馬用医療市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年)

Equine Healthcare Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755349

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

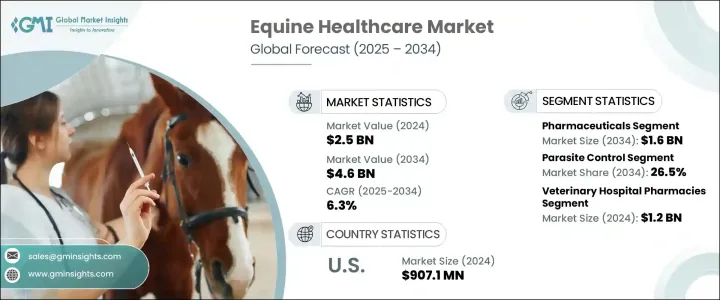

世界の馬用医療市場は、2024年には25億米ドルと評価され、CAGR 6.3%で成長し、2034年には46億米ドルに達すると推定されています。

この市場の拡大は、主に動物医療支出の増加と、馬主、ブリーダー、獣医師の間で予防ケアと早期診断が重視されるようになったことに起因しています。このような意識の高まりにより、馬用医療製品やサービスに対する需要が大幅に増加しています。筋骨格系の障害や馬の感染症の増加も、高度な診断や治療の導入を後押ししています。

さらに、再生医療、標的治療、デジタルヘルスモニタリングツールなど、革新的な治療法の開発に継続的に注力していることも市場の追い風となっています。また、馬のスポーツやレース分野への投資の拡大も需要を後押ししています。馬関連疾患の発生が増加するにつれ、より効果的で利用しやすい治療オプションの必要性も高まっています。獣医学的インフラの強化や、製薬会社による独自の馬用医薬品への投資の増加も、成長加速に重要な役割を果たしています。馬の分野におけるペットの人間化の動向は、技術の進歩や馬に合わせた最新の医療ソリューションに対する持続的な需要にさらに貢献しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025~2034年 |

| 当初の市場規模 | 25億米ドル |

| 市場規模予測 | 46億米ドル |

| CAGR | 6.3% |

馬用医療とは、様々な症状の予防、診断、治療を通じて馬の健康を維持・改善するためのホリスティックなアプローチを指します。同市場は、獣医師、製薬会社、馬専門クリニックが提供する医療・診断サービスを幅広くカバーしています。これらのソリューションは、繁殖、レクリエーション、スポーツに使用される馬の全体的な健康と最高のパフォーマンスを保証します。

製品カテゴリー別では、世界の馬用医療市場はワクチン、医薬品、診断薬、医療用飼料添加物、その他に区分されます。このうち、医薬品分野は2024年に8億1,790万米ドルの収益シェアで市場をリードし、2034年にはCAGR 6.6%の成長率で16億米ドルに達すると予測されています。このセグメントには、抗感染症薬、寄生虫駆除薬、抗炎症薬、鎮痛薬、その他の医薬品治療などの製品が含まれます。このセグメントの優位性は、呼吸器疾患、筋骨格系疾患、感染症などの一般的な馬の疾患を対象とした高度な治療に対する需要の高まりによる。さらに、レクリエーション乗馬や競合イベントへの関与の増加は、優れた健康管理プロトコルの必要性を強調しています。

市場は適応症別に、寄生虫駆除、筋骨格系疾患、馬インフルエンザ、馬脳脊髄炎、馬ヘルペス、ウェストナイルウイルス、破傷風、その他に分類されます。寄生虫駆除分野は2024年に25.1%の市場シェアを獲得し、2034年には26.5%に達すると予測されています。この分野は、馬の健康とパフォーマンスを低下させる有害な寄生虫を管理する必要性が広く浸透しているため、極めて重要な役割を果たし続けています。内部および外部の寄生虫は、胃腸障害、被毛の劣化、体重の問題を引き起こす可能性があります。予防寄生虫管理に対する馬の世話をしている人や獣医師の意識の高まりが、駆虫薬やその他の駆除手段の需要を押し上げています。気候パターンの変化や牧草地への通年のアクセスにより、寄生虫への曝露が増加しており、革新的で効果的な治療薬へのニーズが高まっています。

流通チャネル別では、市場は動物病院薬局、eコマース、その他に区分されます。動物病院薬局は2024年に12億米ドルの評価額で市場を独占し、2034年までリードを維持し、CAGR 6.7%で成長すると予測されています。これらの薬局は、専門的な相談、治療、多種多様な馬用医薬品の入手を含む包括的なサービスを提供しているため、好まれています。診断と治療に対する総合的なアプローチにより、馬主にとって重要なアクセスポイントとなっています。

地域別では、北米は予測期間中CAGR 6.1%で成長すると予測されています。同地域の馬産業は堅調で、動物福祉への関心が高く、高度な獣医学インフラが整っているため、馬用医療分野のリーダーとして位置づけられています。馬の飼育数が多く、馬術競技への参加が盛んであることも、同地域の専門的医療への需要を後押ししています。

世界の馬用医療市場を形成している主要企業には、Heska Corporation、Chanelle Pharma、Ceva、Zoetis、Esaote、Alltech、Vetoquinol、Cargill、Dechra Pharmaceuticals、IDEXX Laboratories、Bentoii、Equal Pharma、Merck、Hallmarq Veterinary、Boehringer Ingelheim、Intacinなどがあります。これらの企業は、製品革新や戦略的提携に積極的に取り組み、馬業界の進化するニーズに応えるべく製品ポートフォリオを拡大しています。

目次

第1章 分析手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 馬術スポーツとレクリエーション活動の増加

- 獣医学における技術の進歩

- 政府や公的機関による動物ケアへの支援の増加

- 業界の潜在的リスクと課題

- 熟練した獣医専門家の不足

- 促進要因

- 成長可能性分析

- テクノロジーの情勢

- パイプライン分析:製薬会社別

- 規制情勢

- 将来の市場動向

- ギャップ分析

- ポーターのファイブフォース分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場の推計・予測:製品別(2021~2034年)

- 主要動向

- ワクチン

- 医薬品

- 寄生虫駆除剤

- 抗感染性

- 抗炎症薬・鎮痛薬

- その他の医薬品

- 医療用飼料添加物

- 診断薬

- その他の製品

第6章 市場の推計・予測:適応症別(2021~2034年)

- 主要動向

- 筋骨格系障害

- 寄生虫駆除

- 馬ヘルペス

- 馬脳脊髄炎

- 馬インフルエンザ

- 破傷風

- ウエストナイルウイルス

- その他の適応症

第7章 市場の推計・予測:流通チャネル別(2021~2034年)

- 主要動向

- 動物病院薬局

- eコマース

- その他の流通チャネル

第8章 市場の推計・予測:地域別(2021~2034年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Alltech

- Bentoii

- Boehringer Ingelheim

- Cargill

- Ceva

- Chanelle Pharma

- Dechra Pharmaceuticals

- Equal pharma

- Esaote

- Hallmarq Veterinary

- Heska Corporation

- IDEXX Laboratories

- Intacin

- Merck

- Vetoquinol

- Zoetis

目次

The Global Equine Healthcare Market was valued at USD 2.5 billion in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 4.6 billion by 2034. The expansion of this market is primarily attributed to rising animal healthcare spending and an increasing emphasis on preventive care and early diagnosis among horse owners, breeders, and veterinarians. This heightened awareness has significantly increased the demand for equine healthcare products and services. The rise in musculoskeletal disorders and equine infectious diseases has also driven the adoption of advanced diagnostics and treatments.

Furthermore, the market is benefiting from a continuous focus on developing innovative therapeutics such as regenerative medicines, targeted therapies, and digital health monitoring tools. Demand is also being propelled by growing investments in the equine sports and racing sectors. As the occurrence of equine-related diseases increases, so does the need for more effective and accessible treatment options. The strengthening of veterinary infrastructure and rising investments from pharmaceutical companies in proprietary equine medications are also playing a critical role in accelerating growth. The trend of pet humanization within the equine segment is further contributing to technological advancements and sustained demand for modern healthcare solutions tailored for horses.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 Billion |

| Forecast Value | $4.6 Billion |

| CAGR | 6.3% |

Equine healthcare refers to the holistic approach to maintaining and improving horse health through prevention, diagnosis, and treatment of various conditions. The market covers a wide range of medical and diagnostic offerings delivered by veterinarians, pharmaceutical firms, and dedicated equine clinics. These solutions ensure the overall wellness and peak performance of horses used in breeding, recreation, and sports.

In terms of product categories, the global equine healthcare market is segmented into vaccines, pharmaceuticals, diagnostics, medicinal feed additives, and others. Among these, the pharmaceuticals segment led the market in 2024 with a revenue share of USD 817.9 million and is expected to reach USD 1.6 billion by 2034, growing at a CAGR of 6.6%. This segment includes products such as anti-infectives, parasiticides, anti-inflammatories, analgesics, and other pharmaceutical treatments. The segment's dominance is driven by rising demand for advanced therapies targeting common equine conditions like respiratory, musculoskeletal, and infectious diseases. Moreover, the increased involvement in recreational riding and competitive events underscores the need for superior health management protocols.

The market by indication is categorized into parasite control, musculoskeletal disorders, equine influenza, equine encephalomyelitis, equine herpes, West Nile virus, tetanus, and others. The parasite control segment captured a 25.1% market share in 2024 and is forecasted to reach 26.5% by 2034. This segment continues to play a pivotal role due to the widespread need to manage harmful parasites that compromise a horse's health and performance. Internal and external parasites can trigger gastrointestinal distress, coat degradation, and weight issues. Rising awareness among horse caretakers and veterinarians around preventive parasite management is pushing the demand for anthelmintics and other control measures. Changing climatic patterns and year-round access to pasturelands have amplified exposure to parasites, boosting the need for innovative and effective therapeutics.

By distribution channel, the market is segmented into veterinary hospital pharmacies, e-commerce, and others. Veterinary hospital pharmacies dominated the market in 2024 with a valuation of USD 1.2 billion and are projected to maintain their lead through 2034, growing at a CAGR of 6.7%. These pharmacies are preferred due to their comprehensive services, which include professional consultation, treatment, and access to a wide variety of equine medications. Their integrated approach to diagnosis and therapy continues to make them a critical access point for horse owners.

Regionally, North America is projected to grow at a CAGR of 6.1% over the forecast period. The region's robust equine industry, heightened focus on animal welfare, and advanced veterinary infrastructure have positioned it as a leader in the equine healthcare space. A large horse population and widespread participation in equine activities further support the demand for specialized healthcare offerings across the region.

Key players shaping the global equine healthcare market include Heska Corporation, Chanelle Pharma, Ceva, Zoetis, Esaote, Alltech, Vetoquinol, Cargill, Dechra Pharmaceuticals, IDEXX Laboratories, Bentoii, Equal Pharma, Merck, Hallmarq Veterinary, Boehringer Ingelheim, and Intacin. These companies are actively involved in product innovation, strategic collaborations, and expanding their product portfolios to meet the evolving needs of the equine industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing equine sports and recreational activities

- 3.2.1.2 Technological advancements in veterinary medicine

- 3.2.1.3 Increasing support offered by government and public organizations for animal care

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled veterinary professionals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Pipeline analysis, by pharmaceuticals

- 3.6 Regulatory landscape

- 3.7 Future market trends

- 3.8 Gap Analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Vaccines

- 5.3 Pharmaceuticals

- 5.3.1 Parasiticides

- 5.3.2 Anti-infective

- 5.3.3 Anti-inflammatory and analgesics

- 5.3.4 Other pharmaceutical products

- 5.4 Medicinal feed additives

- 5.5 Diagnostics

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Indication, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Musculoskeletal disorders

- 6.3 Parasite control

- 6.4 Equine herpes

- 6.5 Equine encephalomyelitis

- 6.6 Equine influenza

- 6.7 Tetanus

- 6.8 West Nile Virus

- 6.9 Other indications

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Veterinary hospital pharmacies

- 7.3 E-commerce

- 7.4 Other distribution channels

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alltech

- 9.2 Bentoii

- 9.3 Boehringer Ingelheim

- 9.4 Cargill

- 9.5 Ceva

- 9.6 Chanelle Pharma

- 9.7 Dechra Pharmaceuticals

- 9.8 Equal pharma

- 9.9 Esaote

- 9.10 Hallmarq Veterinary

- 9.11 Heska Corporation

- 9.12 IDEXX Laboratories

- 9.13 Intacin

- 9.14 Merck

- 9.15 Vetoquinol

- 9.16 Zoetis

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日