人工股関節置換術の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Hip Replacement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755375

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

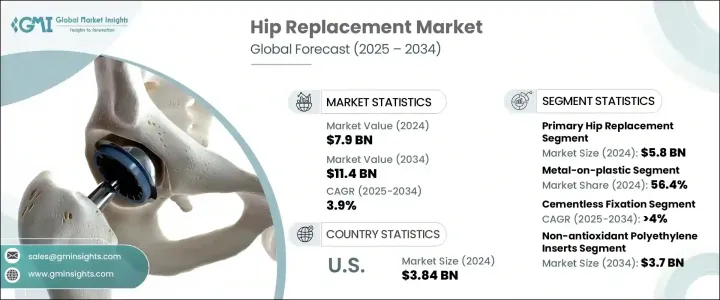

世界の人工股関節置換術市場は、2024年には79億米ドルとなり、CAGR 3.9%で成長し、2034年には114億米ドルに達すると推定されています。

同市場は、技術革新、手術件数の増加、関節関連疾患の罹患率の上昇などが相まって成長を遂げています。高齢者人口の増加、特に退行性関節疾患に罹患している人々は、人工股関節置換術の手術を受ける主要な人口層であり続けています。さらに、ロボット工学と低侵襲手術法の統合により、臨床成績が大幅に向上しています。これらの進歩は、入院期間の短縮、回復期間の短縮、患者満足度の向上につながり、最終的に人工股関節置換術手術の世界の採用率の向上に寄与しています。

関節の機能低下が進行している高齢者の間では、インプラント手術がますます一般的になっています。これらの手術は、手術手技や材料の開発により、今日ではより成功し、広く受け入れられています。さらに、ヘルスケア・インフラの改善や治療結果に関する患者教育の充実が、市場の拡大を支えています。外傷症例や整形外科的損傷の増加、有利な医療費償還も、人工股関節置換術手術の頻度を押し上げています。インプラントの設計、互換性、耐久性における革新は、整形外科医が効果的で患者に特化したソリューションを提供することを可能にしています。市場は、活動的な高齢者層におけるモビリティ向上ソリューションと長期的性能に対する需要の高まりとともに進化を続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 79億米ドル |

| 予測金額 | 114億米ドル |

| CAGR | 3.9% |

製品セグメンテーションでは、主要な人工股関節置換術デバイスが2024年の世界市場を席巻し、58億米ドルを記録しました。これらの器具は、さまざまな外科手術に幅広く適用されるため、依然として最も一般的に使用されているインプラントです。これらの器具が広く使用されているのは、複数の股関節疾患への適合性と、信頼性の高い長期的な結果をもたらす能力に起因しています。骨折や加齢に伴う関節の摩耗などの要因により、股関節インプラント手術の件数が増加していることが、この製品カテゴリーの継続的な成長を確実なものにしています。

材料の種類別では、メタル・オン・プラスティック・インプラントが2024年のシェア56.4%で市場をリードしています。この材料の組み合わせは、優れた耐摩耗性、手頃な価格、機械的安定性により、依然として好ましい選択肢となっています。金属製コンポーネントは圧力を効果的に吸収し、プラスチック製ライナーは関節の摩擦を軽減するため、可動性が向上し、時間の経過とともに摩耗が減少します。これらのインプラントは、その有効性、外科医へのなじみの深さ、再置換率の低さにより、世界中で一般的に使用されており、ヘルスケアの専門家にとっても患者にとっても頼りになる選択肢となっています。

固定方法別に分析すると、セメントレス固定システムは2024年に主要カテゴリーに浮上し、2034年までのCAGRは4%と予測されています。この分野は、長期的な生物学的安定性により支持を集めています。合成接着剤に頼るセメント固定とは異なり、セメントレスインプラントはインプラント表面周囲の自然な骨の成長を促進します。このような生物学的統合により、インプラントの寿命が延び、時間の経過とともにインプラントがゆるむ可能性が低くなります。特に若い患者は、長期間にわたって成功率が高いため、この固定法の恩恵を受けることができます。表面設計や材料コーティングの改善により、特に低侵襲手術や外来手術の場面で、この方法の需要がさらに高まっています。

市場セグメンテーション分野もまた、顕著な動向を見せています。非酸化性ポリエチレン製インサートが注目を集めており、2034年までに37億米ドルに達すると予測されています。これらのインサートは酸化摩耗を低減することが知られており、インプラントの長寿命化に役立っています。これらの用途の拡大は、信頼性の高い臨床性能、幅広い入手可能性、簡素化された製造工程によって支えられています。ヘルスケア専門家は、一貫した処置の成功と長期的な有効性を裏付ける強力な過去のデータにより、これらのインサートを支持しています。

最終用途カテゴリーの中では、病院と診療所が2024年に圧倒的な収益シェアを占め、今後数年間で大幅な成長が見込まれています。これらの施設は、人工股関節置換術を含む複雑な整形外科手術に対応できる設備が整っており、術前診察から術後のリハビリテーションに至るまで一貫したケアを提供しています。また、手術の精度を高めるロボット支援や画像システムなど、高度な手術技術へのアクセスも向上しています。こうした臨床環境で行われる低侵襲手術の件数が増加していることも、市場の成長をさらに後押ししています。

北米は2024年の世界市場シェアの50.6%を占めたが、これは主に、確立されたヘルスケアインフラの存在と高齢者人口の増加によるものです。同地域では、米国が2024年に38億4,000万米ドルの市場価値を記録しました。骨粗鬆症、関節炎、肥満の増加により、人工股関節置換術手術の需要が増加しています。国民の意識向上キャンペーンや手術オプションへのアクセスの改善も、手術件数の増加に寄与しています。

業界各社は、次世代インプラントやデジタル技術に投資することで、製品ラインの強化を続けています。3Dプリントインプラントやロボット手術システムなどの戦略的提携や技術革新は、メーカーが競争力を維持し、進化する患者のニーズによりよく対応するのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 外傷症例の増加

- 股関節炎と骨粗鬆症の有病率の増加

- 最近の技術の進歩

- パーソナライズされた股関節インプラントの需要増加

- 業界の潜在的リスク&課題

- インプラントや手術に伴う高額な費用

- 厳格な規制ガイドライン

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- 償還シナリオ

- 償還政策が市場成長に与える影響

- 特許情勢

- パイプライン分析

- 消費者行動分析

- 主要国における人工股関節置換術手続きの数

- 人工股関節置換術治療シナリオ

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 主な人工股関節置換術デバイス

- 部分的な人工股関節置換術デバイス

- リビジョン人工股関節置換術デバイス

- 股関節表面再建装置

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 金属とプラスチック

- セラミックオンメタル

- セラミックオンプラスチック

- セラミックオンセラミック

第7章 市場推計・予測:固定材別、2021年~2034年

- 主要動向

- セメントレス固定

- ハイブリッド固定

- セメント固定

第8章 市場推計・予測:インサート別、2021年~2034年

- 主要動向

- 非酸化ポリエチレンインサート

- 架橋ポリエチレンインサート

- 抗酸化ポリエチレンインサート

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院と診療所

- 外来手術センター

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- B Braun

- CONFIRMIS

- Corin

- DePuy Synthes(Johnson &Johnson)

- enovis

- ExaTech Inc

- KyOCERA

- Link

- Medacta International

- MicroPort Orthopedics

- ORTHO DEVELOPMENT

- Smith+Nephew

- stryker

- ZIMMER BIOMET

目次

The Global Hip Replacement Market was valued at USD 7.9 billion in 2024 and is estimated to grow at a CAGR of 3.9% to reach USD 11.4 billion by 2034. The market is experiencing growth due to a combination of technological innovation, increased surgical volume, and rising incidences of joint-related disorders. A growing elderly population, particularly those affected by degenerative joint diseases, continues to be a primary demographic undergoing hip replacement procedures. Moreover, the integration of robotics and minimally invasive surgical methods has significantly enhanced clinical outcomes. These advancements have led to shorter hospital stays, reduced recovery periods, and improved patient satisfaction, ultimately contributing to a higher adoption rate of hip replacement procedures globally.

Implant surgeries are increasingly common among older adults experiencing progressive joint deterioration. These procedures are more successful and widely accepted today, thanks to ongoing developments in surgical techniques and materials. In addition, improved healthcare infrastructure and better patient education regarding treatment outcomes have supported market expansion. The rising number of trauma cases and orthopedic injuries, along with favorable healthcare reimbursement, has also boosted the frequency of hip replacement surgeries. Innovations in implant design, compatibility, and durability further enable orthopedic surgeons to deliver effective, patient-specific solutions. The market continues to evolve with the increasing demand for enhanced mobility solutions and long-term performance among active aging populations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.9 Billion |

| Forecast Value | $11.4 Billion |

| CAGR | 3.9% |

In terms of product segmentation, primary hip replacement devices dominated the global market in 2024, with a recorded value of USD 5.8 billion. These devices remain the most commonly used implants due to their broad application across various surgical procedures. Their widespread use is attributed to their compatibility with multiple hip disorders and their ability to provide reliable, long-term results. An increasing number of hip implant procedures-driven by factors such as bone fractures and aging-related joint wear-has ensured continued growth for this product category.

Based on material type, metal-on-plastic implants led the market with a 56.4% share in 2024. This material combination remains a preferred choice due to its excellent wear resistance, affordability, and mechanical stability. The metal component effectively absorbs pressure, while the plastic liner reduces joint friction, leading to improved mobility and reduced wear over time. These implants are commonly used worldwide due to their effectiveness, surgeon familiarity, and lower revision rates, making them a go-to choice for both healthcare professionals and patients.

When analyzed by fixation method, cementless fixation systems emerged as the leading category in 2024 and are forecasted to grow at a CAGR of 4% through 2034. This segment has gained traction due to the long-term biological stability it offers. Unlike cemented fixation, which relies on synthetic adhesives, cementless implants promote natural bone growth around the implant surface. This biological integration offers increased longevity and reduces the chances of implant loosening over time. Younger patients, in particular, benefit from this fixation method due to its higher success rate over extended periods. Improved surface designs and material coatings have further driven demand for this approach, especially in minimally invasive and outpatient surgical settings.

The inserts segment of the market is also experiencing notable trends. Non-antioxidant polyethylene inserts are gaining attention and are projected to reach USD 3.7 billion by 2034. These inserts are known to reduce oxidative wear, which helps enhance implant longevity-a vital consideration for more active and younger individuals. Their growing usage is supported by their reliable clinical performance, broader availability, and simplified manufacturing processes. Healthcare professionals favor these inserts due to consistent procedural success and strong historical data supporting their long-term effectiveness.

Among end-use categories, hospitals and clinics held the dominant revenue share in 2024 and are anticipated to witness substantial growth over the coming years. These facilities are equipped to handle complex orthopedic surgeries, including hip replacements, and offer integrated care that spans pre-surgical consultation through post-surgical rehabilitation. They also benefit from increased access to advanced surgical technologies, including robotic assistance and imaging systems, which enhance procedural accuracy. The rising number of minimally invasive surgeries performed in these clinical environments further supports market growth.

North America accounted for 50.6% of the global market share in 2024, largely due to the presence of well-established healthcare infrastructure and a growing elderly population. Within the region, the United States registered a market value of USD 3.84 billion in 2024. Higher rates of osteoporosis, arthritis, and obesity are increasing the demand for hip replacement procedures. Public awareness campaigns and improved access to surgical options have also contributed to rising procedure volumes.

Industry players continue to enhance their product lines by investing in next-generation implants and digital technologies. Strategic collaborations and technological innovations, including 3D-printed implants and robotic surgical systems, are helping manufacturers stay competitive and better serve evolving patient needs.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Forecast model

- 1.6 Primary research and validation

- 1.6.1 Primary sources

- 1.7 Forecast model

- 1.8 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Material

- 2.2.4 Fixation material

- 2.2.5 Inserts

- 2.2.6 End use

- 2.3 CXO Perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in number of trauma cases

- 3.2.1.2 Increasing prevalence of hip arthritis and osteoporosis

- 3.2.1.3 Recent technological advancements

- 3.2.1.4 Growing demand for personalized hip implants

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with implants and surgery

- 3.2.2.2 Stringent regulatory guidelines

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Future market trends

- 3.8 Reimbursement scenario

- 3.8.1 Impact of reimbursement policies on market growth

- 3.9 Patent landscape

- 3.10 Pipeline analysis

- 3.11 Consumer behaviour analysis

- 3.12 Number of hip replacement procedures for key countries

- 3.13 Hip replacement treatment scenario

- 3.14 Porter's analysis

- 3.15 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn and Units)

- 5.1 Key trends

- 5.2 Primary hip replacement devices

- 5.3 Partial hip replacement devices

- 5.4 Revision hip replacement devices

- 5.5 Hip resurfacing devices

Chapter 6 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn and Units)

- 6.1 Key trends

- 6.2 Metal-on-plastic

- 6.3 Ceramic-on-metal

- 6.4 Ceramic-on-plastic

- 6.5 Ceramic-on-ceramic

Chapter 7 Market Estimates and Forecast, By Fixation Material, 2021 - 2034 ($ Mn and Units)

- 7.1 Key trends

- 7.2 Cementless fixation

- 7.3 Hybrid fixation

- 7.4 Cemented fixation

Chapter 8 Market Estimates and Forecast, By Inserts, 2021 - 2034 ($ Mn and Units)

- 8.1 Key trends

- 8.2 Non-antioxidant polyethylene inserts

- 8.3 Cross-linked polyethylene inserts

- 8.4 Antioxidant polyethylene inserts

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals and clinics

- 9.3 Ambulatory surgical centers

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn and Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 B Braun

- 11.2 CONFIRMIS

- 11.3 Corin

- 11.4 DePuy Synthes (Johnson & Johnson)

- 11.5 enovis

- 11.6 ExaTech Inc

- 11.7 KyOCERA

- 11.8 Link

- 11.9 Medacta International

- 11.10 MicroPort Orthopedics

- 11.11 ORTHO DEVELOPMENT

- 11.12 Smith+Nephew

- 11.13 stryker

- 11.14 ZIMMER BIOMET

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日