regulations for food and pharmaceuticals products

- 3.2.1.2 Increasing demand for water testing

- 3.2.1.3 Proficiency testing is a necessary pre-requisite for laboratory's operational excellence

- 3.2.1.4 Legalization of medical cannabis and increasing number of cannabis testing laboratories

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Dearth of skilled professionals

- 3.2.2.2 Requirement of high-capital investments for advance testing facilities

- 3.2.3 Market opportunities

- 3.2.3.1 Technological advancements in testing industry

- 3.2.3.2 Increasing adoption of proficiency tests to prevent food adulteration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Policy landscape

- 3.10 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 By Region

- 4.3.1.1 North America

- 4.3.1.2 Europe

- 4.3.1.3 Asia Pacific

- 4.3.1 By Region

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New services launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Industry, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Clinical diagnostics

- 5.3 Microbiology

- 5.4 Pharmaceuticals

- 5.5 Food and beverages

- 5.6 Biologics

- 5.7 Other industries

Chapter 6 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cell culture

- 6.3 Immunoassays

- 6.4 Polymerase chain reaction

- 6.5 Spectrometry

- 6.6 Chromatography

- 6.7 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pathogen detection

- 7.3 Molecular infectious disease testing

- 7.4 Blood chemistry and hematology panels

- 7.5 Sterility assurance

- 7.6 Endotoxin and pyrogen testing

- 7.7 Residual solvent and contaminant analysis

- 7.8 Other applications

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Aashvi PT

- 9.2 ABSOLUTE STANDARDS

- 9.3 American Proficiency Institute

- 9.4 AOAC INTERNATIONAL

- 9.5 BIO-RAD

- 9.6 COLLEGE of AMERICAN PATHOLOGISTS

- 9.7 FAPAS

- 9.8 FLUXANA

- 9.9 LGC

- 9.10 MERCK

- 9.11 QACS LAB

- 9.12 RANDOX

- 9.13 Trilogy

- 9.14 Waters

- 9.15 WEQAS

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日