|

|

市場調査レポート

商品コード

1766273

高度な水管理・ろ過装置の市場機会、成長促進要因、産業動向分析、2025~2034年予測Advanced Water Management and Filtration Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 高度な水管理・ろ過装置の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年06月10日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

世界の高度な水管理・ろ過装置市場は、2024年に295億米ドルと評価され、CAGR 5.5%で成長し、2034年には482億米ドルに達すると推定されています。

この成長の原動力となっているのは、厳しい環境規制、水不足の深刻化、各業界における持続可能な水管理ソリューションの必要性です。世界各国の政府は、水質汚染と闘い、きれいな水を確保するために厳しい環境規制を実施しています。こうした規制により、さまざまな産業で高度な水処理・ろ過システムの導入が必要となっています。この指令により、水処理インフラや技術への投資が増加しています。同様にアジア太平洋では、中国やインドなどの国々がより厳しい廃水排出基準を導入しており、産業界に処理施設のアップグレードを促しています。

このような世界の規制動向は、高度な水管理ソリューションの需要を促進する上で、コンプライアンスが重要な役割を果たしていることを裏付けています。気候変動、人口増加、都市化によって深刻化する水不足の問題は、高度な水処理・ろ過装置を採用する大きな原動力となっています。産業界では、淡水の消費量を削減し環境への影響を最小限に抑えるため、水効率の高い技術を採用する傾向が強まっています。膜バイオリアクターや逆浸透装置などの高度処理システムは、廃水の再生利用を可能にし、水資源を節約します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 295億米ドル |

| 予測金額 | 482億米ドル |

| CAGR | 5.5% |

ろ過システム分野は、2024年に295億米ドルを生み出し、2034年には482億米ドルに達すると予測されています。ろ過システムは、その実証された効率性、拡張性、幅広い用途への適応性により、主に高度な水管理・ろ過装置業界で支配的な地位を占めています。メカニカルフィルター、メンブレンフィルター、活性炭フィルターなど、伝統的なろ過技術や高度なろ過技術は、自治体や産業界の水処理プロセスの基礎的な構成要素として機能しています。浮遊物質、微生物、化学汚染物質を除去するその能力は、規制遵守と公衆衛生の安全を確保する上で不可欠です。他のシステムと比較して、ろ過装置はモジュール式に拡張でき、既存のインフラと統合でき、さまざまな水質パラメーターに合わせることができるため、包括的な水処理戦略の第一防衛ラインとなっています。

化学処理分野は2024年に214億米ドルを生み出し、72.6%を占めました。化学処理は、広範囲の水質汚染物質への対処において長年にわたって確立された有効性により、高度水管理・ろ過装置業界を支配しています。この技術は、凝集剤、殺菌剤、pH調整剤などの化学薬品を使用して、病原菌を中和し、浮遊物を除去し、有機汚染物質を効率的に分解します。その汎用性により、自治体、産業、農業の各分野で、飲料水と廃水の両方を処理することができます。凝集・凝集や塩素処理などの化学処理プロセスは、世界中の既存の水インフラに深く浸透しており、何十年にもわたって実証された信頼性と規制当局の受け入れの恩恵を受けています。

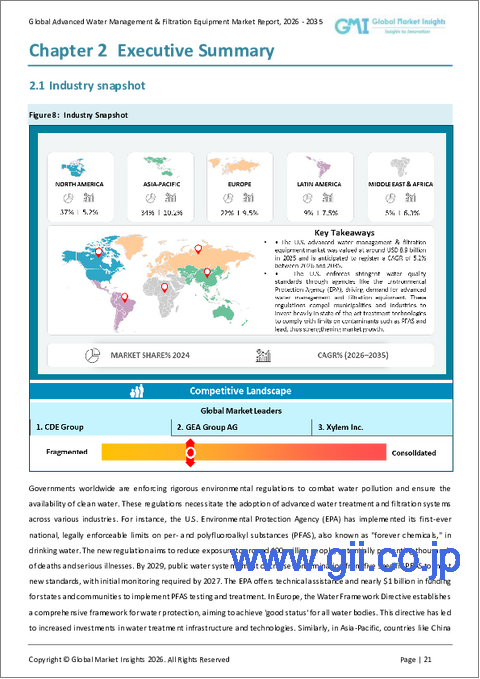

米国の高度水管理・ろ過装置市場は、2024年に88億米ドルと評価され、2025年から2034年にかけて5.2%のCAGRを記録すると予測されています。米国では、環境保護庁(EPA)などの機関を通じて厳しい水質基準が施行されており、高度な水管理・ろ過装置の需要を牽引しています。こうした規制により、自治体や産業界はPFASや鉛などの汚染物質の規制値を遵守するために最先端の処理技術に多額の投資を余儀なくされ、市場の成長が強化されます。米国は、膜ろ過、高度酸化プロセス、リアルタイムモニタリングシステムなどの革新的技術を大幅に統合した、発達した水処理インフラを保有しています。このような技術的リーダーシップが早期採用と継続的なアップグレードを促進し、市場における同国の支配的地位を維持しています。

世界の高度な水管理・ろ過装置業界のトップ企業は、Pentair plc、Xylem Inc.、GEA Group AG、Pall Corporation、CDE Groupなどです。これらの企業は、水処理分野における技術革新と販売能力で認められています。高度な水管理・ろ過装置市場におけるプレゼンスを強化するため、各社はいくつかの重要な戦略を採用しています。Pentair plcは、買収を通じて製品ポートフォリオを拡大し、住宅用および産業用のろ過ソリューションを強化しています。ザイレム社は、センサー、データ分析、遠隔監視を統合したスマート水管理システムを導入し、水処理施設の運用効率を向上させています。GEA Group AGは、特に食品、乳製品、飲食品、化学、バイオテクノロジー、発酵、でんぷん、甘味料産業におけるクロスフロー膜ろ過技術の開発に注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 機会

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:機器種別、2021年~2034年

- 主要動向

- ろ過システム

- 機械式フィルター

- メンブレンフィルター

- 精密ろ過

- 限外ろ過

- ナノろ過

- 逆浸透

- 活性炭フィルター

- イオン交換システム

- UV消毒

- オゾンろ過

- 高度酸化プロセス(AOP)システム

- 電気化学的水処理システム

- 生物学的処理システム

- 膜分離活性汚泥法(MBR)

- 移動床バイオフィルムリアクター(MBBR)

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 物理的処理

- 化学処理

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 商業用

- 住宅用

- 産業用

- 産業製造業

- 自動車

- エレクトロニクス

- 食品・飲料

- パルプ・紙

- その他(繊維等)

- 発電

- 石油・ガス

- その他(鉱業など)

- 産業製造業

- 自治体

- その他

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接

- 間接

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Alfa Laval AB

- Amiad Water Systems Ltd.

- Bluewater Group

- Calgon Carbon Corporation

- CDE Group

- Doosan Enpure

- GEA Group AG

- Hydranautics

- Kurita Water Industries Ltd.

- Lenntech B.V.

- MANN+HUMMEL Water &Fluid Solutions

- Pall Corporation

- Pentair plc

- Toray Industries, Inc.

- Xylem Inc.

The Global Advanced Water Management and Filtration Equipment Market was valued at USD 29.5 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 48.2 billion by 2034. This growth is driven by stringent environmental regulations, increasing water scarcity, and the need for sustainable water management solutions across industries. Governments worldwide are enforcing rigorous environmental regulations to combat water pollution and ensure the availability of clean water. These regulations necessitate the adoption of advanced water treatment and filtration systems across various industries. This directive has led to increased investments in water treatment infrastructure and technologies. Similarly, in Asia-Pacific, countries like China and India are introducing stricter wastewater discharge standards, prompting industries to upgrade their treatment facilities.

These global regulatory trends underscore the critical role of compliance in propelling the demand for advanced water management solutions. The escalating issue of water scarcity, exacerbated by climate change, population growth, and urbanization, is a significant driver for the adoption of advanced water treatment and filtration equipment. Industries are increasingly adopting water-efficient technologies to reduce their freshwater consumption and minimize environmental impact. Advanced treatment systems, such as membrane bioreactors and reverse osmosis units, enable the reclamation and reuse of wastewater, thereby conserving water resources.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $29.5 Billion |

| Forecast Value | $48.2 Billion |

| CAGR | 5.5% |

The filtration systems segment generated USD 29.5 billion in 2024 and is anticipated to reach USD 48.2 billion by 2034. Filtration systems hold a dominant position in the advanced water management and filtration equipment industry primarily due to their proven efficiency, scalability, and adaptability across a wide range of applications. Traditional and advanced filtration technologies-such as mechanical filters, membrane filters, and activated carbon filters-serve as foundational components in both municipal and industrial water treatment processes. Their capability to remove suspended solids, microorganisms, and chemical contaminants makes them indispensable in ensuring regulatory compliance and public health safety. Compared to other systems, filtration equipment can be modularly scaled, integrated with existing infrastructure, and tailored to varying water quality parameters, making it the first line of defense in comprehensive water treatment strategies.

The chemical treatment segment generated USD 21.4 billion in 2024 and held 72.6%. Chemical treatment dominates the advanced water management & filtration equipment industry due to its long-established effectiveness in addressing a broad spectrum of water contaminants. This technology employs chemicals such as coagulants, disinfectants, and pH adjusters to neutralize pathogens, remove suspended solids, and degrade organic pollutants efficiently. Its versatility allows the treatment of both potable and wastewater across municipal, industrial, and agricultural sectors. Chemical treatment processes, including coagulation-flocculation and chlorination, are deeply embedded in existing water infrastructure worldwide, benefiting from decades of proven reliability and regulatory acceptance, which sustains its leading market position.

U.S. Advanced Water Management & Filtration Equipment Market was valued at USD 8.8 billion in 2024 and is anticipated to register a CAGR of 5.2% between 2025 and 2034. The U.S. enforces stringent water quality standards through agencies like the Environmental Protection Agency (EPA), driving demand for advanced water management and filtration equipment. These regulations compel municipalities and industries to invest heavily in state-of-the-art treatment technologies to comply with limits on contaminants such as PFAS and lead, thus strengthening market growth. The U.S. possesses a well-developed water treatment infrastructure with significant integration of innovative technologies such as membrane filtration, advanced oxidation processes, and real-time monitoring systems. This technological leadership fosters early adoption and continuous upgrades, maintaining the country's dominant position in the market.

The top companies in the Global Advanced Water Management and Filtration Equipment Industry include Pentair plc, Xylem Inc., GEA Group AG, Pall Corporation, and CDE Group. These companies are recognized for their innovation and distribution capabilities in the water treatment sector. To strengthen their presence in the advanced water management and filtration equipment market, companies are adopting several key strategies. Pentair plc has expanded its product portfolio through acquisitions, enhancing its filtration solutions for residential and industrial applications. Xylem Inc. has introduced smart water management systems, integrating sensors, data analytics, and remote monitoring to improve operational efficiency in water treatment facilities. GEA Group AG focuses on developing crossflow membrane filtration technology, particularly in the food, dairy, beverage, chemical, biotechnology, fermentation, starch, and sweetener industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Filtration systems

- 5.2.1 Mechanical filters

- 5.2.2 Membrane filters

- 5.2.2.1 Microfiltration

- 5.2.2.2 Ultrafiltration

- 5.2.2.3 Nanofiltration

- 5.2.2.4 Reverse osmosis

- 5.2.3 Activated carbon filters

- 5.2.4 Ion exchange systems

- 5.2.5 UV Disinfection

- 5.2.6 Ozone filtration

- 5.3 Advanced oxidation processes (AOPs) systems

- 5.4 Electrochemical water treatment systems

- 5.5 Biological treatment systems

- 5.5.1 Membrane bioreactors (MBR)

- 5.5.2 Moving bed biofilm reactor (MBBR)

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Physical treatment

- 6.3 Chemical treatment

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Commercial

- 7.3 Residential

- 7.4 Industrial

- 7.4.1 Industrial manufacturing

- 7.4.1.1 Automotive

- 7.4.1.2 Electronics

- 7.4.1.3 Food & beverage

- 7.4.1.4 Pulp & paper

- 7.4.1.5 Others (Textiles, etc.)

- 7.4.2 Power generation

- 7.4.3 Oil & Gas

- 7.4.4 Others (Mining, etc.)

- 7.4.1 Industrial manufacturing

- 7.5 Municipality

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 U.K.

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 10.1 Alfa Laval AB

- 10.2 Amiad Water Systems Ltd.

- 10.3 Bluewater Group

- 10.4 Calgon Carbon Corporation

- 10.5 CDE Group

- 10.6 Doosan Enpure

- 10.7 GEA Group AG

- 10.8 Hydranautics

- 10.9 Kurita Water Industries Ltd.

- 10.10 Lenntech B.V.

- 10.11 MANN+HUMMEL Water & Fluid Solutions

- 10.12 Pall Corporation

- 10.13 Pentair plc

- 10.14 Toray Industries, Inc.

- 10.15 Xylem Inc.