中電圧ドライブの市場機会と促進要因、産業動向分析、2025年~2034年予測

Medium Voltage Drives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755401

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

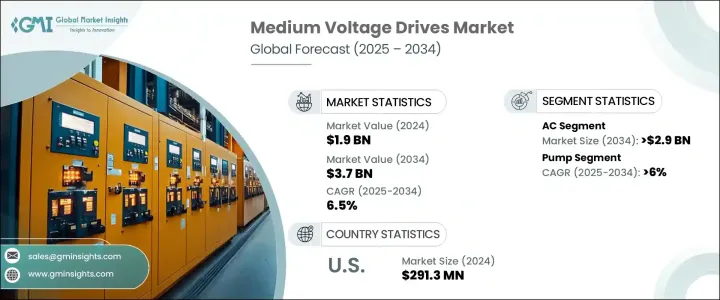

中電圧ドライブの世界市場規模は、2024年に19億米ドルとなり、CAGR 6.5%で成長し、2034年には37億米ドルに達すると予測されています。

この産業の成長は、高効率エネルギーソリューションに対する産業需要の増加と、洗練されたモーター制御システムの必要性による影響が大きいです。これらのドライブは、速度とトルクを調整することでモータ性能を最適化する上で重要な役割を果たし、大幅なエネルギー節約、運用コストの削減、排出量の削減につながります。持続可能性と費用対効果への注目の高まりは、さまざまな産業でこれらのシステムの普及を促しています。

大型機械とエネルギーの最適化を必要とするセグメントへの資本流入の増加が、市場の将来を形成しています。中電圧ドライブは、大規模な機械システムを伴うさまざまな業務に不可欠なコンポーネントとなりつつあります。特に大規模なHVACネットワークや自動化システムを組み込んだ新しい産業インフラの開発は、市場加速のための強固な基盤となっています。さらに、製造業と公益事業における自動化とスマート技術への注目の高まりが、需要をさらに押し上げています。企業が生産の合理化と効率の向上を目指す中、中電圧ドライブ技術の採用は戦略的な優先事項となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 19億米ドル |

| 予測金額 | 37億米ドル |

| CAGR | 6.5% |

AC中電圧ドライブセグメントが市場を独占し、2034年には29億米ドルを超えると予測されます。このセグメントは、新たなデジタル技術との互換性により顕著な成長を遂げています。インテリジェントシステムとリアルタイム分析の統合により、ACドライブは最新の産業用途にとってますます魅力的なものとなっています。スマート機能を組み込むことで、システムの応答性向上、予知保全、運用の柔軟性が可能になり、これらは今日の急速に進化する産業環境において非常に重要です。デジタルトランスフォーメーション、特に自動化された製造業への関心の高まりは、ACベースのシステムに対する需要を強化しています。

中電圧ドライブ市場は用途別に、ポンプ、ファン、コンベア、コンプレッサ、押出機、その他に区分されます。このうち、ポンプ用途は最大の市場シェアを確保する展望で、2034年のCAGRは6%以上で拡大すると予測されています。ポンプ用途で使用されるドライブは、システム出力と運転効率の向上に大きく貢献します。強化された制御機構によって正確な速度調節が可能になり、性能の向上とエネルギー使用量の削減につながります。また、摩耗や損傷を最小限に抑え、メンテナンスの必要性を低減することで、システムの長寿命化にも貢献します。ポンプ運転における中電圧ドライブの採用は、多様な産業セグメントでの汎用性と性能上の利点により、支持を集めています。

米国では、中電圧ドライブ市場は引き続き大きな勢いを見せています。2022年の市場規模は2億6,200万米ドル、2023年には2億7,610万米ドル、2024年には2億9,130万米ドルと評価されています。インフラの近代化とエネルギー効率の向上を目指した継続的な投資が、この上昇傾向に極めて重要な役割を果たしています。さらに、信頼性の高いモーター制御ソリューションに対するニーズや、エネルギー効率の高い技術の採用を求める規制機関の後押しが強まっていることも、需要を支えています。技術的なアップグレードや、省エネルギーを対象とした連邦政府のインセンティブも、さまざまなセクタの購買決定やシステムアップグレードに影響を与えています。

中電圧ドライブ市場の大手メーカーは、一貫した技術革新と強固な世界事業によって競合を維持しています。産業環境に合わせた統合パワーシステムとエネルギーソリューションの提供における専門知識により、これらの企業は重要な参入企業として位置づけられています。これらの企業は、自動化プロセスやスマート製造環境に適合する高度でカスタマイズ型ドライブシステムを提供することで、進化する顧客要件に適応し続けています。

OEM、ユーティリティ企業、産業用エンドユーザーとの戦略的提携やパートナーシップは、市場参入企業にとって不可欠なものとなっています。技術的な強化に重点を置き、最新のオートメーション動向に合わせた製品を提供することで、メーカーは市場の需要により効率的に対応しています。また、サプライチェーン全体の利害関係者と密接に協力することで、製品の供給範囲を拡大し、製品の可用性を高めています。的を絞ったR&D投資を通じて、エネルギー性能とデジタル産業エコシステムへのシームレスな統合に対する高まる期待に応える次世代ドライブを提供しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- 規制情勢

- 産業への影響要因

- 促進要因

- 産業の潜在的リスク・課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的取り組み

- 競合ベンチマーキング

- 戦略的ダッシュボード

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:出力範囲別、2021~2034年

- 主要動向

- 1MW以下

- 1MW~3MW

- 3MW~7MW

- 7MW以上

第6章 市場規模・予測:ドライブ別, 2021~2034年

- 主要動向

- AC

- DC

- サーボ

第7章 市場規模・予測:流通チャネル別、2021~2034年

- 主要動向

- 最終用途への直接供給

- 機械メーカーに直接

- システムインテグレーターに直接

- 販売代理店/パートナー

第8章 市場規模・予測:用途別、2021~2034年

- 主要動向

- ポンプ

- ファン

- クレーンとホイスト

- コンベア

- コンプレッサー

- 押出機

- その他

第9章 市場規模・予測:最終用途別、2021~2034年

- 主要動向

- 石油・ガス

- 発電

- 鉱業・金属

- パルプと紙

- 海洋

- その他

第10章 市場規模・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- タイ

- シンガポール

- マレーシア

- ベトナム

- インドネシア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第11章 企業プロファイル

- ABB

- CG Power & Industrial Solutions

- Danfoss

- Delta Electronics

- Eaton

- Fuji Electric

- General Electric

- Hitachi Hi-Rel Power Electronics

- Ingeteam Power Technology

- Johnson Controls

- Nidec Industrial Solutions

- Rockwell Automation

- Schneider Electric

- Siemens

- TECO-Westinghouse

- TMEIC

- WEG

- Yaskawa Electric

目次

The Global Medium Voltage Drives Market was valued at USD 1.9 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 3.7 billion by 2034. Growth in the industry is largely influenced by increasing industrial demand for high-efficiency energy solutions and the need for sophisticated motor control systems. These drives play a crucial role in optimizing motor performance by adjusting speed and torque, leading to considerable energy savings, reduced operational expenses, and lower emissions. This growing focus on sustainability and cost-effectiveness is encouraging more widespread deployment of these systems across different industries.

Rising capital inflow into sectors that require heavy-duty machinery and energy optimization is shaping the future of the market. Medium voltage drives are becoming essential components in various operations involving large-scale mechanical systems. The development of new industrial infrastructure, particularly those incorporating large HVAC networks and automated systems, is providing a solid foundation for market acceleration. Additionally, the increased focus on automation and smart technologies in manufacturing and utilities is further propelling demand. As companies aim to streamline production and boost efficiency, the adoption of medium voltage drive technologies is becoming a strategic priority.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $3.7 Billion |

| CAGR | 6.5% |

The AC medium voltage drive segment is expected to dominate the market landscape and is forecasted to exceed USD 2.9 billion by 2034. This segment is experiencing notable growth due to its compatibility with emerging digital technologies. The integration of intelligent systems and real-time analytics is making AC drives increasingly attractive for modern industrial applications. The incorporation of smart features allows for better system responsiveness, predictive maintenance, and operational flexibility, which are critical in today's fast-evolving industrial environments. Growing interest in digital transformation, especially in automated manufacturing, is reinforcing the demand for AC-based systems.

By application, the medium voltage drives market is segmented into pump, fan, conveyor, compressor, extruder, and others. Among these, the pump application is poised to secure the largest market share and is projected to expand at a CAGR of over 6% through 2034. Drives used in pump applications contribute significantly to improving system output and operational efficiency. Enhanced control mechanisms allow precise speed regulation, leading to better performance and reduced energy use. This capability also supports system longevity by minimizing wear and tear and lowering maintenance requirements. The adoption of medium voltage drives in pump operations is gaining traction due to their versatility and performance benefits across diverse industrial sectors.

In the United States, the medium voltage drives market continues to witness strong momentum. The market was assessed at USD 262 million in 2022, followed by USD 276.1 million in 2023 and USD 291.3 million in 2024. Ongoing investments aimed at modernizing infrastructure and enhancing energy efficiency are playing a pivotal role in this upward trend. Demand is further supported by the need for reliable motor control solutions and an increasing push from regulatory bodies for the adoption of energy-efficient technologies. Technological upgrades and federal incentives targeting energy conservation are also making an impact on purchasing decisions and system upgrades in various sectors.

Leading manufacturers in the medium voltage drive market maintain their competitive edge through consistent innovation and robust global operations. Their expertise in delivering integrated power systems and energy solutions tailored for industrial settings positions them as key players. These companies continue to adapt to evolving customer requirements by offering advanced and customized drive systems that are compatible with automated processes and smart manufacturing environments.

Strategic collaborations and partnerships with OEMs, utilities, and industrial end-users are becoming essential for market players. By focusing on technological enhancements and aligning their offerings with modern automation trends, manufacturers are addressing market demands more efficiently. They are also expanding their reach and improving product availability by working closely with stakeholders across the supply chain. Through targeted R&D investments, they are delivering next-generation drives that meet the rising expectations for energy performance and seamless integration into digital industrial ecosystems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic initiative

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Range, 2021 - 2034, (USD Million, Units)

- 5.1 Key trends

- 5.2 ≤ 1 MW

- 5.3 1 MW - 3 MW

- 5.4 3 MW - 7 MW

- 5.5 > 7 MW

Chapter 6 Market Size and Forecast, By Drive, 2021 - 2034, (USD Million, Units)

- 6.1 Key trends

- 6.2 AC

- 6.3 DC

- 6.4 Servo

Chapter 7 Market Size and Forecast, By Sales Channel, 2021 - 2034, (USD Million, Units)

- 7.1 Key trends

- 7.2 Direct to end use

- 7.3 Direct to machine builder

- 7.4 Direct to systems integrator

- 7.5 Distribution/partner

Chapter 8 Market Size and Forecast, By Application, 2021 - 2034, (USD Million, Units)

- 8.1 Key trends

- 8.2 Pump

- 8.3 Fan

- 8.4 Cranes & hoists

- 8.5 Conveyor

- 8.6 Compressor

- 8.7 Extruder

- 8.8 Others

Chapter 9 Market Size and Forecast, By End use, 2021 - 2034, (USD Million, Units)

- 9.1 Key trends

- 9.2 Oil & gas

- 9.3 Power generation

- 9.4 Mining & metals

- 9.5 Pulp and paper

- 9.6 Marine

- 9.7 Others

Chapter 10 Market Size and Forecast, By Region, 2021 - 2034, (USD Million, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Thailand

- 10.4.7 Singapore

- 10.4.8 Malaysia

- 10.4.9 Vietnam

- 10.4.10 Indonesia

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 South Africa

- 10.5.4 Egypt

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 CG Power & Industrial Solutions

- 11.3 Danfoss

- 11.4 Delta Electronics

- 11.5 Eaton

- 11.6 Fuji Electric

- 11.7 General Electric

- 11.8 Hitachi Hi-Rel Power Electronics

- 11.9 Ingeteam Power Technology

- 11.10 Johnson Controls

- 11.11 Nidec Industrial Solutions

- 11.12 Rockwell Automation

- 11.13 Schneider Electric

- 11.14 Siemens

- 11.15 TECO-Westinghouse

- 11.16 TMEIC

- 11.17 WEG

- 11.18 Yaskawa Electric

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日