|

市場調査レポート

商品コード

1755359

産業用真空ポンプ市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年)Industrial Vacuum Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 産業用真空ポンプ市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年) |

|

出版日: 2025年05月23日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

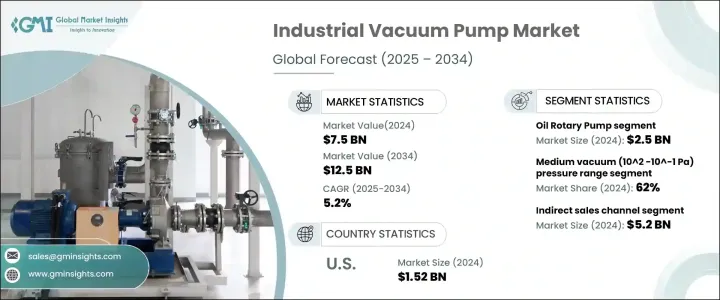

世界の産業用真空ポンプ市場は、2024年には75億米ドルと評価され、複数の最終用途分野にわたる需要の増加により、CAGR 5.2%で成長し、2034年には125億米ドルに達すると予測されています。

これらの真空ポンプは、精密製造や高純度処理を必要とする産業で広く使用されており、市場拡大に大きく貢献しています。制御された環境を必要とする繊細な作業を扱う部門に広く適用されることで、産業ワークフローにおける真空ポンプの関連性が確固たるものとなっています。

半導体分野の進歩に伴い、相互接続市場の需要も高まっています。産業オートメーションと生産基準のクリーン化に伴い、真空ポンプ技術は世界中でますます採用されるようになっています。とはいえ、高額な先行投資と継続的なメンテナンスコストは、特に中小企業にとっては依然として大きな足かせとなっています。さらに、操作の複雑さと技術的な専門知識の必要性から、高度でないセットアップでは採用が難しくなり、新興市場での成長に限界が生じています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025~2034年 |

| 当初の市場規模 | 75億米ドル |

| 市場規模予測 | 125億米ドル |

| CAGR | 5.2% |

これらの地域の多くは、熟練技術者不足に直面しており、最新の真空システムの管理・保守に不可欠な専門トレーニング・プログラムへのアクセスも不足しています。日常的なトラブルシューティングやメンテナンスでさえ大きな障害となり、ダウンタイムの増加や装置寿命の低下につながる可能性があります。さらに、複雑な機械をサポートするための限られたインフラと相まって、技術スタッフの派遣に関連する高コストが、中小産業が高度な真空ポンプ技術にアップグレードすることをさらに躊躇させています。

オイルロータリポンプ分野は、2024年に25億米ドルを生み出し、2034年までCAGR 5%で力強い勢いを維持すると予測されています。これらのポンプは、安定した真空出力と、可変圧力条件下での連続的で過酷な運転に耐える能力が特に評価されています。堅牢な構造と高い性能により、精度と一貫性が不可欠な産業環境において、最適なソリューションとなっています。過酷なプロセス環境への適応性と最小限のダウンタイムが、材料加工から真空コーティングまで、さまざまな分野での有用性をさらに高めています。

流通の観点からは、間接販売セグメントは2024年に52億米ドルを生み出し、2034年までCAGR 4.7%で成長すると予想されています。間接販売の成功は、真空ポンプ製品の幅広い選択肢を提供する代理店、再販業者、デジタルマーケットプレースの確立されたネットワークによってもたらされます。これらのチャネルは、エンドユーザーの調達を簡素化するだけでなく、システムのカスタマイズ、技術トレーニング、購入後のサポート、地域在庫による迅速な納品などの付加価値サービスを提供しています。

米国の産業用真空ポンプの2024年の市場規模は15億2,000万米ドルで、2034年までにCAGR 5.2%で成長すると予測されています。このリーダーシップは、エレクトロニクス、医薬品、特殊化学品など、高純度製造プロセスを必要とする分野における同国の高度なインフラが後押ししています。製造業の近代化に対する政府の支援と自動化技術の広範な統合が、市場の見通しをさらに強めています。

世界の産業用真空ポンプ市場に貢献している著名企業には、Gardner Denver、Ebara Corporation、Pfeiffer Vacuum GmbH、Atlas Copco AB(Edwards)、ULVAC Inc.、Flowserve Corporation、Global Vac、Wintek Corporation、Ingersoll Rand Inc.、Busch Vacuum Solutions、Becker Pumps Corporation、Tsurumi Manufacturing Co.Ltd.、Graham Corporation、Agilent Technologiesです。産業用真空ポンプ市場の主要企業が採用している主な戦略には、製品革新、生産能力拡大、戦略的合併や提携への注力などがあります。各社は、自動化とデジタル統合の拡大をターゲットに、エネルギー効率の高いスマート真空技術を導入するための研究開発に投資しています。各業界に特化したOEMとの提携は、応用範囲の拡大に役立っています。流通網を通じた地理的拡大は、地域的な足跡をより強固なものにし、アフターサービスとカスタマイズされた提供は顧客維持を後押しします。

目次

第1章 分析手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 販売代理店

- 小売業者

- トランプ政権による関税

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(顧客へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 影響要因

- 促進要因

- 半導体・エレクトロニクス産業における需要の増加

- 化学および製薬産業の拡大

- 食品・飲料業界での採用増加

- 製造業と産業プロセスの成長

- 業界の潜在的リスクと課題

- 初期投資と維持費が高め

- 複雑さと技術的課題

- 促進要因

- テクノロジーとイノベーションの情勢

- 成長可能性分析

- 規制情勢

- 価格分析

- ポーターのファイブフォース分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場の推計・予測:種類別(2021~2034年)

- 主要動向

- 液封式真空ポンプ

- オイルロータリーポンプ

- ルーツポンプ

- 乾燥真空ポンプ

- 多段ルーツ真空ポンプ

- 乾燥スクリュー真空ポンプ

- 乾燥スクロール真空ポンプ

- 乾燥ダイヤフラム真空ポンプ

- 乾燥ロータリーベーン真空ポンプ

- 乾燥ロッキングピストン真空ポンプ

- 乾燥ロータリークロウ真空ポンプ

- 乾燥ターボ真空ポンプ

第6章 市場の推計・予測:圧力範囲別(2021~2034年)

- 主要動向

- 低真空圧(10^5~10^2 Pa)

- 中真空圧(10^2~10^-1 Pa)

第7章 市場の推計・予測:サイズ別(2021~2034年)

- 主要動向

- 小型(10 m3/h以下)

- 中型(10~100 m3/h)

- 大型(100 m3/h以上)

第8章 市場の推計・予測:最終用途産業別(2021~2034年)

- 主要動向

- 半導体

- 上下水道処理

- 化学・石油化学

- 鉱業

- 食品・飲料

- 建設業

- 石油・ガス

- 製薬

- その他(農業、繊維など)

第9章 市場の推計・予測:流通チャネル別(2021~2034年)

- 主要動向

- 直接販売

- 間接販売

第10章 市場の推計・予測:地域別(2021~2034年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- マレーシア

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第11章 企業プロファイル

- Agilent Technologies

- Atlas Copco AB(Edwards)

- Becker Pumps Corporation

- Busch Vacuum Solutions

- Ebara Corporation

- Flowserve Corporation

- Gardner Denver

- Global Vac

- Graham Corporation

- Ingersoll Rand Inc.

- Pfeiffer Vacuum GmbH

- Tsurumi Manufacturing Co. Ltd

- ULVAC Inc.

- Wintek Corporation

The Global Industrial Vacuum Pump Market was valued at USD 7.5 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 12.5 billion by 2034, driven by the increasing demand across multiple end-use sectors. These vacuum pumps are extensively used in industries requiring precision manufacturing and high-purity processing, contributing significantly to market expansion. Their widespread application across sectors dealing with sensitive operations requiring a controlled environment has solidified their relevance in industrial workflows.

As the semiconductor segment advances, it fuels demand in interconnected markets. With rising industrial automation and cleaner production standards, vacuum pump technology is increasingly being adopted across the globe. Nevertheless, the high upfront investment and the ongoing maintenance costs remain major deterrents, especially for smaller companies. In addition, the operational complexity and the need for technical expertise make adoption more challenging in less advanced setups, creating growth limitations in emerging markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.5 Billion |

| Forecast Value | $12.5 Billion |

| CAGR | 5.2% |

Many of these regions face a shortage of skilled technicians and lack access to specialized training programs, essential for managing and maintaining modern vacuum systems. Even routine troubleshooting or maintenance can become a significant hurdle, leading to increased downtime and reduced equipment lifespan. Moreover, the high cost associated with technical staffing, coupled with limited infrastructure to support complex machinery, further deters smaller industries from upgrading to advanced vacuum pump technologies.

The oil rotary pump segment generated USD 2.5 billion in 2024 and is projected to maintain strong momentum with a CAGR of 5% through 2034. These pumps are particularly valued for their stable vacuum output and ability to withstand continuous, demanding operations under variable pressure conditions. Their robust construction and high performance make them a go-to solution in industrial environments where precision and consistency are mission-critical. Their adaptability to harsh process environments and minimal downtime further boost their utility across various sectors, from material processing to vacuum coating.

From a distribution standpoint, the indirect sales segment generated USD 5.2 billion in 2024 and is anticipated to grow at a CAGR of 4.7% through 2034. The success of indirect sales is driven by a well-established network of distributors, resellers, and digital marketplaces that offer a broad selection of vacuum pump products. These channels simplify procurement for end-users but provide value-added services like system customization, technical training, post-purchase support, and faster delivery through regional inventories.

United States Industrial Vacuum Pump Market was valued at USD 1.52 billion in 2024, projected to grow at a CAGR of 5.2% by 2034. This leadership is fueled by the country's advanced infrastructure in sectors requiring high-purity manufacturing processes, such as electronics, pharmaceuticals, and specialty chemicals. Government support for modernizing manufacturing and the widespread integration of automation technologies further strengthens the market outlook.

Prominent companies contributing to the Global Industrial Vacuum Pump Market include Gardner Denver, Ebara Corporation, Pfeiffer Vacuum GmbH, Atlas Copco AB (Edwards), ULVAC Inc., Flowserve Corporation, Global Vac, Wintek Corporation, Ingersoll Rand Inc., Busch Vacuum Solutions, Becker Pumps Corporation, Tsurumi Manufacturing Co. Ltd, Graham Corporation, and Agilent Technologies. Key strategies adopted by leading players in the industrial vacuum pump market include a strong focus on product innovation, capacity expansion, and strategic mergers or partnerships. Companies are investing in R&D to introduce energy-efficient and smart vacuum technologies, targeting increased automation and digital integration. Collaborations with industry-specific OEMs help broaden their application reach. Geographic expansion through distribution networks ensures stronger regional footprints, while after-sales services and customized offerings help boost customer retention.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Retailers

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Trade impact

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (Cost to customers)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook & future considerations

- 3.2.1 Trade impact

- 3.3 Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing demand in semiconductor and electronics industry

- 3.3.1.2 Expansion in chemical and pharmaceutical industries

- 3.3.1.3 Rising adoption in food and beverage industry

- 3.3.1.4 Growth in manufacturing and industrial processes

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 High initial investment and maintenance costs

- 3.3.2.2 Complexity and technical challenges

- 3.3.1 Growth drivers

- 3.4 Technology & innovation landscape

- 3.5 Growth potential analysis

- 3.6 Regulatory landscape

- 3.7 Pricing analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 – 2034, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Liquid ring vacuum pump

- 5.3 Oil rotary pump

- 5.4 Roots pump

- 5.5 Dry vacuum pump

- 5.6 Multi-stage roots vacuum pump

- 5.6.1 Dry screw vacuum pump

- 5.6.2 Dry scroll vacuum pump

- 5.6.3 Dry diaphragm vacuum pump

- 5.6.4 Dry rotary vane vacuum pump

- 5.6.5 Dry rocking piston vacuum pump

- 5.6.6 Dry rotary crow vacuum pump

- 5.6.7 Dry turbo vacuum pump

Chapter 6 Market Estimates & Forecast, By Pressure Range, 2021 – 2034, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Low vacuum (10^5-10^2 Pa)

- 6.3 Medium vacuum (10^2 -10^-1 Pa)

Chapter 7 Market Estimates & Forecast, By Size, 2021 – 2034, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Small (< 10 m3/h)

- 7.3 Medium (10-100 m3/h)

- 7.4 Large (> 100 m3/h)

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021 – 2034, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Semiconductor

- 8.3 Water & wastewater treatment

- 8.4 Chemicals and petrochemicals

- 8.5 Mining

- 8.6 Food and beverages

- 8.7 Construction

- 8.8 Oil & gas

- 8.9 Pharmaceutical

- 8.10 Others (Agricultural, textile, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 – 2034, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2021 – 2034, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 11.1 Agilent Technologies

- 11.2 Atlas Copco AB (Edwards)

- 11.3 Becker Pumps Corporation

- 11.4 Busch Vacuum Solutions

- 11.5 Ebara Corporation

- 11.6 Flowserve Corporation

- 11.7 Gardner Denver

- 11.8 Global Vac

- 11.9 Graham Corporation

- 11.10 Ingersoll Rand Inc.

- 11.11 Pfeiffer Vacuum GmbH

- 11.12 Tsurumi Manufacturing Co. Ltd

- 11.13 ULVAC Inc.

- 11.14 Wintek Corporation