|

市場調査レポート

商品コード

1766195

AACブロックの市場機会、成長促進要因、産業動向分析、2025年~2034年予測AAC (Autoclaved Aerated Concrete) Blocks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| AACブロックの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月10日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

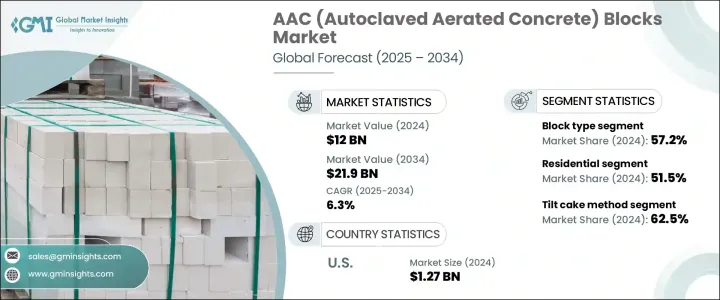

AAC(自動気泡コンクリート)ブロックの世界市場規模は2024年に120億米ドルとなり、CAGR6.3%で推移し、2034年には219億米ドルに達すると予測されています。

この市場は、環境負荷を低減する建築材料への需要が高まるにつれて着実に拡大しています。AACブロックは軽量で持続可能であり、安全な天然原材料と産業廃棄物を使用して製造されるため、従来のレンガに代わる環境に優しい材料として認知されています。AACブロックの製造工程で消費されるエネルギーは、赤土レンガよりも約30%少なく、二酸化炭素排出量の大幅な削減に貢献します。インドのような急成長する経済圏では、AACブロックが国の持続可能性目標をサポートし、エネルギー効率の高い建設基準に合致していることから、AACブロックが勢いを増しています。

AACブロックが提供する断熱性能は、室内の余分な熱を防ぎ、冷房システムへの依存を軽減します。これは、電力使用量の削減、コスト削減、環境保全に貢献します。インドなどでは、政府機関が後押しするエネルギー効率基準が、不動産や公共インフラでのAAC採用をさらに後押ししています。急速な都市成長、進行中のインフラ開発、スマートシティ構想の下での環境に配慮した建設へのシフトは、いずれも市場拡大に拍車をかけています。また、AACブロックは運搬や設置が容易なため、建設時間や労力を削減できる点でも好まれています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 120億米ドル |

| 予測金額 | 219億米ドル |

| CAGR | 6.3% |

製品タイプ別では、ブロックの変種が2024年のシェア57.2%で市場を独占しています。標準サイズのブロックは、コスト、重量、断熱性のバランスが良好なため、住宅建築と商業建築の両方で広く使用されています。より大規模なプロジェクトでは、目地数を減らして壁の施工を迅速化するため、ジャンボブロックの使用が増加しています。まぐさやUブロックのような補完的な形状は、構造支持や電線管通過のための付加価値ソリューションとして普及しつつあり、多くの場合、型枠を追加する必要がなくなります。

製造方法は、AAC市場のもうひとつの重要な要素です。2024年の市場シェアは、ティルトケーキ工法が62.5%でリードしています。この工法は、ブロックを垂直に切断する前にミックスを部分的に硬化させるもので、大量生産と最適な垂直スペース利用を可能にします。業界で最も確立された方法であり、拡張性には理想的です。しかし、トリミングによる材料の無駄が増える可能性があり、最新の自動化技術に比べ、より多くの手作業が必要となります。

米国のAAC(自動気泡コンクリート)ブロック市場は2024年に85%のシェアを占め、評価額は12億7,000万米ドルでした。同国の成長は、堅調なインフラ開発と環境に優しい代替建築物に対する需要の急増に結びついています。国内生産能力はこの需要を満たすために拡大しており、輸入材料への依存を減らして市場アクセスや配送効率を向上させています。これにより、米国の建設部門における主要材料としてのAACの地位はさらに強固なものとなっています。

世界のAAC(自動気泡コンクリート)ブロック市場を形成している主要企業には、Aercon AAC、H+H International A/S、CSR Limited(Hebel)、ACICO Industries Company、Xella Groupなどがあります。これらのプレーヤーは、技術革新、足跡の拡大、強力な流通戦略を通じて競争力を維持しています。市場での存在感を高めるため、AACブロックメーカーは生産能力の拡大、需要の高い地域での工場設立、建設会社との合弁事業参入といった戦略的な動きに注力しています。多くの企業は、無駄を省き製品の一貫性を高めるために製造技術を強化しています。特定の建築機能に対応するためのブロック設計の革新や、規制やグリーンビルディングの枠組みにおけるAACの推進努力も、重要な戦略となってきています。さらに、請負業者や建築家にAACブロックの利点を啓蒙することが、新興市場でも成熟市場でも幅広い採用を支えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 持続可能な建設資材の需要の高まり

- エネルギー効率と断熱効果

- 急速な都市化とインフラ開発

- 軽量性と施工スピードのメリット

- 業界の潜在的リスク&課題

- 原材料価格の変動

- 輸送コストと物流

- 熟練労働者の不足

- 地域の建築基準法の遵守

- 市場機会

- グリーンビルディング認証プログラム

- 製造業における技術の進歩

- 新興市場への拡大

- プレハブおよびモジュール建設の成長

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- ブロックタイプ

- 標準ブロック

- ジャンボブロック

- リンテルブロック

- U字型ブロック

- その他

- サイズ

- 小型(長さ400mmまで)

- 中型(長さ400~600mm)

- 大型(長さ600mm以上)

第6章 市場推計・予測:原材料別、2021年~2034年

- 主要動向

- セメント

- ライム

- フライアッシュ

- 珪砂/石英砂

- アルミニウム粉末

- 石膏

- その他

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 壁の建設

- 外壁

- 内壁

- 間仕切り壁

- 屋根断熱材

- 床

- リンテル

- クラッディングパネル

- その他

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 住宅建設

- 一戸建て住宅

- 集合住宅

- 手頃な価格の住宅プロジェクト

- 商業建設

- オフィスビル

- 小売スペース

- ホテルとホスピタリティ

- 教育機関

- ヘルスケア施設

- 産業建設

- 製造工場

- 倉庫

- その他

- インフラ開発

- その他

第9章 市場推計・予測:製造方法別、2021年~2034年

- 主要動向

- ティルトケーキ法

- フラットケーキ法

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第11章 企業プロファイル

- ACICO Industries Company

- Aercon AAC

- AKG Gazbeton

- Biltech Building Elements Limited

- Broco Industries

- Buildmate Projects Pvt. Ltd

- CSR Limited(Hebel)

- Eastland Building Materials Co., Ltd.

- H+H International A/S

- JK Lakshmi Cement Ltd.

- Magicrete Building Solutions Pvt. Ltd.

- Solbet Sp. z o.o

- UAL Industries Limited

- Xella Group

The Global AAC (Autoclaved Aerated Concrete) Blocks Market was valued at USD 12 billion in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 21.9 billion by 2034. This market is expanding steadily as demand increases for building materials that reduce environmental impact. AAC blocks are recognized for being lightweight, sustainable, and made using safe, natural raw materials and industrial waste-making them a green alternative to conventional bricks. Their production process consumes around 30% less energy than red clay bricks, contributing to significantly lower carbon emissions. In fast-growing economies like India, these materials are gaining momentum as they support national sustainability goals and align with energy-efficient construction norms.

The thermal insulation offered by AAC blocks helps prevent excess indoor heat, reducing reliance on cooling systems. This contributes to lower power usage, cost savings, and environmental benefits. Energy efficiency standards backed by government agencies in countries such as India further encourage AAC adoption in real estate and public infrastructure. Rapid urban growth, ongoing infrastructure development, and a shift toward environmentally sound construction under smart city initiatives are all fueling market expansion. AAC blocks are also preferred for being easy to transport and install, reducing construction time and labor.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12 Billion |

| Forecast Value | $21.9 Billion |

| CAGR | 6.3% |

In terms of product type, block variants dominated the market with a 57.2% share in 2024. Standard-sized blocks are widely used in both residential and commercial construction due to their favorable balance of cost, weight, and insulation. For larger-scale projects, jumbo blocks are increasingly used to reduce the number of joints and speed up wall installation. Complementary shapes like lintels and U-blocks are becoming more prevalent as value-added solutions for structural support and conduit passage, often eliminating the need for additional formwork.

Production methods are another key factor in the AAC market. The tilt cake method led with a 62.5% market share in 2024. This method involves partially curing the mix before cutting the blocks vertically, allowing high-volume output and optimal vertical space usage. It remains the most established method in the industry, ideal for scalability. However, it may create additional material waste due to trimming and requires more manual input than newer automated techniques.

United States AAC (Autoclaved Aerated Concrete) Blocks Market held 85% share in 2024, with a valuation of USD 1.27 billion. The country's growth is tied to robust infrastructure development and a surge in demand for green construction alternatives. Domestic production capacity is expanding to meet this demand and reduce reliance on imported materials, ensuring better market access and delivery efficiency. This has further strengthened the position of AAC as a key material in the US construction sector.

Major companies shaping the Global AAC (Autoclaved Aerated Concrete) Blocks Market include Aercon AAC, H+H International A/S, CSR Limited (Hebel), ACICO Industries Company, and Xella Group. These players remain competitive through innovation, expanding footprints, and strong distribution strategies. To boost their market presence, AAC block manufacturers are focusing on strategic moves such as capacity expansion, plant setup in high-demand regions, and entering joint ventures with construction firms. Many companies are enhancing their manufacturing technologies to reduce waste and improve product consistency. Innovation in block design to cater to specific building functions, and efforts to promote AAC in regulatory and green building frameworks, are also becoming critical strategies. Additionally, educating contractors and architects about the benefits of AAC blocks supports wider adoption across both emerging and mature markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Raw Material

- 2.2.4 Application

- 2.2.5 End use industry

- 2.2.6 Production process

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for sustainable construction materials

- 3.2.1.2 Energy efficiency and thermal insulation benefits

- 3.2.1.3 Rapid urbanization and infrastructure development

- 3.2.1.4 Lightweight properties and construction speed advantages

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Raw material price fluctuations

- 3.2.2.2 Transportation costs and logistics

- 3.2.2.3 Skilled labor shortages

- 3.2.2.4 Regional building code compliance

- 3.2.3 Market opportunities

- 3.2.3.1 Green building certification programs

- 3.2.3.2 Technological advancements in manufacturing

- 3.2.3.3 Expansion in emerging markets

- 3.2.3.4 Prefabricated and modular construction growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Block type

- 5.2.1 Standard blocks

- 5.2.2 Jumbo blocks

- 5.2.3 Lintel blocks

- 5.2.4 U-shaped blocks

- 5.2.5 Others

- 5.3 Size

- 5.3.1 Small (Up to 400mm Length)

- 5.3.2 Medium (400-600mm Length)

- 5.3.3 Large (Above 600mm Length)

Chapter 6 Market Estimates and Forecast, By Raw Material, 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cement

- 6.3 Lime

- 6.4 Fly Ash

- 6.5 Silica sand/quartz sand

- 6.6 Aluminum powder

- 6.7 Gypsum

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Wall construction

- 7.2.1 External walls

- 7.2.2 Internal walls

- 7.2.3 Partition walls

- 7.3 Roof insulation

- 7.4 Floor elements

- 7.5 Lintels

- 7.6 Cladding panels

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Residential construction

- 8.2.1 Single-family homes

- 8.2.2 Multi-family buildings

- 8.2.3 Affordable housing projects

- 8.3 Commercial construction

- 8.3.1 Office buildings

- 8.3.2 Retail spaces

- 8.3.3 Hotels and hospitality

- 8.3.4 Educational institutions

- 8.3.5 Healthcare facilities

- 8.4 Industrial construction

- 8.4.1 Manufacturing plants

- 8.4.2 Warehouses

- 8.4.3 Others

- 8.5 Infrastructure development

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Production Method, 2021 – 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Tilt cake method

- 9.3 Flat cake method

- 9.4 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 ACICO Industries Company

- 11.2 Aercon AAC

- 11.3 AKG Gazbeton

- 11.4 Biltech Building Elements Limited

- 11.5 Broco Industries

- 11.6 Buildmate Projects Pvt. Ltd

- 11.7 CSR Limited (Hebel)

- 11.8 Eastland Building Materials Co., Ltd.

- 11.9 H+H International A/S

- 11.10 JK Lakshmi Cement Ltd.

- 11.11 Magicrete Building Solutions Pvt. Ltd.

- 11.12 Solbet Sp. z o.o

- 11.13 UAL Industries Limited

- 11.14 Xella Group