電子ドラッグデリバリーデバイスの市場機会、成長促進要因、産業動向分析、予測、2025年~2034年

Electronic Drug Delivery Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766184

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

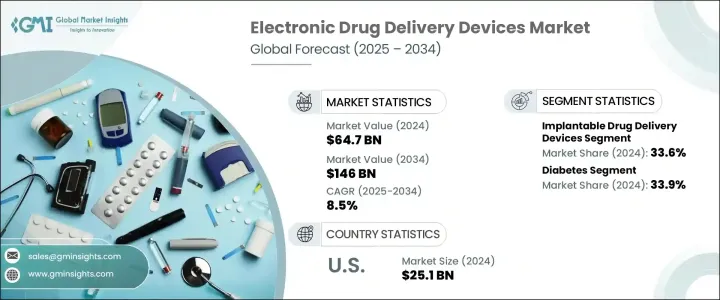

電子ドラッグデリバリーデバイスの世界市場規模は、2024年に647億米ドルとなり、2034年には1,460億米ドルに達し、CAGRで8.5%の成長が予測されています。

これらのデバイスは、ユーザーによる手動開始または自動プログラミングによって電子的に薬剤を投与するように設計された高度なシステムであり、多くの場合、モニタリングとコンプライアンスのために投与イベントを記録します。この技術は、リアルタイムで接続されるセンサーやマイクロプロセッサーと統合されており、事前に設定された治療プロトコルやリアルタイムの生理学的データに基づいて、正確で個別化された薬物送達を可能にします。アドヒアランスの問題に悩まされる可能性のある従来のドラッグデリバリー方法とは異なり、電子デバイスはプログラム可能で正確、かつ患者の立場に立った投薬ソリューションを提供します。

これは、一貫した投薬による治療成績の向上だけでなく、入院やモニタリングのコスト削減にも役立ち、高所得者や資源に乏しいヘルスケア環境において価値があります。がん、心血管疾患、糖尿病、慢性腎臓病などの慢性疾患にしばしば直面する高齢者人口の増加は、電子ドラッグデリバリーシステムの需要を促進する重要な要因です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 647億米ドル |

| 予測金額 | 1,460億米ドル |

| CAGR | 8.5% |

埋込み型ドラッグデリバリーデバイスセグメントは、2024年に33.6%のシェアを占め市場を牽引しました。がん、糖尿病、心臓病などの慢性疾患の増加に伴い、長期的に制御されたドラッグデリバリーシステムに対する需要が大きく伸びています。化学療法ポートや標的送達システムなどの埋め込み型デバイスは、コンプライアンス違反を減らし、臨床転帰を向上させる。プログラム可能なポンプ、標的薬剤溶出インプラント、生分解性インプラントの需要は、疼痛管理や神経学など他の治療分野にも拡大しています。

2024年には、糖尿病セグメントのシェアが33.9%に達します。世界の糖尿病患者数の増加が、持続的なグルコースモニタリングと自動インスリン投与を提供する高度なインスリンポンプやパッチインジェクターのようなデバイスの需要を牽引しています。さらに、規制当局の承認と支援的な償還政策により、糖尿病用の電子ドラッグデリバリーシステムがより広く利用できるようになり、普及を後押ししています。

米国の電子ドラッグデリバリーデバイス市場は、2024年の市場規模が251億米ドルでした。人口の高齢化と慢性疾患の増加に伴い、米国における電子ドラッグデリバリーデバイスの需要は拡大が見込まれています。高度な自動注射器、デジタル吸入器、スマートウェアラブル輸液ポンプの採用が増加しており、その背景には、遠隔外来モニタリング、ヘルスケア支出の増加、価値に基づくケアへのシフトがあります。米国ではデジタル医療インフラが確立されており、コネクテッド医療システムの統合をさらに後押ししています。

電子ドラッグデリバリーデバイスの世界市場の主要企業には、Becton, Dickinson and Company, Pfizer, Medtronic, Insulet, West Pharmaceutical Services, Eli Lilly and Company, Novo Nordisk, Tandem Diabetes Care, Gerresheimer, Ypsomed, AstraZeneca, Abbott Laboratories, SHL Group, Nemera, Sanofiなどがあります。電子ドラッグデリバリーデバイス市場で事業を展開する企業は、その存在感を高めるために様々な戦略を採用しています。その多くは、リアルタイムデータ機能を備えた、より精密で使いやすい機器の開発など、技術革新に注力しています。これらの企業はまた、糖尿病や心血管疾患などの慢性疾患を含む複数の治療領域にわたるソリューションを提供することで、ポートフォリオを拡大しています。医療プロバイダーや規制機関との戦略的パートナーシップは、承認を迅速化し、より広範な市場アクセスを確保するのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 慢性疾患の発生率の上昇

- 在宅ヘルスケアソリューションへの傾向の高まり

- デジタル統合の進歩とパーソナライズされた治療法に関する意識の高まり

- 高齢化人口の増加

- 業界の潜在的リスク&課題

- 高度なドラッグデリバリーデバイスの高コスト

- 患者の意識の低さとデバイス関連の合併症

- 市場機会

- ヘルスケアインフラが限られている新興市場への進出

- 個別投与のためのAIと分析の統合

- 促進要因

- 成長可能性分析

- 規制情勢

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 償還シナリオ

- 償還政策が市場成長に与える影響

- 特許情勢

- 消費者行動分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推定・予測:製品別、2021年~2034年

- 主要動向

- スマート輸液ポンプ

- スマート定量吸入器

- 埋込み型ドラッグデリバリーデバイス

- スマート経皮パッチ

- その他の製品

第6章 市場推定・予測:用途別、2021年~2034年

- 主要動向

- 糖尿病

- 呼吸器疾患

- 腫瘍

- 心臓病

- その他の用途

第7章 市場推定・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第8章 企業プロファイル

- Abbott Laboratories

- AstraZeneca

- Becton, Dickinson and Company

- Eli Lilly and Company

- Gerresheimer

- Haselmeier

- Insulet

- Medtronic

- Nemera

- Novo Nordisk

- Pfizer

- Sanofi

- SHL Group

- Tandem Diabetes Care

- West Pharmaceutical Services

- Ypsomed

目次

The Global Electronic Drug Delivery Devices Market was valued at USD 64.7 billion in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 146 billion by 2034. These devices are advanced systems designed to administer medication electronically, either through manual initiation by the user or automatic programming, and often record dosage events for monitoring and compliance. The technology is integrated with sensors and microprocessors that connect in real-time, enabling the delivery of precise, individualized medication based on pre-set therapeutic protocols and real-time physiological data. Unlike traditional drug delivery methods, which may suffer from adherence issues, electronic devices offer programmable, accurate, and patient-focused medication solutions.

This not only improves treatment outcomes through consistent dosing but also helps reduce hospitalization and monitoring costs, which is valuable in both high-income and resource-constrained healthcare settings. The growing elderly population, who often face chronic diseases like cancer, cardiovascular conditions, diabetes, and chronic kidney disease, is a significant factor driving the demand for electronic drug delivery systems, as these patients require continuous, user-friendly treatments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $64.7 Billion |

| Forecast Value | $146 Billion |

| CAGR | 8.5% |

The implantable drug delivery devices segment led the market in 2024, accounting for 33.6% share. With the increasing prevalence of chronic diseases like cancer, diabetes, and heart conditions, the demand for long-term, controlled drug delivery systems has grown significantly. Implantable devices, such as chemotherapy ports and targeted delivery systems, reduce non-compliance and enhance clinical outcomes. The demand for programmable pumps, targeted drug-eluting implants, and biodegradable implants is also expanding into other therapeutic areas, including pain management and neurology.

In 2024, the diabetes segment represented 33.9% share. The rising number of diabetes cases worldwide has driven demand for devices like advanced insulin pumps and patch injectors that offer continuous glucose monitoring and automatic insulin delivery. Furthermore, regulatory approvals and supportive reimbursement policies have made electronic drug delivery systems for diabetes more widely accessible, boosting adoption.

U.S. Electronic Drug Delivery Devices Market was valued at USD 25.1 billion in 2024. As the population ages and chronic diseases continue to rise, the demand for electronic drug delivery devices in the U.S. is expected to grow. The adoption of advanced autoinjectors, digital inhalers, and smart wearable infusion pumps has increased, driven by remote outpatient monitoring, rising healthcare spending, and a shift toward value-based care. The well-established digital health infrastructure in the U.S. further supports the integration of connected medical systems, which fuels the market for these devices.

Major players in the Global Electronic Drug Delivery Devices Market include Becton, Dickinson and Company, Pfizer, Medtronic, Insulet, West Pharmaceutical Services, Eli Lilly and Company, Novo Nordisk, Tandem Diabetes Care, Gerresheimer, Ypsomed, AstraZeneca, Abbott Laboratories, SHL Group, Nemera, and Sanofi. Companies operating in the electronic drug delivery devices market employ various strategies to strengthen their presence. Many are focusing on technological innovation, such as the development of more precise, user-friendly devices with real-time data capabilities. These companies are also expanding their portfolios by offering solutions across multiple therapeutic areas, including chronic diseases like diabetes and cardiovascular conditions. Strategic partnerships with healthcare providers and regulatory bodies help expedite approvals and ensure broader market access.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of chronic diseases

- 3.2.1.2 Increasing inclination toward home-based healthcare solutions

- 3.2.1.3 Advancements in digital integration and heightened awareness around personalized therapeutics

- 3.2.1.4 Growing geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced drug delivery devices

- 3.2.2.2 Low patient awareness and device-related complications

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets with limited healthcare infrastructure

- 3.2.3.2 Integration of AI and analytics for personalized dosing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Reimbursement scenario

- 3.11.1 Impact of reimbursement policies on market growth

- 3.12 Patent landscape

- 3.13 Consumer behaviour analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Smart infusion pumps

- 5.3 Smart metered dose inhalers

- 5.4 Implantable drug delivery devices

- 5.5 Smart transdermal patches

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Diabetes

- 6.3 Respiratory diseases

- 6.4 Oncology

- 6.5 Cardiology

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott Laboratories

- 8.2 AstraZeneca

- 8.3 Becton, Dickinson and Company

- 8.4 Eli Lilly and Company

- 8.5 Gerresheimer

- 8.6 Haselmeier

- 8.7 Insulet

- 8.8 Medtronic

- 8.9 Nemera

- 8.10 Novo Nordisk

- 8.11 Pfizer

- 8.12 Sanofi

- 8.13 SHL Group

- 8.14 Tandem Diabetes Care

- 8.15 West Pharmaceutical Services

- 8.16 Ypsomed

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日