固定式太陽光発電取付システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Fixed Solar PV Mounting Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755376

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

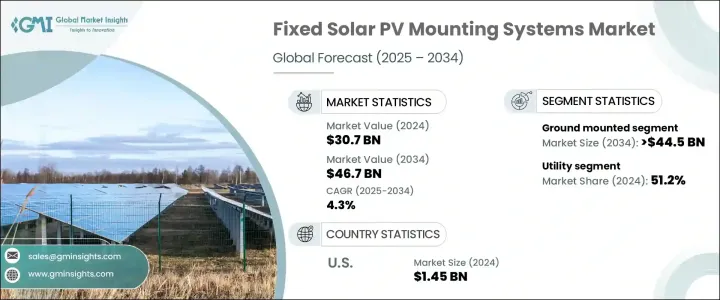

世界の固定式太陽光発電取付システム市場は、2024年に307億米ドルと評価され、再生可能エネルギーへの世界のシフトとともに、ソーラーパネルと関連部品のコスト低下により、CAGR 4.3%で成長し、2034年には467億米ドルに達すると予測されています。

開発途上国では、州レベルの政策やインセンティブ、固定価格買取制度(FiT)に支えられて太陽光発電モジュールの導入が進んでおり、架台システムの需要も増加するとみられます。太陽光発電設備からより高いエネルギー収率を得る必要性が、これらのシステムの需要をさらに押し上げています。ソーラートラッカーは、エネルギー発電量を増加させる能力があり、より複雑な追尾システムと比べて比較的安価であることから人気を博しています。さらに、設計がシンプルで可動部品がないため、市場の拡大に大きく貢献しています。

関税引き上げによる太陽電池モジュールのコスト上昇などの課題にもかかわらず、市場全体の見通しは依然として明るいです。関税の引き上げが公共施設規模のプロジェクトのコスト上昇につながり、太陽光発電取付システムの費用が約30%上昇したが、地上設置型太陽光発電プロジェクトにおける架台システムの採用は拡大を続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 307億米ドル |

| 予測金額 | 467億米ドル |

| CAGR | 4.3% |

地上設置型太陽光発電取付システム分野は、再生可能エネルギー需要の増加と大規模太陽光発電設備の必要性により、2034年までに445億米ドルに達すると予測されます。地上設置型システムには、設置の容易さや費用対効果など、いくつかの利点があり、特に広大で安価な土地面積を持つ地域ではそれが顕著です。これらのシステムの手頃な価格と拡張性は、設置コストを最小限に抑えながらエネルギー出力を最大化することが重要な、公益事業規模の太陽光発電プロジェクトにとって特に魅力的です。設置システムの設計、材料、設置技術における技術の進歩は、これらのシステムの総コストを大幅に引き下げ、財政的な実現可能性をさらに高めています。

再生可能エネルギー目標を達成し、エネルギー生産量を増加させるため、大規模太陽光発電プロジェクトへの依存度が高まっていることを反映して、2024年には公益事業セグメントが51.2%を占める。地上設置型太陽光発電取付システムは、追尾型システムよりも導入が簡単で安価であるため、公益事業規模での設置に広く支持されています。政府の優遇措置や規制と政策など、金融・政策面の進化は、太陽光発電における地上設置型ソリューションの魅力を高め続けています。

米国の固定式太陽光発電取付システム好ましい政治的規制、財政的インセンティブ、急速な技術進歩に牽引され、2024年の産業規模は14億5,000万米ドルと評価されました。こうした要因によって、特に公益事業規模での太陽光発電取付システムの導入が加速しています。再生可能エネルギー生産への需要が高まり続けるなか、効率的なソーラー架台システムの導入が拡大し、この地域がより持続可能でクリーンなエネルギー源へとシフトしていくことに貢献すると予想されます。

世界の固定式太陽光発電取付システム業界には、Aerocompact, Arctech, Clenergy, Convert Italia SPA, Esdec, K2 Systems GmbH, Mounting Systems, Schletter Group, UNIRAC, Versolsolar Hangzhou Co., Ltd., Xiamen Grace Solar New Energy Technology Co., Ltd.などの主要企業が含まれています。固定式太陽光発電取付システム業界の企業は、いくつかの戦略的イニシアチブを実施しています。エネルギー効率の高いソリューションに対する需要の高まりに対応するため、設計や技術の革新を優先しています。多くの企業が研究開発に投資し、耐久性や設置の容易さなど、製品の性能を高めています。さらに、主要プレーヤーは、住宅用と商業用に製品ポートフォリオを拡大し、多様な顧客ニーズを満たす幅広いシステムを提供できるようにしています。また、太陽電池モジュールメーカーや建設会社との戦略的提携も増加しており、これによって各社は業務を効率化し、市場範囲を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア

- 戦略的取り組み

- 企業ベンチマーク

- 戦略的ダッシュボード

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- 地上設置型

- 屋上

第6章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅用

- 商業および工業

- ユーティリティ

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- オーストリア

- ノルウェー

- デンマーク

- フィンランド

- フランス

- ドイツ

- イタリア

- スイス

- スペイン

- スウェーデン

- 英国

- アジア太平洋

- 中国

- オーストラリア

- 韓国

- 日本

- インド

- 中東

- イスラエル

- サウジアラビア

- アラブ首長国連邦

- ヨルダン

- オマーン

- アフリカ

- 南アフリカ

- イスラエル

- モロッコ

- ラテンアメリカ

- ブラジル

- チリ

- アルゼンチン

第8章 企業プロファイル

- Aerocompact

- Arctech

- Clenergy

- Convert Italia SPA

- Esdec

- K2 Systems GmbH

- Mounting Systems

- Schletter Group

- UNIRAC

- Versolsolar Hangzhou Co., Ltd.

- Xiamen Grace Solar New Energy Technology Co., Ltd.

目次

The Global Fixed Solar PV Mounting Systems Market was valued at USD 30.7 billion in 2024 and is estimated to grow at a CAGR of 4.3% to reach USD 46.7 billion by 2034, driven by the decreasing costs of solar panels and related components, along with the global shift toward renewable energy sources. As developing nations increase their adoption of solar PV modules, supported by state-level policies, incentives, and feed-in tariffs (FiTs), the demand for mounting systems is also set to rise. The need for higher energy yields from solar installations further boosts the demand for these systems. Solar trackers have gained popularity due to their ability to increase energy generation and their relatively lower cost compared to more complex tracking systems. Additionally, with their simpler design and lack of moving parts, they have contributed significantly to the market's expansion.

Despite challenges such as tariffs that have increased the cost of solar modules, the overall market outlook remains positive. While tariff increases have led to higher costs for utility-scale projects, driving up the expense of solar systems by roughly 30%, the adoption of mounting systems in ground-mounted solar projects continues to grow.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $30.7 Billion |

| Forecast Value | $46.7 Billion |

| CAGR | 4.3% |

The ground-mounted solar systems segment is anticipated to reach USD 44.5 billion by 2034, driven by increasing demand for renewable energy and the need for large-scale solar installations. Ground-mounted systems offer several advantages, including ease of installation and cost-effectiveness, especially in regions with large, inexpensive land areas. The affordability and scalability of these systems make them particularly attractive for utility-scale solar projects, where maximizing energy output while minimizing installation costs is critical. Technological advancements in mounting system design, materials, and installation techniques have significantly lowered the overall cost of these systems, further boosting their financial viability.

The utility segment accounted for 51.2% in 2024, reflecting the growing reliance on large-scale solar power projects to meet renewable energy targets and increase energy production. Ground-mounted solar systems, simpler and more affordable to deploy than tracking systems, are widely favored for utility-scale installations. The evolving financial and policy landscape, including government incentives and supportive regulations, continues to enhance the attractiveness of ground-mounted solutions in solar energy generation.

United States Fixed Solar PV Mounting Systems Industry was valued at USD 1.45 billion in 2024 driven by favorable political regulations, financial incentives, and rapid technological advancements. These factors are accelerating the adoption of solar PV systems, particularly for utility-scale projects. As the demand for renewable energy production continues to rise, deploying efficient solar mounting systems is expected to grow, contributing to the region's shift toward more sustainable and cleaner energy sources.

The Global Fixed Solar PV Mounting Systems Industry includes key players such as Aerocompact, Arctech, Clenergy, Convert Italia SPA, Esdec, K2 Systems GmbH, Mounting Systems, Schletter Group, UNIRAC, Versolsolar Hangzhou Co., Ltd., Xiamen Grace Solar New Energy Technology Co., Ltd. Companies in the fixed solar PV mounting systems industry implement several strategic initiatives. They prioritize innovation in design and technology to meet the growing demand for energy-efficient solutions. Many are investing in R&D to enhance product performance, including durability and ease of installation. Additionally, key players are expanding their product portfolios to cater to residential and commercial segments, ensuring they offer a range of systems that meet diverse customer needs. Strategic partnerships with solar module manufacturers and construction firms are also rising, enabling companies to streamline operations and expand market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic initiatives

- 4.4 Company benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2021 – 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Ground mounted

- 5.3 Rooftop

Chapter 6 Market Size and Forecast, By End Use, 2021 – 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial & Industrial

- 6.4 Utility

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Austria

- 7.3.2 Norway

- 7.3.3 Denmark

- 7.3.4 Finland

- 7.3.5 France

- 7.3.6 Germany

- 7.3.7 Italy

- 7.3.8 Switzerland

- 7.3.9 Spain

- 7.3.10 Sweden

- 7.3.11 UK

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 South Korea

- 7.4.4 Japan

- 7.4.5 India

- 7.5 Middle East

- 7.5.1 Israel

- 7.5.2 Saudi Arabia

- 7.5.3 UAE

- 7.5.4 Jordan

- 7.5.5 Oman

- 7.6 Africa

- 7.6.1 South Africa

- 7.6.2 Israel

- 7.6.3 Morocco

- 7.7 Latin America

- 7.7.1 Brazil

- 7.7.2 Chile

- 7.7.3 Argentina

Chapter 8 Company Profiles

- 8.1 Aerocompact

- 8.2 Arctech

- 8.3 Clenergy

- 8.4 Convert Italia SPA

- 8.5 Esdec

- 8.6 K2 Systems GmbH

- 8.7 Mounting Systems

- 8.8 Schletter Group

- 8.9 UNIRAC

- 8.10 Versolsolar Hangzhou Co., Ltd.

- 8.11 Xiamen Grace Solar New Energy Technology Co., Ltd.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日