|

市場調査レポート

商品コード

1766211

超高温セラミックスの市場機会、成長促進要因、産業動向分析、2025~2034年予測Ultra-High Temperature Ceramics (UHTCs) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 超高温セラミックスの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年06月11日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

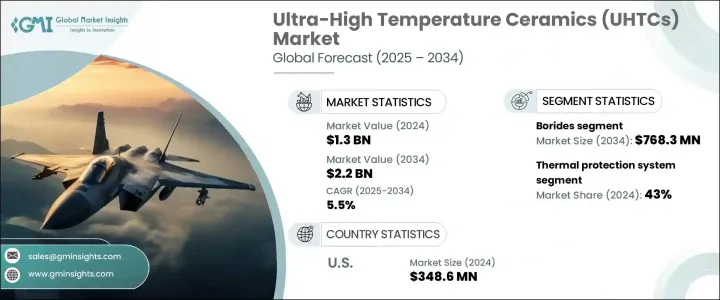

世界の超高温セラミック市場は、2024年に13億米ドルと評価され、CAGR 5.5%で成長し、2034年には22億米ドルに達すると推定されています。

このセグメントの成長は、防衛、航空宇宙、自動車、エネルギーなどにおける技術進歩が大きな原動力となっており、極端な熱的・機械的条件下で動作可能な材料がますます求められています。UHTCは、3,000℃を超える温度に耐えるように設計されており、従来型材料が故障するような環境では不可欠なものとなっています。これらのセラミックは現在、高熱システムにおいてエネルギー効率を高め、持続可能性の目標を達成する上で極めて重要な役割を果たしています。その用途は、先進的推進力、高速飛行システム、次世代の熱保護用途で拡大しています。

産業が性能を重視し、排出を削減する技術革新にシフトするにつれて、UHTCに対する需要は増加の一途をたどっています。UHTCの重要性は、技術的限界を押し広げ、比類のない耐久性を必要とする高性能セグメントにおいて、より大きくなっています。さらに、世界の軍事戦略の進化や宇宙探査への注目の高まりにより、熱に強い材料へのニーズが加速しています。特に米国では、産業全体で投資が拡大しており、UHTCは酸化、熱衝撃、機械的ストレスに対する耐性が求められる用途で不可欠なものとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 13億米ドル |

| 予測金額 | 22億米ドル |

| CAGR | 5.5% |

ホウ化物セグメントは2024年に4億5,610万米ドルを生み出し、2034年には7億6,830万米ドルに成長すると予想されています。このセグメントは、その優れた熱伝導性、卓越した耐酸化性、超高融点により優位を保っており、最高レベルの性能が要求される用途に最適です。UHTCの中でもホウ化物は、標準的なセラミックが耐えられる範囲をはるかに超える機械的負荷と温度に耐える能力を持つため、過酷な環境において特に高く評価されています。このような特性から、ホウ化物は、信頼性が重要視される推進システムや熱障壁で好まれる材料クラスとなっています。

熱保護システムセグメントは43%のシェアを占め、依然として主要な用途セグメントです。極超音速飛行や宇宙ミッションのような極めて過酷な環境下で構造的・熱的完全性を維持できる材料へのニーズが高まっていることが、このセグメントにおけるUHTCの需要に拍車をかけています。持続的な空気力学的ストレス、激しい摩擦熱、急速な大気遷移のもとで性能を発揮するUHTCの能力は、絶対的な熱制御を必要とするシステムにとって不可欠なものとなっています。宇宙と防衛技術の革新が加速するにつれて、高い耐熱性と機械的弾力性を備えた材料への需要が急増しています。

米国の超高温セラミック(UHTC)市場は、2024年に3億4,860万米ドルを創出しました。この強い存在感は、高温で性能を発揮できる材料に大きく依存する先進的防衛システム、宇宙技術、エネルギー用途への多額の投資が原動力となっています。軍事力の近代化と宇宙開発への積極的な取り組みにより、超耐久性材料への依存度が高まっています。次世代推進力と国防戦略への注目が高まっていることから、米国のUHTC市場は堅調な勢いを維持すると予想されます。

世界の超高温セラミック(UTHC)市場に貢献している主要企業には、Rolls-Royce、Precision Ceramics、Lockheed Martin、Saint-Gobain、Lockheed Martin Corporationなどがあります。これらの産業大手は、より高い破壊靭性、より長い耐用年数といった強化された特性を持つUHTCの開発を目指し、研究開発への的を絞った投資を通じて市場での地位を強化しています。航空宇宙・防衛機関との戦略的協力関係は、カスタマイズ型材料開発と重要システムへの統合を可能にしています。また、需要の増大に対応するため、企業は生産能力を拡大し、先進的製造技術を追求しています。用途を多様化し、厳格な品質管理を徹底することで、これらの企業は、この発展途上のセグメントで長期的なリーダーシップを発揮できるよう自らを位置づけています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- 産業の潜在的リスク・課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- サステイナブルプラクティス

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場規模・予測:材料別、2021~2034年

- 主要動向

- ホウ化物

- 二ホウ化ジルコニウム(ZrB2)

- 二ホウ化ハフニウム(HfB2)

- 二ホウ化タンタル(TaB2)

- 二ホウ化チタン(TiB2)

- その他のホウ化物

- 炭化物

- 炭化ジルコニウム(ZrC)

- ハフニウムカーバイド(HfC)

- 炭化タンタル(TaC)

- 炭化チタン(TiC)

- 炭化ケイ素(SiC)

- その他の炭化物

- 窒化物

- 窒化ハフニウム(HfN)

- 窒化ジルコニウム(ZrN)

- 窒化タンタル(TaN)

- 窒化シリコン(Si3N4)

- その他の窒化物

- 複合材料システム

- ホウ化物系複合材料

- 炭化物系複合材料

- 窒化物系複合材料

- その他

- その他の材料タイプ

第6章 市場規模・予測:製品形態別、2021~2034年

- 主要動向

- 粉末

- バルクコンポーネント

- モノリシックコンポーネント

- 複合部品

- コーティング

- 遮熱コーティング

- 耐酸化コーティング

- 耐食性コーティング

- その他のコーティングタイプ

- 繊維とウィスカー

- その他

第7章 市場規模・予測:製造方法別、2021~2034年

- 主要動向

- ホットプレス

- 放電プラズマ焼結(SPS)

- 反応性ホットプレス

- 加圧焼結

- 化学蒸着(CVD)

- 積層造形

- その他の製造方法

第8章 市場規模・予測:用途別、2021~2034年

- 主要動向

- 熱保護システム

- 極超音速機の前縁

- 再突入機の熱シールド

- ロケットノズルのスロート

- 燃焼室ライナー

- その他

- 推進システム

- ロケットエンジン部品

- ガスタービン部品

- スクラムジェットのコンポーネント

- その他の推進用途

- 高温センサと計測機器

- 切削工具と耐摩耗部品

- 炉の要素とるつぼ

- 原子力用途

- その他

第9章 市場規模・予測:最終用途産業別、2021~2034年

- 主要動向

- 航空宇宙と防衛

- 軍事航空宇宙

- 民間航空宇宙

- 宇宙探査

- ミサイルシステム

- その他

- 産業

- 金属加工

- ガラス製造

- 化学処理

- その他の産業用途

- エネルギー

- 原子力エネルギー

- 化石燃料発電

- その他のエネルギー用途

- エレクトロニクスと半導体

- 研究と学術

- その他

第10章 市場規模・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他の中東・アフリカ

第11章 企業プロファイル

- Lockheed Martin Corporation

- Rolls-Royce

- Ultramet

- BAE Systems

- 3M Company

- CoorsTek

- Morgan Advanced Materials

- Kennametal

- Aremco Products

- Advanced Ceramics Manufacturing

- Precision Ceramics USA

- Kyocera Corporation

- Saint-Gobain

The Global Ultra-High Temperature Ceramics Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 2.2 billion by 2034. Growth in this sector is largely driven by technological advancements in defense, aerospace, automotive, and energy, which increasingly require materials capable of operating under extreme thermal and mechanical conditions. UHTCs are engineered to withstand temperatures exceeding 3000°C, making them essential in environments where conventional materials fail. These ceramics are now playing a pivotal role in enhancing energy efficiency and meeting sustainability goals in high-heat systems. Their use is expanding in advanced propulsion, high-speed flight systems, and next-gen thermal protection applications.

As industries shift towards performance-focused and emission-reducing innovations, demand for UHTCs continues to climb. Their importance is magnified in high-performance sectors pushing technological boundaries and requiring unmatched durability. In addition, evolving global military strategies and a greater focus on space exploration are accelerating the need for thermally resilient materials. With escalating investments across industrial verticals, particularly in the US, UHTCs are becoming indispensable in applications that demand resistance to oxidation, thermal shock, and mechanical stress.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 5.5% |

The Borides segment generated USD 456.1 million in 2024 and is expected to grow to USD 768.3 million by 2034. This category remains dominant due to its superior thermal conductivity, exceptional oxidation resistance, and ultra-high melting points, making it ideal for applications that demand the highest levels of performance. Among UHTCs, borides are specifically valued in extreme environments due to their capacity to endure mechanical loads and temperatures well beyond what standard ceramics can tolerate. These attributes make them the preferred material class in propulsion systems and thermal barriers where reliability is critical.

The thermal protection systems segment accounted for 43% share, remaining the leading application segment. The increasing need for materials that can maintain structural and thermal integrity in extremely harsh environments, such as during hypersonic travel or space-bound missions, is fueling demand for UHTCs in this segment. Their ability to perform under sustained aerodynamic stress, intense frictional heat, and rapid atmospheric transitions makes them indispensable for systems requiring absolute thermal control. As innovation accelerates in space and defense technologies, demand for materials with high heat tolerance and mechanical resilience is surging.

United States Ultra-High Temperature Ceramics (UHTCs) Market generated USD 348.6 million in 2024. This strong presence is driven by significant investments in advanced defense systems, space technology, and energy applications that rely heavily on materials capable of performing at elevated temperatures. The country's aggressive push to modernize military capabilities and space initiatives is increasing reliance on ultra-durable materials. Given the rising focus on next-generation propulsion and national defense strategies, the market for UHTCs in the US is expected to maintain steady momentum.

Key companies contributing to the Global Ultra-High Temperature Ceramics (UTHCs) Market include Rolls-Royce, Precision Ceramics, Lockheed Martin Corporation, Saint-Gobain, and Advanced Ceramics Manufacturing. These industry leaders are strengthening their market positions through targeted investments in R&D, aiming to develop UHTCs with enhanced properties such as higher fracture toughness and longer service life. Strategic collaborations with aerospace and defense organizations allow for customized material development and integration into critical systems. Firms are also scaling production capacities and pursuing advanced manufacturing techniques to meet growing demand. By diversifying applications and ensuring stringent quality control, these companies are positioning themselves for long-term leadership in this evolving field.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material type

- 2.2.3 Product form

- 2.2.4 Manufacturing method

- 2.2.5 Application

- 2.2.6 End use Industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Size and Forecast, By Material Type, 2021-2034 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Borides

- 5.2.1 Zirconium diboride (ZrB?)

- 5.2.2 Hafnium diboride (HfB?)

- 5.2.3 Tantalum diboride (TaB?)

- 5.2.4 Titanium diboride (TiB?)

- 5.2.5 Other borides

- 5.3 Carbides

- 5.3.1 Zirconium carbide (ZrC)

- 5.3.2 Hafnium carbide (HfC)

- 5.3.3 Tantalum carbide (TaC)

- 5.3.4 Titanium carbide (TiC)

- 5.3.5 Silicon carbide (SiC)

- 5.3.6 Other carbides

- 5.4 Nitrides

- 5.4.1 Hafnium nitride (HfN)

- 5.4.2 Zirconium nitride (ZrN)

- 5.4.3 Tantalum nitride (TaN)

- 5.4.4 Silicon nitride (Si?N?)

- 5.4.5 Other nitrides

- 5.5 Composite systems

- 5.5.1 Boride-based composites

- 5.5.2 Carbide-based composites

- 5.5.3 Nitride-based composites

- 5.5.4 Other composite systems

- 5.6 Other material types

Chapter 6 Market Size and Forecast, By Product Form, 2021-2034 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Powders

- 6.3 Bulk components

- 6.3.1 Monolithic components

- 6.3.2 Composite components

- 6.4 Coatings

- 6.4.1 Thermal barrier coatings

- 6.4.2 Oxidation-resistant coatings

- 6.4.3 Erosion-resistant coatings

- 6.4.4 Other coating types

- 6.5 Fibers & whiskers

- 6.6 Other product forms

Chapter 7 Market Size and Forecast, By Manufacturing Method, 2021-2034 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Hot pressing

- 7.3 Spark plasma sintering (SPS)

- 7.4 Reactive hot pressing

- 7.5 Pressureless sintering

- 7.6 Chemical vapor deposition (CVD)

- 7.7 Additive manufacturing

- 7.8 Other manufacturing methods

Chapter 8 Market Size and Forecast, By Application, 2021-2034 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 Thermal protection systems

- 8.2.1 Hypersonic vehicle leading edges

- 8.2.2 Reentry vehicle heat shields

- 8.2.3 Rocket nozzle throats

- 8.2.4 Combustion chamber liners

- 8.2.5 Other thermal protection applications

- 8.3 Propulsion systems

- 8.3.1 Rocket engine components

- 8.3.2 Gas turbine components

- 8.3.3 Scramjet components

- 8.3.4 Other propulsion applications

- 8.4 High-temperature sensors & instrumentation

- 8.5 Cutting tools & wear-resistant components

- 8.6 Furnace elements & crucibles

- 8.7 Nuclear applications

- 8.8 Other applications

Chapter 9 Market Size and Forecast, By End Use Industry, 2021-2034 (USD Billion) (Tons)

- 9.1 Key trends

- 9.2 Aerospace & defense

- 9.2.1 Military aerospace

- 9.2.2 Civil aerospace

- 9.2.3 Space exploration

- 9.2.4 Missile systems

- 9.2.5 Other aerospace & defense applications

- 9.3 Industrial

- 9.3.1 Metal processing

- 9.3.2 Glass manufacturing

- 9.3.3 Chemical processing

- 9.3.4 Other industrial applications

- 9.4 Energy

- 9.4.1 Nuclear energy

- 9.4.2 Fossil fuel power generation

- 9.4.3 Other energy applications

- 9.5 Electronics & semiconductor

- 9.6 Research & academia

- 9.7 Other end use industries

Chapter 10 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Rest of Middle East & Africa

Chapter 11 Company Profiles

- 11.1 Lockheed Martin Corporation

- 11.2 Rolls-Royce

- 11.3 Ultramet

- 11.4 BAE Systems

- 11.5 3M Company

- 11.6 CoorsTek

- 11.7 Morgan Advanced Materials

- 11.8 Kennametal

- 11.9 Aremco Products

- 11.10 Advanced Ceramics Manufacturing

- 11.11 Precision Ceramics USA

- 11.12 Kyocera Corporation

- 11.13 Saint-Gobain