|

市場調査レポート

商品コード

1755399

乳房インプラント市場機会と促進要因、業界動向分析、2025年~2034年予測Breast Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 乳房インプラント市場機会と促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年05月19日

発行: Global Market Insights Inc.

ページ情報: 英文 145 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

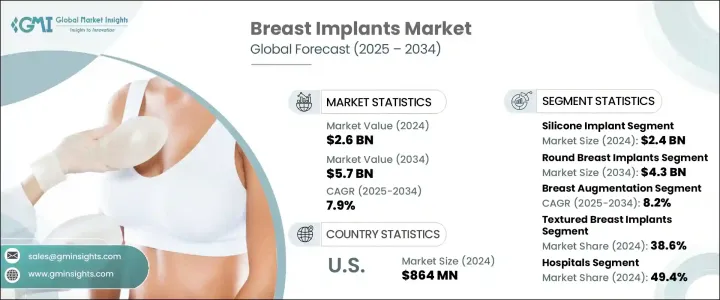

世界の乳房インプラント市場は、2024年に26億米ドルと評価され、豊胸手術の増加、インプラントデザインの技術革新、外見への注目の高まりによって、CAGR 7.9%で成長し、2034年には57億米ドルに達すると推定されています。

豊胸手術は、その高い満足度、個人に合わせた仕上がり、比較的安全で低侵襲な手術のため、特に先進地域で広く求められる美容術となっています。回復時間の短縮や合併症リスクの軽減など、手術手技の進歩もこの手術の魅力に貢献しています。

加えて、特に美的感覚や自信に焦点を当てた、体を美しくする手術が社会的に受け入れられつつあることも、乳房インプラントの人気の高まりに貢献しています。女性は、美容的な理由だけでなく、非対称性や、乳房切除やその他の病状の後の乳房再建の必要性といった機能的な問題にも対処するために、豊胸術を選択することが増えています。乳房インプラントが、すべての人の体型や美的目標に合わせてカスタマイズ型ソリューションを提供できることが、需要を大きく後押ししています。さらに、低侵襲法を含む手術技術の進歩により、これらの手術はより安全で効果的なものとなり、回復時間も短縮され、合併症のリスクも減少しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 26億米ドル |

| 予測金額 | 57億米ドル |

| CAGR | 7.9% |

シリコンインプラントセグメントは、2024年に24億米ドルを生み出しました。特に乳房切除後の豊胸と再建のためのシリコーンインプラントへの嗜好が高まっているのは、その自然な外観と感触、耐久性によるところが大きいです。シリコーンインプラントは、しわや波紋ができにくく、より滑らかで自然な美しさを提供するため、形成外科医に非常に支持されています。これらのインプラントは、米国食品医薬品局(FDA)と欧州医薬品庁(EMA)の両方から、増大術と再建術の両方に認可されています。インプラントのサイズやプロファイルの多様化もその人気の一因となっており、幅広い患者に適しています。さらに、シリコンインプラントは再手術に使用されることが増えており、市場の成長をさらに後押ししています。

ラウンド型乳房インプラントセグメントは2024年にかなりのシェアを占め、2034年には43億米ドルに成長すると予想されています。ラウンド型インプラントは、よりリフトアップされた丸みを帯びた外観を提供できることと、設置の柔軟性から特に人気があります。丸型インプラントは、脇の下の切開を含むあらゆるタイプの切開から挿入できるため、傷跡が目立ちにくく、多くの患者に好まれています。さらに、ラウンド型インプラントは、費用対効果、手術のしやすさ、サイズの選択肢の広さによる柔軟性を提供し、使用量の増加に寄与しています。このセグメントの成長は、生理食塩水とシリコンの両方のバージョンを含む多様なオプションの利用可能性と、改良されたインプラント技術の継続的な開発によって強化されると予想されます。

米国の乳房インプラント 2024年の市場規模は8億6,400万米ドルで、豊胸手術の増加とヘルスケア施設の進歩が市場成長を牽引しています。大手企業の存在と先進的なインプラント新製品の開発が市場拡大を支えています。美容整形が受け入れられつつあることに加え、乳房インプラントの価格が手ごろになったことで、より幅広い層が利用しやすくなり、採用率が高まっています。

世界の乳房インプラント産業の主要企業には、AbbVie、Euromi、Guangzhou Wanhe Plastic Material、Sientra、POLYTECH Health & Aesthetics、Mentor Worldwide LLCなどがあります。これらの企業は、製品の技術革新と戦略的パートナーシップや提携による市場拡大に注力しています。また、インプラントの品質を向上させ、患者の満足度を高め、手術リスクを軽減するための研究開発への投資も活発化しています。さらに、これらの企業の多くは、多様な患者のニーズに応えるため、より幅広いインプラントのサイズ、形態、材料の開発に積極的に取り組んでおり、市場における競合の強化に貢献しています。さらに、より先進的製造プロセスを採用することで、これらの企業はよりカスタマイズ型高品質のインプラントを提供できるようになり、市場シェアをさらに押し上げています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- 産業への影響要因

- 促進要因

- 豊胸手術件数の増加

- 乳がん発症率の増加

- 技術的進歩

- 形成外科医の増加

- 産業の潜在的リスク・課題

- インプラント手術の高額な費用

- 合併症のリスク

- 促進要因

- 成長可能性分析

- 規制情勢

- 米国

- 欧州

- 技術

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 産業への影響

- 供給側の影響(原料)

- 主要原料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原料)

- 影響を受ける主要企業

- 戦略的な産業対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 施策関与

- 展望と今後の検討事項

- 貿易への影響

- 償還シナリオ

- 価格分析

- ポーター分析

- PESTEL分析

- 将来の市場動向

- GAP分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推定・予測:製品別、2021~2034年

- 主要動向

- 生理食塩水インプラント

- シリコンインプラント

第6章 市場推定・予測:形態別、2021~2034年

- 主要動向

- ラウンド

- アナトミカル

第7章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 豊胸手術

- 乳房再建

第8章 市場推定・予測:インプラントテクスチャ別、2021~2034年

- 主要動向

- スムーズ

- テクスチャあり

第9章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 病院

- クリニック

- その他

第10章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- スウェーデン

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- タイ

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- チリ

- ペルー

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- イスラエル

- トルコ

第11章 企業プロファイル

- AbbVie

- Establishment Labs

- Euromi

- GC Aesthetics

- Groupe Sebbin

- Guangzhou Wanhe Plastic Material

- Hansbiomed

- IDEAL Implant

- Laboratoires Arion

- Mentor Worldwide LLC(Johnson & Johnson)

- POLYTECH Health & Aesthetics

- Prayasta 3D Inventions

- Shanghai Kangning Medical Device

- Sientra

The Global Breast Implants Market was valued at USD 2.6 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 5.7 billion by 2034, driven by the rise in breast augmentation surgeries, technological innovations in implant designs, and an increasing focus on physical appearance. Breast augmentation has become a widely sought-after cosmetic procedure, particularly in developed regions, due to its high satisfaction rate, personalized results, and relatively safe, minimally invasive procedures. Advances in surgical techniques, including quicker recovery times and reduced complication risks, have also contributed to the procedure's appeal.

Additionally, the increasing societal acceptance of body-enhancing procedures, particularly those focused on aesthetics and self-confidence, has contributed to the growing popularity of breast implants. Women are increasingly opting for breast augmentation not just for cosmetic reasons but also to address functional issues like asymmetry and the need for breast reconstruction following mastectomies or other medical conditions. The ability of breast implants to offer customized solutions tailored to everyone's body shape and aesthetic goals has significantly driven demand. Moreover, advances in surgical techniques, including minimally invasive methods, have made these procedures safer and more effective, with faster recovery times and reduced risk of complications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 Billion |

| Forecast Value | $5.7 Billion |

| CAGR | 7.9% |

The silicone implant segment generated USD 2.4 billion in 2024. The increasing preference for silicone implants for breast augmentation and reconstruction, especially after mastectomy, is largely due to their natural look and feel, as well as their durability. Silicone implants are highly favored by plastic surgeons because they are less prone to wrinkles or rippling and provide a smoother, more natural aesthetic. These implants are approved by both the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) for both augmentation and reconstruction procedures. The growing variety of implant sizes and profiles has also contributed to their popularity, making them suitable for a broad range of patients. Moreover, silicone implants are increasingly used for revision surgeries, further supporting market growth.

The round breast implants segment accounted for a substantial share in 2024 and is expected to grow to USD 4.3 billion by 2034. Round implants are particularly popular due to their ability to provide a more lifted, rounder appearance and flexibility in placement. They can be inserted through any type of incision, including underarm incisions, which reduces visible scarring, making them a preferred choice for many patients. Furthermore, round implants offer flexibility based on cost-effectiveness, surgical ease, and a wider range of size options, contributing to their increasing usage. The growth of this segment is expected to be bolstered by the availability of diverse options, including both saline and silicone versions, and the continued development of improved implant technologies.

United States Breast Implants Market generated USD 864 million in 2024, with an increase in breast augmentation procedures and advancements in healthcare facilities driving market growth. The presence of major players and the development of new, advanced implant products support this market expansion. The growing acceptance of aesthetic surgery, as well as the increasing affordability of breast implants, has made them more accessible to a broader demographic, resulting in higher adoption rates.

Key players in the Global Breast Implants Industry include AbbVie, Euromi, Guangzhou Wanhe Plastic Material, Sientra, POLYTECH Health & Aesthetics, and Mentor Worldwide LLC, among others. These companies focus on product innovation and expanding their market reach through strategic partnerships and collaborations. They are also increasingly investing in research and development to improve implant quality, enhance patient satisfaction, and reduce surgical risks. Furthermore, many of these companies are actively working to develop a wider range of implant sizes, shapes, and materials to cater to diverse patient needs, which helps strengthen their competitive position in the market. Additionally, adopting more advanced manufacturing processes has enabled these companies to offer more customized, higher-quality implants, further boosting their market share.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.1.3 Base year calculation

- 1.1.4 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.1.5 Primary sources

- 1.1.6 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of breast augmentation procedures

- 3.2.1.2 Growing breast cancer incidence

- 3.2.1.3 Technological advancements

- 3.2.1.4 Increasing number of plastic surgeons

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of implantation procedure

- 3.2.2.2 Risk of complications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technological landscape

- 3.6 Trump administration tariffs

- 3.6.1 Impact on trade

- 3.6.1.1 Trade volume disruptions

- 3.6.1.2 Retaliatory measures

- 3.6.2 Impact on the Industry

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.2.1.1 Price volatility in key materials

- 3.6.2.1.2 Supply chain restructuring

- 3.6.2.1.3 Production cost implications

- 3.6.2.2 Demand-side impact (selling price)

- 3.6.2.2.1 Price transmission to end markets

- 3.6.2.2.2 Market share dynamics

- 3.6.2.2.3 Consumer response patterns

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.3 Key companies impacted

- 3.6.4 Strategic industry responses

- 3.6.4.1 Supply chain reconfiguration

- 3.6.4.2 Pricing and product strategies

- 3.6.4.3 Policy engagement

- 3.6.5 Outlook and future considerations

- 3.6.1 Impact on trade

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

- 3.12 GAP analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Saline implant

- 5.3 Silicone implant

Chapter 6 Market Estimates and Forecast, By Shape, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Round

- 6.3 Anatomical

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Breast augmentation

- 7.3 Breast reconstruction

Chapter 8 Market Estimates and Forecast, By Implant Texture, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Smooth

- 8.3 Textured

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Clinics

- 9.4 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Sweden

- 10.3.7 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Columbia

- 10.5.5 Chile

- 10.5.6 Peru

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

- 10.6.5 Turkey

Chapter 11 Company Profiles

- 11.1 AbbVie

- 11.2 Establishment Labs

- 11.3 Euromi

- 11.4 GC Aesthetics

- 11.5 Groupe Sebbin

- 11.6 Guangzhou Wanhe Plastic Material

- 11.7 Hansbiomed

- 11.8 IDEAL Implant

- 11.9 Laboratoires Arion

- 11.10 Mentor Worldwide LLC (Johnson & Johnson)

- 11.11 POLYTECH Health & Aesthetics

- 11.12 Prayasta 3D Inventions

- 11.13 Shanghai Kangning Medical Device

- 11.14 Sientra