|

市場調査レポート

商品コード

1892795

医療機器流通サービス市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測Medical Device Distribution Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 医療機器流通サービス市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年12月04日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

概要

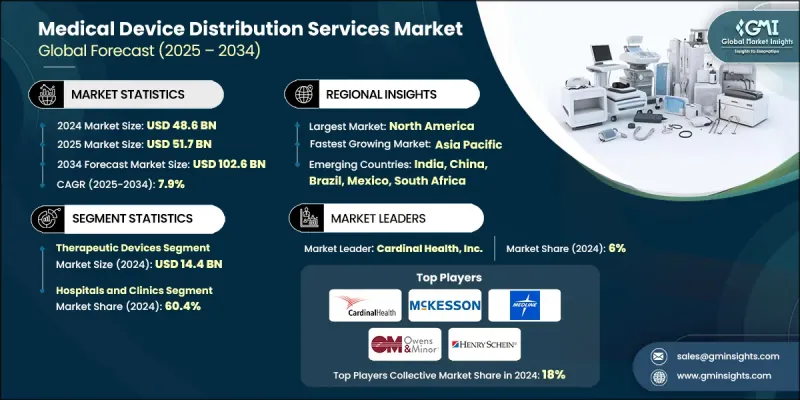

世界の医療機器流通サービス市場は、2024年に486億米ドルと評価され、2034年までにCAGR7.9%で成長し、1,026億米ドルに達すると予測されています。

この拡大は、慢性疾患の有病率の上昇、在宅医療および遠隔モニタリングソリューションの急速な普及、ならびにデジタルサプライチェーン能力への多額の投資によって推進されています。流通業者は、医療システムにとって戦略的パートナーとしての位置付けを強めており、物流だけでなく、設置、校正、トレーニング、コールドチェーン管理、UDIトレーサビリティなどの付加価値サービスを提供しています。これにより、商品輸送から統合された臨床供給ソリューションへの移行が加速しています。同時に、病院の大量調達やグループ購買組織(GPO)の動向により、在庫切れの削減、リードタイムの短縮、複数の管轄区域にわたる規制順守を確保する高度な流通サービスへの需要が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年度 | 2025-2034 |

| 開始時価値 | 486億米ドル |

| 予測金額 | 1,026億米ドル |

| CAGR | 7.9% |

製品タイプ別では、治療用機器セグメントが2024年に144億米ドルで市場をリードし、輸液ポンプ、呼吸器、心血管ステント、人工インプラント、透析システム、その他の治療に不可欠な技術に対する強い需要を反映しています。治療用デバイスは通常、専門的な取り扱い、コールドチェーンまたは環境条件に敏感な物流、アフターサービス(設置、保守、スタッフ研修)を必要とするため、販売代理店のマージンを拡大し、病院や診療所との長期的なパートナーシップを強化します。

最終用途別では、病院・診療所セグメントが2024年に60.4%のシェアを占めました。これは、幅広い医療機器の需要、集中調達プロセス、緊急時・外科治療のための高水準な院内在庫維持の必要性によるものです。病院が物流・設置・アフターサービスを組み合わせた包括的サービス提供を好む傾向は、トレーサビリティ、迅速な修理対応、コンプライアンス報告を保証できる流通パートナーの戦略的重要性を高めています。

北米医療機器流通サービス市場は2024年に39.2%のシェアを占めました。これは同地域の成熟した医療インフラ、高い処置件数、デジタル物流技術(IoT、AI、トレーサビリティのためのブロックチェーン)の早期導入を反映しています。大規模病院ネットワーク、集中型GPO契約、強力な在宅医療償還制度を含む米国市場の市場力学は、流通業者の利益率向上と先進的なコールドチェーン・自動補充システムへの投資を支えています。さらに、サプライチェーンのレジリエンス強化、流通センターにおける技術近代化、UDI(医療機器識別子)などの規制枠組み(追跡可能で品質保証された流通モデルを促進)に対する公的・民間資金の大幅な投入により、北米の主導的立場はさらに強化されています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患の増加傾向

- 調査目的の投資急増と医療機器承認の増加

- 在宅医療および遠隔モニタリングに対する需要の高まり

- 医療機器技術の進歩

- 業界の潜在的リスク&課題

- 高い初期資本支出の必要性

- 厳格な規制順守の必要性

- 市場機会

- オンライン流通サービスとデジタル発注システムの成長

- サプライチェーン強化に向けた官民連携の拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術的進歩

- 現在の技術動向

- 新興技術

- サプライチェーン分析

- 償還シナリオ

- 価格分析、2024

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携および共同事業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 診断機器

- 治療用機器

- 患者モニタリング機器

- 在宅医療機器

- その他の製品タイプ

第6章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院および診療所

- 診断センター

- 外来手術センター(ASCs)

- 長期療養施設

- 在宅医療環境

第7章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第8章 企業プロファイル

- Alfresa Holdings Corporation

- Avantor, Inc.

- Bunzl plc

- CAN-med Healthcare

- Cardinal Health, Inc.

- Henry Schein, Inc.

- ケボメッド・欧州株式会社

- McKesson Corporation

- Meditek Systems Pvt. Ltd.

- Medline Industries, LP.

- Owens &Minor, Inc.

- Patterson Companies, Inc.

- Soquelec Ltd.

- Southmedic Inc.

- The Stevens Company Limited