分散型温度センシング(DTS)の市場機会、成長促進要因、産業動向分析、予測、2025年~2034年

Distributed Temperature Sensing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766177

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

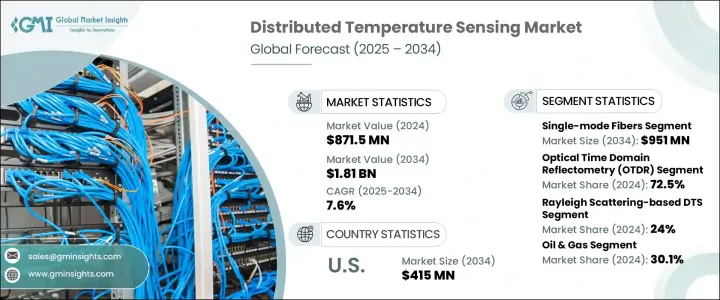

分散型温度センシング(DTS)の世界市場は、2024年には8億7,150万米ドルとなり、2034年には18億1,000万米ドルに達し、CAGRで7.6%の成長が予測されています。

産業用IoT技術の採用が増加していることが、この市場の推進に重要な役割を果たしています。産業界では、安全性と業務効率を高めるためにデジタルシステムへの移行が進んでおり、正確なリアルタイムデータを提供する温度監視ソリューションへのニーズが高まっています。分散型温度センシング(DTS)は、長距離での継続的な温度測定を提供することで、この需要に応えています。これにより、異常の早期発見が可能となり、システム障害の防止や潜在的な危険状態の回避に役立ちます。

データセンターインフラの拡大、都市化、電気自動車の利用増加に伴う電力消費の急増は、電力会社や産業事業者にスマートな電力網ソリューションの採用を促しています。DTSシステムは熱負荷を管理し、グリッドの信頼性を向上させるため、こうした開発には不可欠です。これらのセンシングシステムは、地下や架空送電線、配電ノード、変電所などの厳しい環境に一般的に配備されています。電力ケーブルの過熱や応力を検出する能力により、現代のエネルギーインフラには欠かせないものとなっています。産業界がリスクの軽減と資産寿命の向上を目指す中、DTSの需要は着実に高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 8億7,150万米ドル |

| 予測金額 | 18億1,000万米ドル |

| CAGR | 7.6% |

ファイバータイプ別では、シングルモードファイバーが大きな成長を記録し、その市場価値は2034年までに9億5,100万米ドルに達すると予測されています。これらのファイバーは、長距離の高速データ転送を必要とするアプリケーションに適しています。信号損失を最小限に抑えてデータを伝送する固有の能力と高い帯域幅容量により、最新の通信や産業用セットアップに最適です。ネットワーク接続が世界的に拡大するにつれ、特に次世代ブロードバンドや無線システムの開発により、DTSアプリケーションにおけるシングルモードファイバーの使用は増加の一途をたどっています。これらのファイバーは、分散型センサーがケーブルの長さに沿って温度変化を正確に測定することを可能にします。

技術別に分析すると、市場は光時間領域反射率法(OTDR)と光周波数領域反射率法(OFDR)に区分されます。OTDRは、2024年の世界市場の72.5%を占め、依然として支配的な技術です。OTDRは、光ファイバーネットワークの障害検出や導通確認における精度の高さで広く受け入れられています。OTDRは、正確な障害点、スプライス損失、ファイバー断線を特定することにより、効率的な保守を可能にします。OTDRを使用するDTSシステムは、後方散乱光を解析してファイバー長全体の温度プロファイルを決定し、リアルタイムの監視機能を強化します。

動作原理別では、市場はレイリー散乱ベース、ラマン散乱ベース、ブリルアン散乱ベースのDTSシステムに区分されます。このうち、レイリー散乱ベースのDTSは2024年に市場シェアの24%を獲得しました。この技術は、きめ細かな温度監視を必要とする環境に特に適しています。詳細な熱分析が可能なため、温度スパイクの早期発見が重要な業務をサポートします。高リスクゾーンで操業する業界では、重大な故障が発生する前に一貫した監視と問題解決を確実にするため、このような技術への依存度が高まっています。

アプリケーション別では、DTSシステムは電力ケーブルの監視、火災検知、パイプライン管理、環境評価など、さまざまな産業で使用されています。しかし、石油・ガス用途が2024年には30.1%と最大のシェアを占めています。これらの分野では、作業効率と安全性を確保するため、長距離にわたる継続的な温度監視が必要となります。DTSソリューションは、こうしたニーズをサポートするために必要な精度と信頼性を提供し、性能の最適化と予防保全に貢献します。

地域別分析では、米国が主要市場として際立っており、2034年までに4億1,500万米ドルに達するとの予測が出ています。国内では、DTSシステムが坑井や送電網のリアルタイム熱モニタリング用に広く導入されています。老朽化したインフラの近代化に重点を置いた取り組みにより、高度な温度検知ソリューションの採用が勢いを増しています。これらのシステムは、効率的な負荷管理と性能問題の早期発見をサポートし、計画外停止のリスクを低減します。

市場競争は激しく、Schlumberger Limited、Halliburton Company、AP Sensing GmbH、Silixa Ltd.、Bandweaver Technologiesなどの主要企業が世界売上高の43.3%以上を占めています。リーダーシップを維持し、進化する業界の需要に対応するため、各社は測定精度と環境耐久性を向上させる次世代ファイバー材料とセンサー技術に多額の投資を行っています。リアルタイムで高精度なモニタリングに対する需要の高まりに対応するため、分解能を向上させたコンパクトでエネルギー効率の高いDTSシステムが導入されています。

AIを活用した診断と分析もDTSソリューションに統合され、予知保全をサポートし、システムの信頼性を高めています。業界各社は、特定の産業課題に合わせてカスタマイズしたDTS構成を提供することで、ユーザーのニーズに応えています。さらに、戦略的パートナーシップ、買収、協力関係は、技術的能力と地理的範囲を拡大する上で中心的な存在となっています。また、規制機関や公益事業者と協力することで、企業はDTSが進化する環境・安全基準に適合していることを保証しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 高度なパイプライン監視の需要増加

- 火災検知・予防システムの必要性の高まり

- 電力網インフラへの投資増加

- 光ファイバーセンシングの技術的進歩

- スマートインフラと産業用IoT(IIoT)の拡大

- 業界の潜在的リスク&課題

- 初期資本投資額が高め

- 複雑なインストールと統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新たなビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 消費者感情分析

- 特許および知的財産分析

- 地政学と貿易のダイナミクス

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 市場集中分析

- 地域別

- 主要プレーヤーの競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- リーダーたち

- 課題者たち

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推定・予測:ファイバータイプ別、2021年~2034年

- 主要動向

- シングルモードファイバー

- マルチモードファイバー

第6章 市場推定・予測:技術タイプ別、2021年~2034年

- 主要動向

- 光時間領域反射率測定法(OTDR)

- 光周波数領域反射率測定法(OFDR)

第7章 市場推定・予測:動作原理別、2021年~2034年

- 主要動向

- レイリー散乱ベースDTS

- ラマン散乱ベースDTS

- ブリルアン散乱ベースDTS

第8章 市場推定・予測:アプリケーション別、2021年~2034年

- 主要動向

- 石油・ガス

- 電力ケーブル監視

- 火災検知

- プロセス・パイプライン監視

- 環境モニタリング

- 変圧器温度監視

- その他

第9章 市場推定・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- AOMS Technologies

- AP Sensing GmbH

- Bandweaver Technologies

- Fluves

- GESO GmbH &Co.

- Halliburton Company

- Inventec B.V.

- Micron Optics

- NKT Photonics A/S

- OFS Fitel, LLC

- Omicron Electronics

- Omnisens SA

- Optromix, Inc.

- Schlumberger Limited

- Silixa Ltd.

- Sumitomo Electric Industries, Ltd.

- Yokogawa Electric Corporation

目次

The Global Distributed Temperature Sensing Market was valued at USD 871.5 million in 2024 and is estimated to grow at a CAGR of 7.6% to reach USD 1.81 billion by 2034. The rising adoption of industrial IoT technologies is playing a key role in driving this market forward. With industries increasingly turning to digital systems for enhanced safety and operational efficiency, there is a growing need for temperature monitoring solutions that deliver accurate, real-time data. Distributed temperature sensing meets this demand by offering continuous temperature measurements over long distances. This allows early detection of anomalies, helping to prevent system failures and avoid potentially hazardous conditions.

The rapid increase in electricity consumption-fueled by growing data center infrastructure, urbanization, and rising electric vehicle usage-is pushing utilities and industrial operators to adopt smarter power grid solutions. DTS systems are vital to these developments, as they assist in managing thermal loads and improving grid reliability. These sensing systems are commonly deployed in challenging environments like underground and overhead power lines, distribution nodes, and substations. Their ability to detect overheating or stress in power cables makes them indispensable in modern energy infrastructure. As industries aim to mitigate risks and improve asset lifespan, the demand for DTS is steadily rising.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $871.5 Million |

| Forecast Value | $1.81 Billion |

| CAGR | 7.6% |

In terms of fiber type, single-mode fibers are expected to record significant growth, with their market value projected to reach USD 951 million by 2034. These fibers are favored for applications requiring high-speed data transfer over long distances. Their inherent ability to transmit data with minimal signal loss and higher bandwidth capacity makes them ideal for modern telecommunication and industrial setups. As network connectivity expands globally, especially with the development of next-generation broadband and wireless systems, the use of single-mode fiber in DTS applications continues to increase. These fibers enable distributed sensors to measure temperature variations accurately along extended cable lengths.

When analyzed by technology, the market is segmented into Optical Time Domain Reflectometry (OTDR) and Optical Frequency Domain Reflectometry (OFDR). OTDR remains the dominant technology, accounting for 72.5% of the global market in 2024. The method is widely accepted for its precision in detecting faults and verifying continuity in optical fiber networks. OTDR enables efficient maintenance by identifying exact fault points, splice losses, or fiber breaks, which is essential for sectors that rely on uninterrupted operations. DTS systems using OTDR analyze backscattered light to determine temperature profiles across a fiber's length, enhancing real-time monitoring capabilities.

By operating principle, the market is segmented into Rayleigh scattering-based, Raman scattering-based, and Brillouin scattering-based DTS systems. Among these, Rayleigh scattering-based DTS captured 24% of the market share in 2024. This technology is particularly suitable for environments that demand fine-grained temperature monitoring. Its capacity for detailed thermal analysis supports operations where early detection of temperature spikes is critical. Industries operating in high-risk zones are increasingly relying on such technologies to ensure consistent monitoring and issue resolution before major failures occur.

From an application standpoint, DTS systems are used across several industries, including power cable monitoring, fire detection, pipeline management, environmental assessments, and more. However, oil and gas applications held the largest share of 30.1% in 2024. These sectors require continuous temperature monitoring over long distances to ensure operational efficiency and safety. DTS solutions offer the necessary precision and reliability to support these needs, contributing to optimized performance and preventive maintenance.

In regional analysis, the United States stands out as a major market, with projections indicating it will reach USD 415 million by 2034. Within the country, DTS systems are widely deployed for real-time thermal monitoring of wellbores and electrical grids. With initiatives focused on modernizing aging infrastructure, the adoption of advanced temperature sensing solutions is gaining momentum. These systems support efficient load management and early detection of performance issues, reducing the risk of unplanned outages.

The market landscape is competitive, with key players including Schlumberger Limited, Halliburton Company, AP Sensing GmbH, Silixa Ltd., and Bandweaver Technologies collectively accounting for over 43.3% of global revenue. To maintain leadership and adapt to evolving industry demands, companies are investing heavily in next-generation fiber materials and sensor technologies that improve measurement accuracy and environmental durability. Compact and energy-efficient DTS systems with enhanced resolution are being introduced to meet the growing demand for real-time, high-precision monitoring.

AI-driven diagnostics and analytics are also being integrated into DTS solutions to support predictive maintenance and extend system reliability. Industry participants are responding to user needs by offering customized DTS configurations tailored for specific industrial challenges. In addition, strategic partnerships, acquisitions, and collaborations are becoming central to expanding technological capabilities and geographic reach. By engaging with regulatory bodies and utility operators, firms are also ensuring that their DTS offerings align with evolving environmental and safety standards.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.3 Fiber type

- 2.4 Technology type

- 2.5 Operating principle

- 2.6 Application

- 2.7 Regional

- 2.8 TAM Analysis, 2025-2034 (USD Billion)

- 2.9 CXO perspectives: Strategic imperatives

- 2.9.1 Executive decision points

- 2.9.2 Critical Success Factors

- 2.10 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for advanced pipeline monitoring

- 3.2.1.2 Growing need for fire detection and prevention systems

- 3.2.1.3 Rising investments in power grid infrastructure

- 3.2.1.4 Technological advancements in optical fiber sensing

- 3.2.1.5 Expansion of smart Infrastructure and Industrial IoT (IIoT)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital investment

- 3.2.2.2 Complex installation and integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Sustainability Measures

- 3.13 Consumer Sentiment Analysis

- 3.14 Patent and IP analysis

- 3.15 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic Presence Comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive Positioning Matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche Players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates & Forecast, By Fiber Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Single-mode fibers

- 5.3 Multimode fibers

Chapter 6 Market Estimates & Forecast, By Technology Type, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Optical Time Domain Reflectometry (OTDR)

- 6.3 Optical Frequency Domain Reflectometry (OFDR)

Chapter 7 Market Estimates & Forecast, By Operating Principle, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Rayleigh scattering-based DTS

- 7.3 Raman scattering-based DTS

- 7.4 Brillouin scattering-based DTS

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Oil & gas

- 8.3 Power cable monitoring

- 8.4 Fire detection

- 8.5 Process & pipeline monitoring

- 8.6 Environmental monitoring

- 8.7 Transformer temperature monitoring

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AOMS Technologies

- 10.2 AP Sensing GmbH

- 10.3 Bandweaver Technologies

- 10.4 Fluves

- 10.5 GESO GmbH & Co.

- 10.6 Halliburton Company

- 10.7 Inventec B.V.

- 10.8 Micron Optics

- 10.9 NKT Photonics A/S

- 10.10 OFS Fitel, LLC

- 10.11 Omicron Electronics

- 10.12 Omnisens SA

- 10.13 Optromix, Inc.

- 10.14 Schlumberger Limited

- 10.15 Silixa Ltd.

- 10.16 Sumitomo Electric Industries, Ltd.

- 10.17 Yokogawa Electric Corporation

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日