|

市場調査レポート

商品コード

1755352

脊椎インプラント市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年)Spinal Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 脊椎インプラント市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年) |

|

出版日: 2025年06月03日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

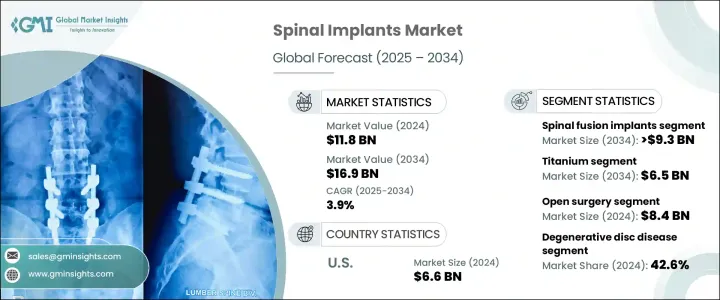

世界の脊椎インプラント市場は、2024年には118億米ドルと評価され、CAGR 3.9%で成長し、2034年には169億米ドルに達すると予測されています。

需要の高まりは、高齢化人口の増加、脊椎疾患の増加、低侵襲手術へのシフト、インプラント材料や手術手技の技術進歩が背景にあります。脊柱管狭窄症、椎間板変性症、椎間板ヘルニアなどの脊椎疾患が、特に高齢者の間で蔓延するにつれ、外科的介入と脊椎安定化ソリューションの必要性は上昇の一途をたどっています。

肥満や座りっぱなしのライフスタイルは、脊椎変性にさらに拍車をかけます。その結果、より多くの患者が外科的矯正を選択するようになり、特に痛みの軽減と回復の早さを提供する新しいソリューションが注目されています。脊椎手術にロボットシステムやナビゲーションツールが導入されたことで、手術の精度が高まっただけでなく、合併症の発生率も最小化されたため、先進的なインプラントの使用が奨励されています。多くの機器メーカーは、低侵襲手技に合わせたインプラントを設計することで対応しており、コストが徐々に低下し、利用しやすさが向上するにつれて、世界的に幅広い臨床採用を促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025~2034年 |

| 当初の市場規模 | 118億米ドル |

| 市場規模予測 | 169億米ドル |

| CAGR | 3.9% |

脊椎固定インプラント分野は、CAGR 4.3%で力強い成長を遂げ、2034年には93億米ドルに達すると予測されます。これらの器具が広く使用されているのは、変性や外傷によって引き起こされる脊椎の不安定性を治療する上で重要な役割を担っているからです。脊椎すべり症や椎間板障害などの変性疾患が一般的になるにつれ、脊椎固定術の件数は増加の一途をたどっています。PEEKやチタンなどの先端材料から作られた新しい固定インプラントの設計は、人体との適合性、強度の向上、周囲の骨組織とのより良い統合により、現在ではより一般的に使用されています。これらの特性は、患者の長期的な予後を向上させ、市場におけるこのセグメントの優位性を確固たるものにしています。

チタンベース脊椎インプラントのセグメントは、2034年までに65億米ドルを生み出すと予想されています。チタンは、その高い生体適合性、耐食性、構造的耐久性により、脊髄手術に好まれる材料であり続けています。チタンは身体とシームレスに一体化し、免疫拒絶反応のリスクを最小化すると同時に、体液の多い環境でも弾力性を維持します。チタンインプラントは強靭でありながら軽量であり、回復期および回復後の患者の快適性とパフォーマンスにとって不可欠です。大きな機械的負荷に耐えるため、頸椎と腰椎の両方の手術における体間ケージ、ロッド、プレートなどの用途に理想的です。長期にわたる安全性の記録は、最新の脊椎手術におけるその地位をさらに強固なものにしています。

米国の脊椎インプラントの2024年の市場規模は66億米ドルで、2025年から2034年にかけてCAGR 3.5%で成長すると予測されています。米国は、ジョンソン・エンド・ジョンソン、ストライカー、メドトロニック、ジマー・バイオメット、NuVasiveなどの大手メーカーの存在に支えられ、脊椎インプラントの生産において世界のリーダーであり続けています。これらの企業は技術革新の最前線にあり、手術精度と臨床転帰を向上させるロボット工学とスマートインプラントの開発に投資しています。国内各地に広範な研究開発ネットワークと製造施設を持つこれらの企業は、製品の展開と採用を加速し、世界の脊髄医療情勢における同国の影響力を強化しています。

世界の脊椎インプラント市場を形成する主要企業には、Spineart、Ulrich、Orthofix Holdings、B. Braun、CENTINEL SPINE、INTEGRA、Seaspine、RTI Surgical、Zimmer Biomet、Stryker、Johnson &Johnson、Globus Medical、Alphatec Spine、Medtronic、NuVasiveなどがあります。脊椎インプラント業界の各社は、市場の足跡を拡大するため、インプラントの機能性と低侵襲手技との適合性を高める戦略的研究開発投資に注力しています。また、合併、提携、買収を通じた世界展開を積極的に推進し、新たな顧客基盤の獲得と販売チャネルの強化を図っています。ロボット工学とデジタルナビゲーションの製品ポートフォリオへの統合は、手術精度と患者満足度の向上に役立っています。各社はまた、製品の性能を検証し、規制当局の承認を迅速に取得し、世界中のヘルスケアプロバイダーからの信頼を強化するために、臨床機関と協力しています。

目次

第1章 分析手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 脊椎疾患の有病率の上昇

- 低侵襲手術の需要増加

- 技術的進歩

- 先進国における有利な償還政策

- 業界の潜在的リスクと課題

- 脊椎インプラントと手術の高額な費用

- 先進国における厳格な規制シナリオ

- 市場機会

- 脊椎手術におけるAIとロボットの統合

- 外来診療と通院診療への注目が高まる

- 促進要因

- 成長可能性分析

- 規制情勢

- 米国

- 欧州

- 技術情勢

- 償還シナリオ

- ポーター分析

- PESTEL分析

- 価格分析

- GAP分析

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 地域別

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

- 主な発展

- 企業合併・買収 (M&A)

- 事業提携・協力

- 新製品の発売

- 拡張計画

第5章 市場の推計・予測:製品種類別(2021~2034年)

- 主要動向

- 脊椎固定インプラント

- 椎弓根スクリュー

- 椎間体固定装置(IBFD)

- ロッド

- プレート

- ケージ

- その他の脊椎固定インプラント

- 動的安定化装置

- 人工椎間板

- 頸部

- 腰椎

- その他の製品種類

第6章 市場の推計・予測:材料別(2021~2034年)

- 主要動向

- チタン

- コバルトクロム

- ステンレス鋼

- ポリエーテルエーテルケトン(PEEK)

- その他の材料

第7章 市場の推計・予測:手術の種類別(2021~2034年)

- 主要動向

- 開腹手術

- 低侵襲手術

第8章 市場の推計・予測:適応症別(2021~2034年)

- 主要動向

- 変性椎間板疾患

- 脊椎変形

- 脊椎外傷

- 骨折

- その他の適応症

第9章 市場の推計・予測:最終用途別(2021~2034年)

- 主要動向

- 病院

- 外来手術センター

- その他の用途

第10章 市場の推計・予測:地域別(2021~2034年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Alphatec Spine

- B. Braun

- CENTINEL SPINE

- Globus Medical

- INTEGRA

- Johnson &Johnson

- Medtronic

- NuVasive

- Orthofix Holdings

- RTI Surgical

- Seaspine

- Spineart

- Stryker

- Ulrich

- Zimmer Biomet

The Global Spinal Implants Market was valued at USD 11.8 billion in 2024 and is estimated to grow at a CAGR of 3.9% to reach USD 16.9 billion by 2034. The growing demand is fueled by a rising aging population, an increase in spinal disorders, a shift toward minimally invasive procedures, and technological advancements in implant materials and surgical techniques. As spinal conditions like spinal stenosis, degenerative disc disease, and herniated discs become more prevalent, especially among older individuals, the need for surgical intervention and spinal stabilization solutions continues to climb.

Obesity and sedentary lifestyles further contribute to spinal degeneration. As a result, more patients are opting for surgical correction, especially with new solutions offering reduced pain and faster recovery. The introduction of robotic systems and navigation tools in spinal surgeries has not only enhanced procedural precision but also minimized complication rates, encouraging greater use of advanced implants. Many device manufacturers are responding by designing implants tailored for minimally invasive techniques, driving broader clinical adoption globally as costs gradually decline and accessibility improves.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.8 Billion |

| Forecast Value | $16.9 Billion |

| CAGR | 3.9% |

The spinal fusion implants segment is projected to witness strong growth at a CAGR of 4.3%, reaching USD 9.3 billion by 2034. The widespread use of these devices stems from their critical role in treating spinal instability caused by degeneration or trauma. As degenerative conditions such as spondylolisthesis and disc disorders become more common, the volume of spinal fusion procedures continues to grow. New fusion implant designs made from advanced materials such as PEEK and titanium are now more commonly used due to their compatibility with the human body, enhanced strength, and better integration with surrounding bone tissue. These properties increase long-term patient outcomes, helping to solidify the segment's dominance in the market.

Titanium-based spinal implants segment is expected to generate USD 6.5 billion by 2034. Titanium remains the preferred material in spinal surgeries due to its high biocompatibility, corrosion resistance, and structural durability. It integrates seamlessly with the body, minimizing the risk of immune rejection while maintaining resilience in fluid-rich environments. Titanium implants are strong yet lightweight, which is essential for patient comfort and performance during and after the recovery phase. They withstand significant mechanical loads, making them ideal for applications such as interbody cages, rods, and plates in both cervical and lumbar spine procedures. Their long-term safety record further reinforces their position in modern spinal procedures.

U.S. Spinal Implants Market was valued at USD 6.6 billion in 2024 and is expected to grow at a CAGR of 3.5% between 2025 and 2034. The U.S. remains a global leader in spinal implant production, supported by the presence of major manufacturers including Johnson & Johnson, Stryker, Medtronic, Zimmer Biomet, and NuVasive. These companies are at the forefront of innovation, investing in the development of robotics and smart implants that enhance surgical precision and clinical outcomes. With extensive R&D networks and manufacturing facilities across the country, these firms accelerate product deployment and adoption, strengthening the country's influence in the global spinal care landscape.

Key players shaping the Global Spinal Implants Market include Spineart, Ulrich, Orthofix Holdings, B. Braun, CENTINEL SPINE, INTEGRA, Seaspine, RTI Surgical, Zimmer Biomet, Stryker, Johnson & Johnson, Globus Medical, Alphatec Spine, Medtronic, and NuVasive. To expand their market footprint, companies within the spinal implants industry are focusing on strategic R&D investments to enhance implant functionality and compatibility with minimally invasive techniques. They are actively pursuing global expansion through mergers, partnerships, and acquisitions to reach new customer bases and reinforce distribution channels. Integration of robotics and digital navigation into their product portfolios is helping them improve surgical accuracy and patient satisfaction. Firms are also collaborating with clinical institutions to validate product performance, obtain faster regulatory approvals, and strengthen their credibility among healthcare providers worldwide.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Material trends

- 2.2.4 Surgery type trends

- 2.2.5 Indication trends

- 2.2.6 End use trends

- 2.3 CXO Perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of spinal diseases

- 3.2.1.2 Increasing demand for minimally invasive procedures

- 3.2.1.3 Technological advancements

- 3.2.1.4 Favorable reimbursement policies in developed countries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of spinal implants and surgeries

- 3.2.2.2 Stringent regulatory scenario in developed countries

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI and robotics in spine surgery

- 3.2.3.2 Growing focus on outpatient and ambulatory settings

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis

- 3.10 GAP analysis

- 3.11 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 By region

- 4.3.1.1 North America

- 4.3.1.2 Europe

- 4.3.1.3 Asia Pacific

- 4.3.1 By region

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Spinal fusion implants

- 5.2.1 Pedicle screws

- 5.2.2 Intervertebral body fusion device (IBFD)

- 5.2.3 Rods

- 5.2.4 Plates

- 5.2.5 Cages

- 5.2.6 Other spinal fusion implants

- 5.3 Dynamic stabilization devices

- 5.4 Artificial discs

- 5.4.1 Cervical

- 5.4.2 Lumbar

- 5.5 Other product types

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Titanium

- 6.3 Cobalt chrome

- 6.4 Stainless steel

- 6.5 Polyetheretherketone (PEEK)

- 6.6 Other materials

Chapter 7 Market Estimates and Forecast, By Surgery Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Open surgery

- 7.3 Minimally invasive surgery

Chapter 8 Market Estimates and Forecast, By Indication, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Degenerative disc disease

- 8.3 Spinal deformities

- 8.4 Spinal trauma

- 8.5 Fractures

- 8.6 Other indications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Alphatec Spine

- 11.2 B. Braun

- 11.3 CENTINEL SPINE

- 11.4 Globus Medical

- 11.5 INTEGRA

- 11.6 Johnson & Johnson

- 11.7 Medtronic

- 11.8 NuVasive

- 11.9 Orthofix Holdings

- 11.10 RTI Surgical

- 11.11 Seaspine

- 11.12 Spineart

- 11.13 Stryker

- 11.14 Ulrich

- 11.15 Zimmer Biomet