|

市場調査レポート

商品コード

1766202

光線療法機器の市場機会、成長促進要因、産業動向分析、2025~2034年予測Phototherapy Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 光線療法機器の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年06月10日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

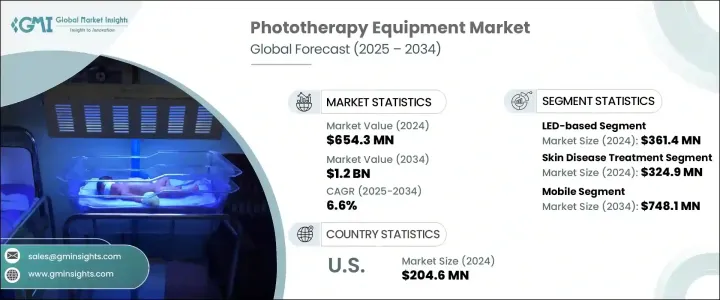

光線療法機器の世界市場は、2024年に6億5,430万米ドルと評価され、CAGR 6.6%で成長し、2034年には12億米ドルに達すると予測されています。

この増加傾向は、主に皮膚関連疾患の有病率の増加、新生児黄疸の発生率の上昇、光線療法技術の急速な革新によってもたらされます。白斑、乾癬、にきび、湿疹などの治療が一般的になりつつあり、非侵襲的な治療法として光線療法への依存が高まっています。これらの機器の普及は、新生児や皮膚科疾患の治療改善を優先するヘルスケアインフラの成長によって強化されています。LEDベースの技術、ウェアラブル・ソリューション、高精度波長照射など、光線療法システムの進歩は、特に熱曝露を最小限に抑え、使用者の快適性を高めることによって、これらの治療をより安全で効果的なものにしています。

紫外線、赤色、青色など特定の波長帯域の光を使用する機器は、新生児のビリルビン分解や慢性皮膚疾患の炎症抑制など、標的とする生物学的反応を誘発することにより、著しい治療効果を示しています。これらの波長は、さまざまな深さで皮膚に浸透するように注意深く選択されているため、周囲の組織を損傷することなく、特定の症状に対して的確な治療を行うことができます。紫外線は、過剰な皮膚細胞の成長を遅らせることにより、乾癬のような自己免疫性皮膚疾患の管理に特に効果的です。抗炎症作用で知られる赤色光は、組織の修復をサポートし、炎症を抑えるため、湿疹や創傷治癒に有用です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 6億5,430万米ドル |

| 予測金額 | 12億米ドル |

| CAGR | 6.6% |

2024年には、LEDベースのシステムが3億6,140万米ドルの評価額で市場をリードしました。これらの機器は、エネルギー効率、低発熱、長寿命が支持され、特に新生児に安全です。臨床と家庭の両方で使用が拡大しているのは、その携帯性と、白斑、乾癬、にきびなどの皮膚科疾患の治療で実証された成果によるところが大きいです。制御された正確で均一な光治療を最小限の副作用で提供できることから、LEDベースのソリューションはヘルスケアプロバイダの間で好ましい選択肢となっています。

モバイル光線療法機器セグメントは、2034年には7億4,810万米ドルに達すると予測されています。これらのモバイルシステムは、使いやすさ、操作の柔軟性、ヘルスケア施設と自宅治療環境の両方への適合性を提供します。新生児黄疸の治療における有用性は大きく、特に可動性によって治療へのアクセス性と効率が高まるからです。皮膚科の分野では、これらのポータブル・ユニットは外来診療に理想的であり、固定設備を必要とせず、より的を絞った治療を可能にします。在宅医療を選択する患者が増えるにつれ、コスト削減と利便性から、モバイル光線療法機器の需要は増加の一途をたどっています。

米国の光線療法機器市場は2024年に2億460万米ドルを占める。医療インフラが整備されていること、皮膚疾患の有病率が高いこと、新生児治療ソリューションに注力し続けていることなどから、同国は光線療法分野で強力な足場を維持しています。光ファイバーシステムや先進的なLEDユニットなどの治療機器は、非侵襲的な治療嗜好の高まりや意識の高まりに支えられ、病院環境と在宅ケアの両方でますます利用されるようになっています。その結果、米国における需要は、一貫した医療の進歩と、患者の快適さと手頃な価格への重点の高まりによって促進されています。

光線療法機器市場を積極的に形成している主要企業は、SolRx、Ibis Medical、Natus、Neotech、PHOENIX、GE HealthCare、DAVID、UVBioTek、ATOM MEDICAL、MEDI WAVES、OKUMAN、Phothera、NARANG MEDICAL LIMITED、PHILIPSなどです。光線療法機器市場の主要企業は、その存在感を高めるため、LED技術、ウェアラブル光治療、個別波長制御を提供するシステムに焦点を当て、製品イノベーションに多額の投資を行っています。いくつかの企業は、世界な販売網を拡大し、病院や診療所と戦略的パートナーシップを結んで顧客基盤を広げています。さらに、遠隔治療をサポートし、患者の転帰を改善するために、IoTやデジタルモニタリング機能を機器に組み込んでいる企業も多いです。マーケティング活動では、ヘルスケアプロバイダーとエンドユーザーの双方を惹きつけるため、非侵襲的な利点と臨床的成功を強調しています。また、便利で費用対効果の高い治療ソリューションに対する需要の高まりに対応するため、各社は小型モデルや家庭用モデルにも注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 新生児黄疸の有病率の上昇

- 増加する皮膚疾患

- 光線療法機器の技術的進歩

- 新生児ケアに対する政府の支援策

- 業界の潜在的リスク&課題

- 代替治療法の利用可能性

- 開発途上地域では製品コストが高く、アクセスが制限される

- 機会

- 在宅ヘルスケアの台頭

- スマート光線療法機器の導入

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 製品別の価格動向

- 将来の市場動向

- 償還シナリオ

- 償還政策が市場成長に与える影響

- 消費者行動分析

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- 世界のその他の地域

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- LEDベース

- 従来型

- 光ファイバー

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 皮膚疾患の治療

- 新生児黄疸の管理

- その他の用途

第7章 市場推計・予測:モダリティ別、2021年~2034年

- 主要動向

- モバイル

- 固定

- ウェアラブル

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院と診療所

- ホームケア

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- ATOM MEDICAL

- DAVID

- GE HealthCare

- Ibis Medical

- MEDI WAVES

- NARANG MEDICAl LIMITED

- natus

- Neotech

- OKUMAN

- PHILIPS

- PHOENIX

- Phothera

- SolRx

- UVBioTek

The Global Phototherapy Equipment Market was valued at USD 654.3 million in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 1.2 billion by 2034. This upward trend is primarily driven by the increasing prevalence of skin-related ailments, rising incidences of neonatal jaundice, and rapid innovation in phototherapy technologies. Conditions like vitiligo, psoriasis, acne, and eczema are becoming more common, increasing the reliance on phototherapy as a non-invasive treatment method. The widespread adoption of these devices is reinforced by the growing healthcare infrastructure that prioritizes improved treatment for newborns and dermatological conditions. Advancements in phototherapy systems, including LED-based technology, wearable solutions, and precision wavelength delivery, have made these treatments safer and more effective, particularly by minimizing heat exposure and enhancing user comfort.

Devices using specific bands of light, such as UV, red, or blue, have shown significant therapeutic effects by triggering targeted biological responses, such as bilirubin breakdown in newborns or inflammation reduction in chronic skin diseases. These wavelengths are carefully selected to penetrate the skin at varying depths, allowing for precise treatment of specific conditions without damaging surrounding tissue. UV light is particularly effective in managing autoimmune skin disorders like psoriasis by slowing down excessive skin cell growth. Red light, known for its anti-inflammatory properties, supports tissue repair and reduces irritation, making it useful for eczema and wound healing.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $654.3 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 6.6% |

In 2024, LED-based systems led the market with a valuation of USD 361.4 million. These devices are favored for their energy efficiency, low heat output, and extended operational life, making them particularly safe for neonates. Their growing use in both clinical and home settings is largely due to their portability and proven outcomes in treating dermatological disorders like vitiligo, psoriasis, and acne. The ability to deliver controlled, precise, and uniform light therapy with minimal side effects is positioning LED-based solutions as a preferred choice among healthcare providers.

The mobile phototherapy device segment is projected to reach USD 748.1 million by 2034. These mobile systems offer ease of use, operational flexibility, and compatibility with both healthcare facilities and at-home treatment environments. Their utility in treating neonatal jaundice is significant, particularly because mobility enhances treatment accessibility and efficiency. In the field of dermatology, these portable units are ideal for outpatient clinics, enabling more targeted care without requiring fixed installations. As more patients opt for home-based care solutions, the demand for mobile phototherapy equipment continues to climb due to cost savings and convenience.

U.S. Phototherapy Equipment Market accounted for USD 204.6 million in 2024. The country maintains a strong foothold in the phototherapy space due to its well-developed healthcare infrastructure, high prevalence of skin conditions, and continued focus on neonatal treatment solutions. Devices such as fiber optic systems and advanced LED units are increasingly utilized in both hospital settings and home care, supported by a rise in non-invasive treatment preferences and heightened awareness. As a result, demand in the U.S. is fueled by consistent medical advancements and the growing emphasis on patient comfort and affordability.

Key players actively shaping the Phototherapy Equipment Market include SolRx, Ibis Medical, Natus, Neotech, PHOENIX, GE HealthCare, DAVID, UVBioTek, ATOM MEDICAL, MEDI WAVES, OKUMAN, Phothera, NARANG MEDICAL LIMITED, and PHILIPS. To enhance their presence, companies in the phototherapy equipment market are investing heavily in product innovation, focusing on LED technology, wearable light therapy, and systems offering personalized wavelength control. Several players are expanding their global distribution networks and entering strategic partnerships with hospitals and clinics to broaden their customer base. Additionally, many are integrating IoT and digital monitoring capabilities into devices to support remote care and improve patient outcomes. Marketing efforts emphasize non-invasive benefits and clinical success to attract both healthcare providers and end-users. Companies are also focusing on compact and home-use models to cater to the increasing demand for convenient and cost-effective therapy solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 Modality

- 2.2.5 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of neonatal jaundice

- 3.2.1.2 Growing skin disorders

- 3.2.1.3 Technological advancements in phototherapy devices

- 3.2.1.4 Supportive government initiatives for newborn care

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Availability of alternative treatments

- 3.2.2.2 High product cost and limited accessibility in underdeveloped regions

- 3.2.3 Opportunities

- 3.2.3.1 Rising trend of home healthcare

- 3.2.3.2 Adoption of smart phototherapy devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends, by product

- 3.7 Future market trends

- 3.8 Reimbursement scenario

- 3.8.1 Impact of reimbursement policies on market growth

- 3.9 Consumer behaviour analysis

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Rest of the world

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 LED-based

- 5.3 Conventional

- 5.4 Fiberoptic

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Skin disease treatment

- 6.3 Neonatal jaundice management

- 6.4 Other applications

Chapter 7 Market Estimates and Forecast, By Modality, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Mobile

- 7.3 Fixed

- 7.4 Wearable

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and clinics

- 8.3 Homecare

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ATOM MEDICAL

- 10.2 DAVID

- 10.3 GE HealthCare

- 10.4 Ibis Medical

- 10.5 MEDI WAVES

- 10.6 NARANG MEDICAl LIMITED

- 10.7 natus

- 10.8 Neotech

- 10.9 OKUMAN

- 10.10 PHILIPS

- 10.11 PHOENIX

- 10.12 Phothera

- 10.13 SolRx

- 10.14 UVBioTek