雑穀の市場機会と促進要因、産業動向分析、2025年~2034年予測

Millets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755354

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

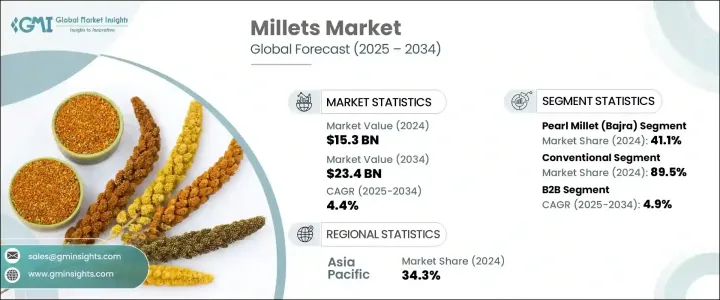

雑穀の世界市場は、2024年には153億米ドルと評価され、CAGR 4.4%で成長し、2034年には234億米ドルに達すると推定されています。

この成長は、食物繊維とタンパク質を豊富に含むヘルシーなグルテンフリー食品に対する消費者の関心の高まりが大きな要因となっています。雑穀の栄養的利点に対する認識が高まるにつれて、現代の食生活では雑穀を取り入れることが一般的になりつつあります。消費者は雑穀を伝統的な消費だけでなく、機能性食品、ウェルネスダイエット、持続可能な食習慣の役割としても注目しています。近年、雑穀は、特に焼き菓子、スナック、飲料など、幅広い新しい用途で利用されるようになり、健康上の利点だけでなく、食感や味も改善されています。

また、厳しい気候条件にも耐えられることから、水の利用可能性が限られた地域でも信頼できる食料源となり、食料安全保障における重要性を高めています。加工と製品開発における革新は、引き続き世界の雑穀消費の原動力となっています。食料システム全体で持続可能性がより強く重視されるようになるにつれて、雑穀は、環境に配慮した食生活に理想的な、気候変動に対応できる穀物として認識されるようになっています。持続可能な植物由来の食品に対する都市市場での需要の高まりが、市場の長期的な軌道をさらに後押ししています。

| 市場の範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 153億米ドル |

| 予測金額 | 234億米ドル |

| CAGR | 4.4% |

支援的な政策枠組みと制度的インセンティブが引き続きこの市場を後押ししています。雑穀を普及させるためのいくつかの世界の取り組みは、雑穀をベースとした食品産業に対する認知度の向上と投資の促進に大きく貢献しています。政府や農業団体は、財政支援、バリューチェーンのインフラ整備、キビ製品開発における起業家精神の育成によってキビ栽培を奨励しています。こうした措置は農家を支援するだけでなく、流通を合理化し、国内市場と国際市場の両方へのアクセスを広げることにも役立っています。

品種別では、2024年にはナラキビが41.1%のシェアを占めて市場をリードし、これは63億米ドルの市場規模に相当します。それぞれの雑穀品種は、その栄養プロファイルと異なる食餌への適合性に基づいて独自の価値を有しています。高タンパク質や高カルシウム含量で好まれるものもあれば、グルテンフリーやビーガン食に使用されることで関心を集めているものもあります。世界の需要がクリーン・ラベルやアレルゲンに配慮した食品にシフトし続けているため、これらの穀物は各地域で力強い成長機会を確保しています。

性質に基づくと、2024年には従来の雑穀が89.5%のシェアを占め、予測期間中のCAGRは5.8%と高い成長が見込まれます。このセグメントは、手頃な価格と入手のしやすさから、引き続き幅広い消費者層にアピールしています。しかし、有機雑穀の分野も、特に消費者が化学薬品を使わず環境に優しい食品の選択肢を求めている都市市場において、関心の高まりを目の当たりにしています。持続可能な農業を推進する政府のプログラムも、有機生産された雑穀の魅力を高めています。現在、有機雑穀のシェアは小さいが、クリーンな栄養に対する需要の高まりが、特に高級小売スペースや健康志向の高い層への浸透を促進すると予想されます。

形態別に分類すると、全粒粉は2024年の市場シェア全体の39.7%を占め、その栄養価の高さと最小限の加工により強い関連性を維持しています。雑穀粉は、クッキー、パン、健康スナックなどグルテンフリーのベーカリー製品の万能材料として世界の人気を獲得し続けています。フレークは朝食用シリアルやスナックバーでますます好まれるようになっており、これは市場が現代的で利便性を重視した消費パターンに合致していることを反映しています。食習慣の進化に伴い、雑穀をベースとした調理済み製品およびすぐに食べられる製品への需要も高まっており、メーカーは小売店の棚に多様な製品ラインを導入する機会を得ています。

B2B分野は急速に拡大しており、2034年までのCAGRは4.9%と予測されます。この成長の原動力となっているのは、機能的で持続可能な原料として雑穀をさまざまな用途に取り入れている食品メーカー、機関投資家、飼料メーカーからの需要の増加です。パッケージ食品、学校給食プログラム、プライベート・ラベルの健康食品への雑穀の統合により、大規模な調達機会が開かれつつあります。より多くの産業が雑穀の健康と持続可能性の利点を利用するにつれて、B2B分野は力強い勢いを見せると予想されます。

地域別では、アジア太平洋が2024年に34.3%で最大の売上シェアを占め、これは高い生産量と国内消費の増加に後押しされています。この地域は、歴史的な栽培パターンと健康意識の高まりにより、雑穀の牙城であり続けています。都市化、所得の増加、農業政策の支援により、伝統的な食生活だけでなく現代的な食品イノベーションにおいても雑穀の利用が増加しています。

雑穀市場の主要企業は、市場での足跡を拡大し、ブランドのポジショニングを強化するための戦略的イニシアチブを積極的に実施しています。主要企業は、進化する消費者の嗜好に対応するため、雑穀をベースとした調理済み食品、スナック、朝食用シリアル、グルテンフリーのベーカリー製品を発売し、製品イノベーションに投資しています。多くの企業がフードテック新興企業や研究機関と協力し、雑穀本来の効能を維持しながら保存性と味を高める栄養密度の高い製剤を開発しています。小売チェーンやeコマース・プラットフォームとの戦略的提携も一般的になりつつあり、より幅広い製品の認知度と消費者へのリーチを可能にしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)

(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- パールミレット(バジュラ)

- シコクビエ(ラギ)

- アワ

- キビ

- ソルガム(ジョワール)

- ヒエ

- コドモキビ

- 小さなキビ

- その他

第6章 市場推計・予測:性質別、2021年~2034年

- 主要動向

- オーガニック

- 従来型

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 食品

- ベーカリー製品

- 朝食用シリアルとポリッジ

- スナック類と塩味製品

- 幼児用食品

- 伝統食品

- その他

- 飲料

- アルコール飲料

- ノンアルコール飲料

- 動物飼料

- 家禽飼料

- 牛の飼料

- その他

- 栄養補助食品および栄養補助食品

- その他

第8章 市場推計・予測:形態別、2021年~2034年

- 主要動向

- 全粒穀物

- 小麦粉

- フレーク

- RTC

- RTE

- その他

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- B2B

- 食品メーカー

- 動物飼料産業

- HoReCa(ホテル・レストラン・カフェ)

- その他

- B2C

- スーパーマーケットとハイパーマーケット

- 専門店

- コンビニエンスストア

- オンライン小売

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第11章 企業プロファイル

- Nestle S.A.

- Archer Daniels Midland Company

- Cargill, Incorporated

- Bunge Limited

- Kellogg Company

- PepsiCo, Inc.(Quaker Oats)

- General Mills, Inc.

- Britannia Industries Ltd.

- ITC Limited

- Patanjali Ayurved Limited

- Organic India Pvt. Ltd.

- 24 Mantra Organic(Sresta Natural Bioproducts)

- Nature's Path Foods

- Bob's Red Mill Natural Foods

- Arrowhead Mills(Hain Celestial Group)

目次

The Global Millets Market was valued at USD 15.3 billion in 2024 and is estimated to grow at a CAGR of 4.4% to reach USD 23.4 billion by 2034. This growth is largely driven by rising consumer interest in healthy, gluten-free foods rich in fiber and protein. With increasing awareness about the nutritional benefits of millets, their inclusion in modern diets is becoming more common. Consumers are turning to millets not just for traditional consumption but also for their role in functional foods, wellness diets, and sustainable food practices. In recent years, millets have found a place in a wide range of new applications, especially in baked goods, snacks, and beverages, where they offer not just health benefits but also improved texture and taste.

Their ability to withstand harsh climatic conditions also makes them a reliable food source in regions with limited water availability, reinforcing their importance for food security. Innovations in processing and product development continue to drive millet consumption globally. As sustainability becomes a stronger focus across food systems, millets are being recognized as climate-smart grains, ideal for environmentally-conscious diets. Growing demand in urban markets for sustainable and plant-based food products further supports the market's long-term trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.3 Billion |

| Forecast Value | $23.4 Billion |

| CAGR | 4.4% |

Supportive policy frameworks and institutional incentives continue to fuel this market. Several global efforts to promote millet have significantly contributed to building awareness and driving investment in millet-based food industries. Governments and agricultural bodies are encouraging millet cultivation by offering financial support, creating value-chain infrastructure, and fostering entrepreneurship in millet product development. Such measures not only support farmers but also help streamline distribution and widen accessibility for both domestic and international markets.

By type, pearl millet led the market in 2024, holding a share of 41.1%, which equates to a market size of USD 6.3 billion. Each millet variety holds unique value based on its nutrient profile and suitability for different diets. While some are favored for their high protein or calcium content, others are gaining interest for their use in gluten-free and vegan diets. As global demand continues to shift towards clean-label and allergen-friendly foods, these grains are securing strong growth opportunities across regions.

Based on nature, in 2024, conventional millets dominated with an 89.5% share and are expected to grow at a higher CAGR of 5.8% during the forecast period. This segment continues to appeal to a broader consumer base due to affordability and easy availability. However, the organic millet segment is also witnessing increased interest, especially in urban markets where consumers are seeking chemical-free and eco-friendly food options. Government programs that promote sustainable agriculture are also enhancing the appeal of organically produced millets. Although organic millets currently occupy a smaller share, rising demand for clean nutrition is expected to boost their penetration, particularly in premium retail spaces and health-conscious demographics.

When segmented by form, the whole grain accounted for 39.7% of the total market share in 2024, maintaining strong relevance due to its nutritional richness and minimal processing. Millet flour continues to gain popularity globally as a versatile ingredient in gluten-free bakery products, including cookies, breads, and health snacks. Flakes are increasingly favored for breakfast cereals and snack bars, reflecting the market's alignment with modern, convenience-driven consumption patterns. With evolving dietary habits, the demand for millet-based ready-to-cook and ready-to-eat offerings is also rising, providing manufacturers the opportunity to introduce diverse product lines across retail shelves.

The B2B segment is expanding rapidly, with a projected CAGR of 4.9% through 2034. This growth is driven by increased demand from food manufacturers, institutional buyers, and animal feed producers who are integrating millet as a functional and sustainable ingredient in a wide variety of applications. The integration of millets into packaged foods, school meal programs, and private-label health foods is opening up large-scale procurement opportunities. As more industries tap into the health and sustainability benefits of millets, the B2B segment is expected to witness strong momentum.

Regionally, Asia Pacific held the largest revenue share in 2024 at 34.3%, fueled by high production and rising domestic consumption. The region continues to be a stronghold for millets due to historical cultivation patterns and increasing health awareness. Urbanization, rising incomes, and supportive agriculture policies are boosting millet usage not only in traditional diets but also in contemporary food innovations.

Key players in the millets market are actively implementing strategic initiatives to expand their market footprint and strengthen brand positioning. Leading companies are investing in product innovation by launching millet-based ready-to-eat meals, snacks, breakfast cereals, and gluten-free bakery items to cater to evolving consumer preferences. Many are collaborating with food tech startups and research institutions to develop nutrient-dense formulations that enhance shelf life and taste while retaining the grains' natural benefits. Strategic partnerships with retail chains and e-commerce platforms are also becoming common, allowing broader product visibility and consumer reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pearl millet (Bajra)

- 5.3 Finger millet (Ragi)

- 5.4 Foxtail millet

- 5.5 Proso millet

- 5.6 Sorghum (Jowar)

- 5.7 Barnyard millet

- 5.8 Kodo millet

- 5.9 Little millet

- 5.10 Others

Chapter 6 Market Estimates and Forecast, By Nature, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Organic

- 6.3 Conventional

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food

- 7.2.1 Bakery products

- 7.2.2 Breakfast cereals & porridges

- 7.2.3 Snacks & savory products

- 7.2.4 Infant food

- 7.2.5 Traditional foods

- 7.2.6 Others

- 7.3 Beverages

- 7.3.1 Alcoholic beverages

- 7.3.2 Non-alcoholic beverages

- 7.4 Animal feed

- 7.4.1 Poultry feed

- 7.4.2 Cattle feed

- 7.4.3 Others

- 7.5 Nutraceuticals & dietary supplements

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Form, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Whole grain

- 8.3 Flour

- 8.4 Flakes

- 8.5 Ready-to-cook

- 8.6 Ready-to-eat

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 B2B

- 9.2.1 Food manufacturers

- 9.2.2 Animal feed industry

- 9.2.3 HoReCa (Hotels, Restaurants, Cafes)

- 9.2.4 Others

- 9.3 B2C

- 9.3.1 Supermarkets & Hypermarkets

- 9.3.2 Specialty stores

- 9.3.3 Convenience stores

- 9.3.4 Online retail

- 9.3.5 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.3.7 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Nestle S.A.

- 11.2 Archer Daniels Midland Company

- 11.3 Cargill, Incorporated

- 11.4 Bunge Limited

- 11.5 Kellogg Company

- 11.6 PepsiCo, Inc. (Quaker Oats)

- 11.7 General Mills, Inc.

- 11.8 Britannia Industries Ltd.

- 11.9 ITC Limited

- 11.10 Patanjali Ayurved Limited

- 11.11 Organic India Pvt. Ltd.

- 11.12 24 Mantra Organic (Sresta Natural Bioproducts)

- 11.13 Nature's Path Foods

- 11.14 Bob's Red Mill Natural Foods

- 11.15 Arrowhead Mills (Hain Celestial Group)

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日