走行車重量計測の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Automotive Weigh in Motion Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755364

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

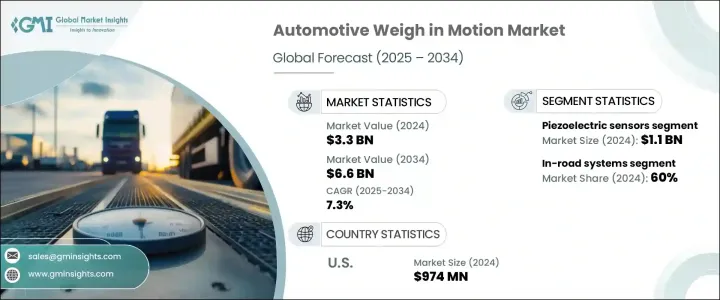

走行車重量計測の世界市場規模は、2024年に33億米ドルとなり、CAGR 7.3%で成長し、2034年には66億米ドルに達すると予測されています。

この上昇トレンドは、貨物通路、料金所、高速道路、物流ハブなどにおけるインテリジェント交通ソリューションとリアルタイム車両重量追跡に対する需要の高まりに後押しされています。交通を止めることなく正確で動的な車両重量を計測するニーズが拡大しているため、WIM技術が広く採用されるようになっています。政府および運輸当局は、交通安全性の向上、道路寿命の延長、軸重規制の確実な遵守を目的として、WIMシステムへの関心を高めています。人工知能、高度なセンサー、リアルタイムのデータ分析の統合により、WIMシステムは世界中の交通インフラにおいて、より信頼性が高く、効率的で、インテリジェントなものになりつつあります。

これらのシステムには現在、交通管理を合理化するためのクラウド統合、組み込みカメラ、高速データ転送、遠隔診断が含まれています。また、IoTを活用したセンサー、予知保全機能、デジタルツインシミュレーションの利用も、インフラ計画を再構築しています。内蔵された耐タンパー性、サイバーセキュリティ・プロトコル、コンプライアンス機能は、安全で効率的な道路監視をさらにサポートします。これらの技術革新により、当局や民間事業者はコスト削減、業務効率の向上、交通障害の軽減を実現するとともに、都市部と長距離輸送ルートの両方で環境の持続可能性を向上させることができます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 33億米ドル |

| 予測金額 | 66億米ドル |

| CAGR | 7.3% |

圧電センサセグメントは2024年に11億米ドルを生み出し、世界のWIM市場の主要センサタイプとなりました。ピエゾ式センサが広く使われているのは、信号感度が高く、サイズがコンパクトで、高速道路の速度で重量を測定できるからです。これらのセンサーは、簡単な設置プロセスと最小限の維持管理の必要性により、交通当局に好まれる選択肢となっています。スケーラブルでコスト効率の高いシステムが不可欠な大規模展開では、特に効果的です。既存の道路インフラとの互換性に加え、交通データ・アプリケーション、料金オペレーション、貨物分析をサポートする能力により、スマート・モビリティ・プロジェクトにおいて非常に魅力的なものとなっています。

2024年には、道路内システムが60%のシェアで市場をリードします。これらのシステムは道路に直接埋め込まれ、交通遅延を引き起こすことなく継続的で正確な重量データを提供します。交通量の多い通路、貨物輸送ルート、料金所などに最適です。インテリジェント交通ネットワークへのシームレスな統合により、自動化が可能になり、取締りの精度が向上し、運用スループットが向上します。当局は、高速車両分類、リアルタイムのコンプライアンス・チェック、動的車両評価を、すべて手作業なしで実施する道路内WIMシステムに依存しています。視認性が低く高性能であるため、道路インフラの最適化や規制の執行に不可欠なツールとなっています。

米国の走行車重量計測市場は、2024年に9億7,400万米ドルを生み出し、2034年までCAGR 7.6%で成長すると予測されています。同国はインフラ近代化と交通のデジタル変革を強力に推進しており、WIM導入の主要なリーダーとして位置づけられています。道路品質の維持、貨物量の管理、軸重遵守規則の遵守に重点を置くことで、先進的な重量モニタリングシステムの全国展開が推進されています。世界有数の広範な高速道路システムを持つ米国は、都市部と農村部の両方の貨物輸送路を対象に、高精度のWIM技術への投資を続けています。連邦政府および州レベルの資金調達、強固なITSエコシステム、データ主導の輸送政策イニシアチブの高まりに支えられ、米国市場は次世代ウェイ・イン・モーション・プラットフォームの革新と展開の重要な拠点であり続けています。

この市場参入企業には、Intercomp、SWARCO AG、Kistler、Q-Free ASA、Kapsch TrafficCom、Siemens Mobility、TE Connectivity、TDC Systems Ltd.、Econolite、International Road Dynamicsなどがあります。自動車重量計測市場での地位を高めるため、各社は継続的な技術革新、特にAIを活用した重量分析、センサーの統合、スマートインフラへの対応に注力しています。クラウド接続、機械学習、エッジコンピューティングへの投資は、リアルタイム診断と自動車両分類の実現に役立っています。各社はまた、さまざまな道路状況や交通密度に対応するため、拡張可能なモジュラーシステムを提供しています。交通当局やスマートシティプランナーとのコラボレーションは、応用分野を拡大する上で中心的な存在となっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:設備別、2021年~2034年

- 主要動向

- 道路内システム

- 重量橋システム

- 車載システム

第6章 市場推計・予測:センサー別、2021年~2034年

- 主要動向

- 圧電センサー

- 曲げ板

- 単一ロードセル

- その他

第7章 市場推計・予測:車軸構成別、2021年~2034年

- 主要動向

- シングル軸

- タンデム軸

- トリプル軸

- クワッド軸

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 重量制限

- 交通データ収集

- 重量制料金

- 橋梁保護

- 産業用トラックの計量

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 政府

- 輸送

- 民間部門

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- Adient

- Applus

- Axis Communications

- Cestel

- Continental

- Econolite

- Efftronics Systems

- Golden River

- IAC Group

- Intercomp

- International Road Dynamics

- Kapsch TrafficCom

- Kasai Kogyo

- Q-Free ASA

- Siemens Mobility

- SWARCO AG

- TDC Systems

- TE Connectivity

- Wavetronix

- WIM Systems

目次

The Global Automotive Weigh in Motion Market was valued at USD 3.3 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 6.6 billion by 2034. This upward trend is fueled by rising demand for intelligent traffic solutions and real-time vehicle weight tracking across freight corridors, toll booths, highways, and logistics hubs. The expanding need for accurate, dynamic vehicle weighing without halting traffic is leading to the widespread adoption of WIM technologies. Governments and transportation authorities are increasingly turning to WIM systems to boost road safety, extend road lifespans, and ensure compliance with axle-load regulations. With the integration of artificial intelligence, advanced sensors, and real-time data analytics, WIM systems are becoming more reliable, efficient, and intelligent across transportation infrastructures worldwide.

These systems now include cloud integration, embedded cameras, high-speed data transfer, and remote diagnostics to streamline traffic management. The use of IoT-powered sensors, predictive maintenance features, and digital twin simulations has also reshaped infrastructure planning. Built-in tamper resistance, cybersecurity protocols, and compliance features further support safe and efficient road monitoring. These innovations empower authorities and commercial operators to cut costs, enhance operational efficiency, and reduce traffic disruptions while improving environmental sustainability across both urban and long-haul transport routes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.3 billion |

| Forecast Value | $6.6 billion |

| CAGR | 7.3% |

The piezoelectric sensors segment generated USD 1.1 billion in 2024, making it the leading sensor type in the global WIM market. Their widespread use stems from their high signal sensitivity, compact size, and ability to measure weights at highway speeds. These sensors are a preferred choice for transportation authorities due to their straightforward installation process and minimal upkeep needs. They are particularly effective in large-scale deployments, where scalable and cost-efficient systems are essential. Their compatibility with existing road infrastructure, as well as their ability to support traffic data applications, toll operations, and freight analytics, makes them highly attractive in smart mobility projects.

In 2024, in-road systems led the market with a 60% share. These systems are directly embedded into roadways and provide continuous, accurate weight data without causing traffic delays. They are ideally suited for high-traffic corridors, freight transport routes, and toll stations. Their seamless integration into intelligent transportation networks enables automation, improves enforcement accuracy, and increases operational throughput. Authorities rely on in-road WIM systems to carry out high-speed vehicle classification, real-time compliance checks, and dynamic vehicle assessments, all without manual intervention. Their low visibility and high performance make them vital tools in road infrastructure optimization and regulatory enforcement.

U.S. Automotive Weigh in Motion Market generated USD 974 million in 2024 and is estimated to grow at a CAGR of 7.6% through 2034. The country's strong push toward infrastructure modernization and digital transformation in transportation has positioned it as a key leader in WIM adoption. The focus on preserving road quality, managing freight volumes, and adhering to axle-load compliance rules has driven nationwide deployments of advanced weight monitoring systems. With one of the most extensive highway systems globally, the U.S. continues to invest in high-precision WIM technology for both urban and rural freight corridors. Backed by federal and state-level funding, robust ITS ecosystems, and increasing data-driven transport policy initiatives, the U.S. market remains a key hub for innovation and deployment of next-gen weigh-in-motion platforms.

Key industry participants in the Automotive Weigh in Motion Market include Intercomp, SWARCO AG, Kistler, Q-Free ASA, Kapsch TrafficCom, Siemens Mobility, TE Connectivity, TDC Systems Ltd., Econolite, and International Road Dynamics. To enhance their position in the automotive weigh-in-motion market, companies are focusing on continuous innovation, particularly in AI-powered weight analytics, sensor integration, and smart infrastructure compatibility. Investments in cloud connectivity, machine learning, and edge computing help deliver real-time diagnostics and automated vehicle classification. Firms are also offering scalable modular systems to meet varying roadway conditions and traffic densities. Collaborations with transportation authorities and smart city planners have become central to expanding application areas.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Installation

- 2.2.3 Sensor

- 2.2.4 Axle configuration

- 2.2.5 Application

- 2.2.6 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Installation, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 In-road systems

- 5.3 Weight bridge systems

- 5.4 Onboard systems

Chapter 6 Market Estimates & Forecast, By Sensor, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Piezoelectric sensors

- 6.3 Bending plate

- 6.4 Single load cell

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Axle Configuration, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Single axle

- 7.3 Tandem axle

- 7.4 Triple axle

- 7.5 Quad axle

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Weight enforcement

- 8.3 Traffic data collection

- 8.4 Weight based tolling

- 8.5 Bridge protection

- 8.6 Industrial truck weighing

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Government

- 9.3 Transportation

- 9.4 Private sector

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Adient

- 11.2 Applus

- 11.3 Axis Communications

- 11.4 Cestel

- 11.5 Continental

- 11.6 Econolite

- 11.7 Efftronics Systems

- 11.8 Golden River

- 11.9 IAC Group

- 11.10 Intercomp

- 11.11 International Road Dynamics

- 11.12 Kapsch TrafficCom

- 11.13 Kasai Kogyo

- 11.14 Q-Free ASA

- 11.15 Siemens Mobility

- 11.16 SWARCO AG

- 11.17 TDC Systems

- 11.18 TE Connectivity

- 11.19 Wavetronix

- 11.20 WIM Systems

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日