|

市場調査レポート

商品コード

1766191

OTC持続グルコースモニタリング(OTC CGM)の市場機会、成長促進要因、産業動向分析、予測、2025年~2034年OTC Continuous Glucose Monitoring Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| OTC持続グルコースモニタリング(OTC CGM)の市場機会、成長促進要因、産業動向分析、予測、2025年~2034年 |

|

出版日: 2025年06月03日

発行: Global Market Insights Inc.

ページ情報: 英文 108 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

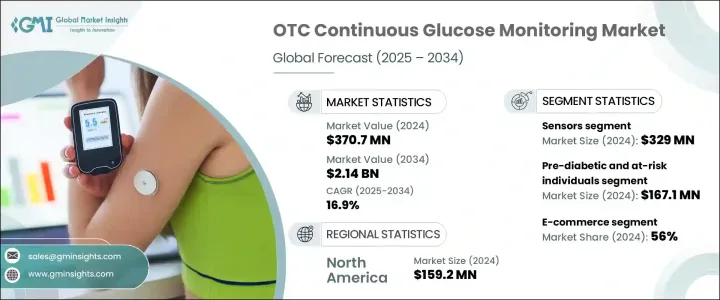

世界のOTC持続グルコースモニタリング(OTC CGM)市場は、2024年に3億7,070万米ドルと評価され、2034年には21億4,000万米ドルに達し、CAGRで16.9%の成長が予測されています。

処方箋なしで購入できるOTC CGMは、糖尿病の管理だけでなく、より広範な健康モニタリング用途でもますます重要な役割を果たしています。これらの機器により、消費者は自分のグルコース値をリアルタイムで追跡することができ、食事、運動、全体的な健康状態について十分な情報に基づいた決定を下すことができるようになります。個人の健康情報に対する需要が高まるにつれ、これらのシステムは予防ヘルスケアや個人に合わせた栄養管理のために受け入れられています。センサー技術の進歩、コンパクトなデザイン、長時間の装着性、スマートフォンやAIプラットフォームとのシームレスな統合により、OTC CGMはより使いやすく、より多くの人が利用できるようになってきています。

メーカーとデジタルプラットフォームは、消費者の全体的な製品体験を向上させるために、ますます協力するようになっています。高度なアナリティクスを統合し、パーソナライズされたライフスタイルコーチングを提供することで、これらのコラボレーションは、ユーザーにとってより魅力的で価値主導の体験を生み出しています。消費者は現在、自分の健康に関する洞察をリアルタイムで利用できるようになり、日々の選択がグルコース値や健康全般にどのような影響を与えるかを理解するのに役立っています。このパーソナライズされたフィードバックは、単にグルコース値のモニタリングにとどまらず、食事、運動、睡眠パターンの最適化など、実行可能な健康目標の作成にまで広がっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 3億7,070万米ドル |

| 予測金額 | 21億4,000万米ドル |

| CAGR | 16.9% |

センサーセグメントは、2024年に3億2,900万米ドルとなり、最大のシェアを占めています。コンパクトで、快適で使いやすいウェアラブルへの嗜好の高まりが、より革新的なセンサーの開発に拍車をかけています。これらのセンサーには現在、グラフェン、柔軟なポリマー、伸縮可能なエレクトロニクスなどの先進素材が組み込まれ、快適性と測定精度が向上しています。これらのセンサーをウェアラブルやスマートフォンと統合することで、リアルタイムの接続とデータ転送が可能になり、ユーザーエクスペリエンスが向上し、CGMの利用範囲が広がります。

eコマースセグメントは2024年に56%のシェアを占めます。この成長の原動力となっているのは、消費者行動の変化であり、健康志向の高い人々は、従来の小売店や臨床の場を迂回して、ウェルネス機器をオンラインで購入することを好みます。eコマースプラットフォームは、消費者にOTC CGMへの直接アクセスを提供し、デジタルヘルスへの旅に大きな自主性をもたらします。このDTCアプローチにより、ブランドはオンラインチャネルを通じてパーソナライズされた教育やサポートを提供し、より効果的に顧客と関わることができます。

米国のOTC持続グルコースモニタリング(OTC CGM)市場は2034年までに11億米ドルに達すると予測されます。特に非糖尿病患者の予防医療への関心の高まりが、この需要を牽引しています。食事、運動、代謝パフォーマンスを最適化するためにCGMを使用する人が増えています。OTC CGMの承認を含むFDAによる規制の進歩は、これらのデバイスの普及をさらに促進しています。CGMとスマートフォンや健康アプリとの統合も、自己管理に対する消費者の信頼を高め、ユーザーがシームレスにグルコースレベルを監視し、パーソナライズされた健康に関する洞察を得ることを可能にしています。この動向は、米国におけるデジタルヘルスツールの高い普及率に支えられており、消費者はパーソナライズされた健康データをますます求めるようになっています。

OTC持続グルコースモニタリング(OTC CGM)市場の主要企業には、Abbott Laboratories、Dexcom、January AI、Levels Health、Limbo(Vitals in View)、Nutrisense、Sinocare、Ultrahuman Healthcare、Veri、Zoeなどがあります。OTC持続グルコースモニタリング(OTC CGM)市場におけるプレゼンスを強化するため、各社はいくつかの戦略を採用しています。まず、センサーの背後にある技術の強化に注力し、柔軟なポリマーや伸縮可能なエレクトロニクスなどの最先端素材を統合して、快適性と精度を向上させています。また、多くの企業がデジタルヘルスプラットフォームと戦略的提携を結び、AIを活用した分析や個人に合わせたコーチングなどの付加サービスを消費者に提供しています。さらに、eコマースへのシフトは多くのメーカーに受け入れられており、オンラインチャネルを通じてより幅広い消費者層に直接リーチできるようになっています。ユーザーフレンドリーなデザインに投資し、教育リソースを提供し、購入プロセスを合理化することで、これらの企業は製品の採用を増やし、強力な顧客ロイヤルティを構築することを目指しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 代謝の健康とウェルネスに対する消費者の関心の高まり

- 消費者直販(DTC)とサブスクリプションモデルの拡大

- 技術の進歩とAIを活用した洞察

- 予防ヘルスケアと長寿の動向の変化

- 業界の潜在的リスク&課題

- 高額な費用と限られた保険適用

- 規制とデータプライバシーに関する懸念

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 世界のその他の地域

- 消費者タイプ別の数量、2024

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- センサー別

- プラットフォーム/アプリ別

- 地域別企業市場ランキング

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推定・予測:コンポーネント別、2021年~2034年

- 主要動向

- センサー

- プラットフォーム/アプリ

第6章 市場推定・予測:消費者タイプ別、2021年~2034年

- 主要動向

- 糖尿病ではない健康志向の人

- 糖尿病予備群・糖尿病リスクのある人

- その他の消費者タイプ

第7章 市場推定・予測:流通チャネル別、2021年~2034年

- 主要動向

- 病院薬局

- 小売薬局

- eコマース

第8章 市場推定・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- 世界のその他の地域

第9章 企業プロファイル

- Abbott Laboratories

- Dexcom

- January AI

- Levels Health

- Limbo(Vitals in View)

- Nutrisense

- Sinocare

- Ultrahuman Healthcare

- Veri

- Zoe

The Global OTC Continuous Glucose Monitoring Market was valued at USD 370.7 million in 2024 and is estimated to grow at a CAGR of 16.9% to reach USD 2.14 billion by 2034. OTC CGMs, which are available for purchase without a prescription, are playing an increasingly significant role not only in managing diabetes but also in broader health monitoring applications. These devices allow consumers to track their glucose levels in real-time, which empowers them to make informed decisions about their diet, exercise, and overall wellness. As the demand for personal health information grows, these systems are being embraced for preventive healthcare and personalized nutrition. With advancements in sensor technology, compact design, longer wearability, and seamless integration with smartphones and AI platforms, OTC CGMs are becoming more user-friendly and accessible to a wider audience.

Manufacturers and digital platforms are increasingly joining forces to improve the overall product experience for consumers. By integrating advanced analytics and offering personalized lifestyle coaching, these collaborations are creating a more engaging and value-driven experience for users. Consumers now have access to insights about their health in real-time, helping them understand how their daily choices impact their glucose levels and overall well-being. This personalized feedback is not just limited to monitoring glucose levels but extends to creating actionable health goals, such as optimizing diet, exercise, and sleep patterns.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $370.7 Million |

| Forecast Value | $2.14 Billion |

| CAGR | 16.9% |

The sensor segment holds the largest share valued at USD 329 million in 2024. The increasing preference for compact, comfortable, and easy-to-use wearables is fueling the development of more innovative sensors. These sensors now incorporate advanced materials such as graphene, flexible polymers, and stretchable electronics to improve comfort and measurement accuracy. The integration of these sensors with wearables and smartphones allows real-time connectivity and data transfer, enhancing the user experience and broadening the scope of CGM usage.

The e-commerce segment held 56% share in 2024. This growth is driven by a shift in consumer behavior, where health-conscious individuals prefer purchasing wellness devices online, bypassing traditional retail and clinical settings. E-commerce platforms offer consumers direct access to OTC CGMs, providing greater autonomy over their digital health journey. This direct-to-consumer approach also enables brands to engage with customers more effectively, offering personalized education and support through online channels.

United States OTC Continuous Glucose Monitoring Market is projected to reach USD 1.1 billion by 2034. The rising interest in preventive health, particularly among non-diabetic individuals, is driving this demand. People are increasingly using CGMs to optimize their diet, exercise, and metabolic performance. Regulatory advancements by the FDA, including approvals for OTC CGMs, are further facilitating the widespread adoption of these devices. The integration of CGMs with smartphones and health apps is also boosting consumer confidence in self-management, enabling users to monitor their glucose levels seamlessly and gain personalized health insights. This trend is supported by the high adoption of digital health tools in the U.S., with consumers increasingly seeking personalized health data.

Key players in the OTC Continuous Glucose Monitoring Market include Abbott Laboratories, Dexcom, January AI, Levels Health, Limbo (Vitals in View), Nutrisense, Sinocare, Ultrahuman Healthcare, Veri, and Zoe. To strengthen their presence in the OTC continuous glucose monitoring market, companies have adopted several strategies. First, they are focusing on enhancing the technology behind their sensors, integrating cutting-edge materials like flexible polymers and stretchable electronics to improve comfort and accuracy. Many companies are also entering strategic partnerships with digital health platforms to provide consumers with additional services, such as AI-powered analytics and personalized coaching. Furthermore, the shift towards e-commerce is being embraced by many manufacturers, allowing them to reach a broader consumer base directly through online channels. By investing in user-friendly designs, providing educational resources, and streamlining the purchase process, these companies aim to increase product adoption and build strong customer loyalty.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer interest in metabolic health and wellness

- 3.2.1.2 Expansion of direct-to-consumer (DTC) and subscription models

- 3.2.1.3 Technological advancements and AI-powered insights

- 3.2.1.4 Shifts in preventive healthcare and longevity trends

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs and limited insurance coverage

- 3.2.2.2 Regulatory and data privacy concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Rest of the World

- 3.5 Volume by consumer type, 2024

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By sensor

- 4.2.2 By platform/app

- 4.3 Company market ranking, by region

- 4.4 Company matrix analysis

- 4.5 Competitive analysis of major market players

- 4.6 Competitive positioning matrix

- 4.7 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Component, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Sensors

- 5.3 Platforms/Apps

Chapter 6 Market Estimates and Forecast, By Consumer Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Non-diabetic health enthusiasts

- 6.3 Pre-diabetic and at-risk individuals

- 6.4 Other consumer types

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Retail pharmacies

- 7.4 E-commerce

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Rest of the World

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Dexcom

- 9.3 January AI

- 9.4 Levels Health

- 9.5 Limbo (Vitals in View)

- 9.6 Nutrisense

- 9.7 Sinocare

- 9.8 Ultrahuman Healthcare

- 9.9 Veri

- 9.10 Zoe