ベビージュースの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Baby Juice Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766269

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

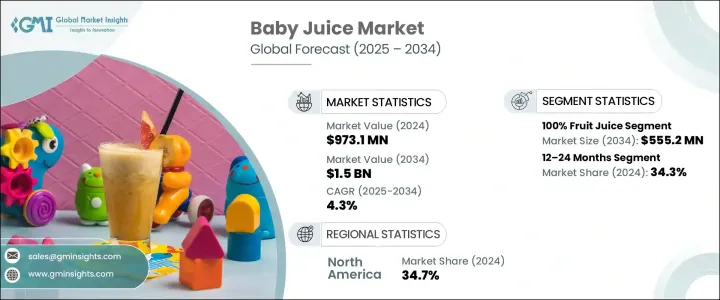

世界のベビージュース市場は、2024年には9億7,310万米ドルとなり、CAGR 4.3%で成長し、2034年には15億米ドルに達すると推定されています。

この着実な成長は、幼児期の栄養に関する親の意識の高まりを反映しています。親は乳幼児に栄養豊富な食事を与えることを重視するようになっており、必須ビタミンやミネラルを強化したベビージュースが好まれる選択肢となっています。健康志向が世界的に高まるにつれ、便利な栄養強化製品への需要が高まっています。さらに、働く母親や共働き世帯の増加といったライフスタイルの変化も、レディトゥイートベビーフードや飲食品への依存度を高めています。こうしたジュースは、多忙なスケジュールを抱える親、特に外出の多い親にとって、手軽で実用的な解決策となります。

ラテンアメリカ、アジア太平洋の、アフリカなどの新興市場の成長も重要な役割を果たしています。出生率の上昇、可処分所得の増加、eコマースチャネルの強化を含む小売インフラの改善が、ベビー用栄養製品の普及を後押ししています。中産階級の人口が拡大を続けるなか、包装入りベビージュースへのアクセスも容易になり、十分なサービスを受けていない地域への市場浸透が進み、このカテゴリーの世界の広がりが確固たるものとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 9億7,310万米ドル |

| 予測金額 | 15億米ドル |

| CAGR | 4.3% |

100%フルーツジュースセグメントは、2034年までに5億5,520万米ドルに達し、2034年のCAGRは4.5%で成長すると予測されます。健康志向の購買行動が主流になりつつあり、幼児の食生活における過剰な糖分への懸念が消費者を自然な代替品へと向かわせています。親たちは、砂糖無添加で本物の果物にこだわったジュースを好むようになっています。こうしたジュースを元気が出る、自然の活力が感じられると位置づけた継続的なプロモーションや啓蒙キャンペーンは、栄養に関心の高い今日の養育者の共感を呼んでいます。こうした嗜好は、放任的な授乳方法からの脱却と、バランスのとれた小児期の発育をサポートする、より健康的な選択肢への移行と一致しています。

年齢層別では、12~24ヵ月のセグメントが2024年に34.3%のシェアを占め、2034年までCAGR 6.8%で成長すると予想されます。この段階は、子どもが母乳や粉ミルクから、ジュースを含むより幅広い種類の固形・半固形食品に移行し始めるため、食生活の重要な転換期となります。このセグメントの親は特に選り好みが激しく、味が良いだけでなく、免疫、消化、全般的な開発をサポートする製品を求める。この年齢層に合わせたベビージュースは、一般的にビタミンC、鉄分、その他の重要な栄養素を含み、天然材料に強く重点を置いています。包装も大きな役割を果たし、こぼれない、人間工学に基づいたボトルは、自分で飲めるようになる幼児用に設計されており、親と幼児の両方への訴求力を高めるのに役立っています。

北米のベビージュースの2024年のシェアは34.7%。同地域のリーダーシップは、先進的流通システム、可処分所得の増加、クリーンラベル、栄養強化、オーガニック志向へのシフトに支えられています。米国とカナダの親は、幼児期の栄養を優先するため、十分な情報に基づいた購買決定を行うようになっています。製品の表示と安全性に関する規制は特に厳しくなっており、これが店頭に並ぶ製品への信頼につながっています。政府の監督と栄養に焦点をあてた表示は、品質と消費者の安全性の一貫性を確保し、強固で透明なベビージュースエコシステムに貢献しています。

世界のベビージュース市場で活躍する主要企業には、Beech-Nut Nutrition Company、The Kraft Heinz Company、Sprout Foods, Inc.、Campbell Soup Company、Nestle S.A.などがあります。主要企業は、オーガニック、非遺伝子組み換え、アレルゲンフリーなど、製品ポートフォリオを多様化することで市場での地位を強化しています。また、栄養に敏感な親にアピールするため、ビタミン、ミネラル、プロバイオティクスを強化した機能性飲料に進出している企業も多いです。リシーラブルでこぼれにくい容器など、魅力的で便利な包装への戦略的投資は、親にとっても幼児にとっても使い勝手を高めています。ブランドはまた、デジタルマーケティングやソーシャルメディアプラットフォームを活用してミレニアル世代やZ世代の親とつながり、一方でeコマースを通じて流通を拡大し、入手しやすさを高めています。小児科栄養士とのコラボレーションや安全認証への準拠は、健康志向の消費者の間でブランドの信頼性と信用をさらに高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- 便利なベビーフードの選択肢に対する需要の高まり

- 新興経済諸国における可処分所得の増加

- 働く女性人口の増加

- 製品の革新と強化

- 産業の潜在的リスク・課題

- 小児の早期ジュース摂取に対する推奨

- 糖分に関する健康上の懸念

- 丸ごとの果物や自家製の果物を好む

- 厳格な規制枠組み

- 市場機会

- 有機と天然の変種の開発

- 新興市場への拡大

- eコマースの成長

- 機能・強化ベビージュース製品

- 成長可能性分析

- 規制情勢

- ベビー飲食品に関する世界の規制

- FDAの規制とガイドライン

- 欧州の連合の規制枠組み

- ジュースのHACCP要件

- ラベル表示と健康強調表示規制

- 規制が市場成長に与える影響

- ポーター分析

- PESTEL分析

- 現在の技術動向

- 新興技術

- 促進要因

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- サステイナブルプラクティス

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

- 消費者行動分析

- 親の好みと決定要因

- 購入パターン

- 小児科の推奨事項の影響

- 健康と栄養に関する意識

- ブランドロイヤルティと乗り換え行動

- 小児栄養の動向

- 乳児栄養に関するガイドラインの進化

- 年齢に応じた飲料の推奨

- 幼児期の砂糖摂取に関する懸念

- 子どもの開発におけるジュースの役割

- 乳幼児向けの代替飲料

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測:製品タイプ別、2021~2034年

- 主要動向

- 100%フルーツジュース

- フルーツジュースブレンド

- 野菜ジュース

- オーガニックベビージュース

- 強化ベビージュース

- その他

第6章 市場推定・予測:年齢層別、2021~2034年

- 主要動向

- 6~12ヵ月

- 12~24ヵ月

- 24~36ヵ月

- 36ヵ月以上

第7章 市場推定・予測:包装形態別、2021~2034年

- 主要動向

- ボトル

- ポーチ

- カートン

- その他

第8章 市場推定・予測:流通チャネル別、2021~2034年

- 主要動向

- スーパーマーケットとハイパーマーケット

- 専門店

- コンビニエンスストア

- オンライン小売

- 薬局とドラッグストア

- その他

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第10章 企業プロファイル

- Nestle S.A.(Gerber Products Company)

- The Kraft Heinz Company

- Danone S.A.

- Beech-Nut Nutrition Company

- Hain Celestial Group

- Campbell Soup Company(Plum Organics)

- Nurture Inc.(Happy Family Organics)

- Sprout Foods, Inc.

- Ella’s Kitchen

- Once Upon a Farm

- Apple & Eve, LLC

- Welch Foods Inc.

- Bellamy's Organic

- Organix Brands Ltd.

- The Coca-Cola Company

目次

The Global Baby Juice Market was valued at USD 973.1 million in 2024 and is estimated to grow at a CAGR of 4.3% to reach USD 1.5 billion by 2034. This steady growth reflects rising parental awareness about early childhood nutrition. Parents are increasingly focused on providing well-rounded, nutrient-rich diets for their infants and toddlers, and baby juices-often enriched with essential vitamins and minerals-are becoming a favored option. As health consciousness grows globally, demand for convenient, fortified products is increasing. Additionally, lifestyle changes, including a growing population of working mothers and dual-income households, have boosted reliance on ready-to-consume baby foods and beverages. These juices offer a quick and practical solution for parents with busy schedules, especially those frequently on the go.

Growth in emerging markets across regions such as Latin America, Asia-Pacific, and Africa is also playing a key role. Rising birth rates, higher disposable incomes, and improved retail infrastructure-including stronger e-commerce channels-are supporting the spread of baby nutrition products. As middle-class populations continue to expand, accessibility to packaged baby juices is becoming easier, pushing forward market penetration in underserved regions and cementing the global reach of the category.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $973.1 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 4.3% |

The 100% fruit juice segment is forecast to reach USD 555.2 million by 2034, growing at a CAGR of 4.5% during 2034. Health-conscious buying behaviors are becoming more mainstream, and concerns around excess sugar in children's diets have driven consumers toward natural alternatives. Parents are gravitating toward juices with no added sugar and a focus on real fruit content. Ongoing promotions and awareness campaigns that position these juices as energizing and naturally vibrant are resonating with today's nutrition-minded caregivers. These preferences align with the shift away from indulgent feeding practices and a move toward healthier options that support balanced childhood development.

In terms of age demographics, the 12-24 months segment held 34.3% share in 2024 and is expected to grow at a CAGR of 6.8% through 2034. This stage marks a critical shift in dietary habits as children begin to transition from breast milk or formula to a broader range of solid and semi-solid foods, including juices. Parents in this segment are particularly selective, seeking products that not only taste good but also support immunity, digestion, and overall development. Baby juices tailored to this age group typically contain vitamin C, iron, and other important nutrients, with a strong focus on natural ingredients. Packaging also plays a major role-non-spill, ergonomic bottles are designed for toddlers learning to drink independently, helping boost appeal for both parents and young children.

North America Baby Juice Market held 34.7% share in 2024. The region's leadership is backed by advanced distribution systems, higher disposable incomes, and a shift toward clean-label, fortified, and organic options. Parents in both the U.S. and Canada are increasingly driven by informed purchasing decisions that prioritize early-life nutrition. Regulations around product labeling and safety are particularly stringent, which builds trust in the products available on the shelves. Government oversight and nutrition-focused labeling contribute to a robust and transparent baby juice ecosystem, ensuring consistency in quality and consumer safety.

Key players active in the Global Baby Juice Market include Beech-Nut Nutrition Company, The Kraft Heinz Company, Sprout Foods, Inc., Campbell Soup Company, and Nestle S.A. Leading brands are strengthening their market position by diversifying product portfolios with organic, non-GMO, and allergen-free offerings. Many have expanded into functional beverages fortified with vitamins, minerals, and probiotics to appeal to nutrition-savvy parents. Strategic investments in attractive, convenient packaging-such as resealable, spill-proof containers-are enhancing usability for parents and toddlers alike. Brands are also leveraging digital marketing and social media platforms to connect with millennial and Gen Z parents, while broadening distribution via e-commerce to boost accessibility. Collaborations with pediatric nutritionists and compliance with safety certifications further elevate brand credibility and trust among health-conscious consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Age group

- 2.2.3 Packaging type

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for convenient baby food options

- 3.2.1.2 Rising disposable income in developing economies

- 3.2.1.3 Increasing working women population

- 3.2.1.4 Product innovations and fortification

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Pediatric recommendations against early juice consumption

- 3.2.2.2 Health concerns related to sugar content

- 3.2.2.3 Preference for whole fruits and homemade options

- 3.2.2.4 Stringent regulatory framework

- 3.2.3 Market opportunities

- 3.2.3.1 Development of organic and natural variants

- 3.2.3.2 Expansion in emerging markets

- 3.2.3.3 E-commerce growth

- 3.2.3.4 Functional and fortified baby juice products

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Global regulations for baby food and beverages

- 3.4.2 FDA regulations and guidelines

- 3.4.3 European Union regulatory framework

- 3.4.4 Juice HACCP requirements

- 3.4.5 Labeling and health claim regulations

- 3.4.6 Impact of regulations on market growth

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.1.1 Juice processing technologies

- 3.6.1.2 Preservation methods

- 3.6.1.3 Packaging innovations

- 3.6.1.4 Quality testing advancements

- 3.6.1.5 Digital technologies in supply chain

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.6.1 Technology and Innovation landscape

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Consumer Behavior Analysis

- 3.13.1 Parental preferences and decision factors

- 3.13.2 Purchase patterns

- 3.13.3 Influence of pediatric recommendations

- 3.13.4 Health and nutrition awareness

- 3.13.5 Brand loyalty and switching behavior

- 3.14 Pediatric nutrition trends

- 3.14.1 Evolving guidelines for infant nutrition

- 3.14.2 Age-appropriate beverage recommendations

- 3.14.3 Sugar intake concerns in early childhood

- 3.14.4 Role of juices in child development

- 3.14.5 Alternative beverage options for infants and toddlers

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.7 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million) (Kilo Liters)

- 5.1 Key trends

- 5.2 100% fruit juice

- 5.3 Fruit juice blends

- 5.4 Vegetable juice

- 5.5 Organic baby juice

- 5.6 Fortified baby juice

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Age Group, 2021-2034 (USD Million) (Kilo Liters)

- 6.1 Key trends

- 6.2 6–12 months

- 6.3 12–24 months

- 6.4 24–36 months

- 6.5 Above 36 months

Chapter 7 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Million) (Kilo Liters)

- 7.1 Key trends

- 7.2 Bottles

- 7.3 Pouches

- 7.4 Cartons

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Million) (Kilo Liters)

- 8.1 Key trends

- 8.2 Supermarkets and hypermarkets

- 8.3 Specialty stores

- 8.4 Convenience stores

- 8.5 Online retail

- 8.6 Pharmacies and drug stores

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Liters)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Nestle S.A. (Gerber Products Company)

- 10.2 The Kraft Heinz Company

- 10.3 Danone S.A.

- 10.4 Beech-Nut Nutrition Company

- 10.5 Hain Celestial Group

- 10.6 Campbell Soup Company (Plum Organics)

- 10.7 Nurture Inc. (Happy Family Organics)

- 10.8 Sprout Foods, Inc.

- 10.9 Ella’s Kitchen

- 10.10 Once Upon a Farm

- 10.11 Apple & Eve, LLC

- 10.12 Welch Foods Inc.

- 10.13 Bellamy's Organic

- 10.14 Organix Brands Ltd.

- 10.15 The Coca-Cola Company

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日