|

市場調査レポート

商品コード

1755332

ファンコイルユニット市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年)Fan Coil Unit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ファンコイルユニット市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年) |

|

出版日: 2025年05月29日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

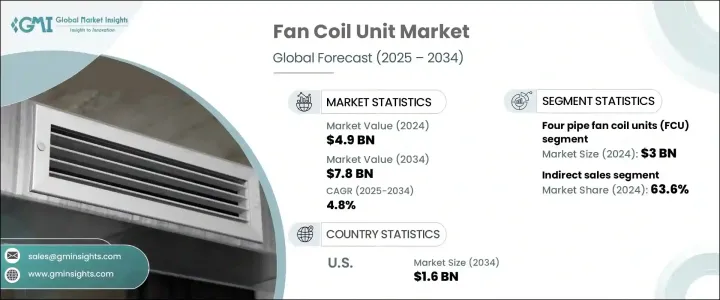

世界のファンコイルユニット (FCU) 市場は、2024年には49億米ドルと評価され、CAGR 4.8%で成長し、2034年には78億米ドルに達すると推定されています。

この成長の主な要因は、室内空気環境の重要性に対する意識の高まりです。人々が家庭やオフィス、その他の閉ざされた環境の中で多くの時間を過ごすようになり、大気汚染や湿度管理にまつわる懸念が顕著になっています。消費者は今、空気を冷やしたり暖めたりするだけでなく、より清潔で健康的な室内環境を確保する空調ソリューションを求めています。高性能の空気ろ過機能と湿度調整機能を備えたFCUは、住宅と商業施設の両方の購入者からますます支持されています。オフィス、学校、ヘルスケアなどの環境では、室内空気の質の向上がウェルネスや生産性の向上と密接に結びついており、これが採用をさらに後押ししています。

さらに、老朽化したインフラを現代のエネルギー基準に適合させるために近代化する動向は、FCUのようなエネルギー効率の高いHVACソリューションに対する強い需要を生み出しています。ビルディングは依然として世界的にエネルギー使用量の最も大きな要因の一つであるため、効率的な空調制御システムを統合することは、エネルギーフットプリントを削減するために不可欠となっています。最新のFCU、特にスマートテクノロジーと統合されたFCUは、強化された制御と自動化機能を提供するため、勢いを増しています。遠隔監視、占有率ベースの設定、ビル管理システムとの統合により、FCUは施設管理者やビル所有者にとってより魅力的なものとなっています。これらのインテリジェント・システムは、エネルギー使用量をより効果的に調整し、運用コストを最小限に抑えながらパフォーマンスを最適化するのに役立ちます。また、リアルタイムの洞察により、積極的なメンテナンスと性能調整が可能になり、長期的な効率向上につながります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025~2034年 |

| 当初の市場規模 | 49億米ドル |

| 市場規模予測 | 78億米ドル |

| CAGR | 4.8% |

ファンコイルユニット市場は、構成別に2本配管式FCUと4本配管式FCUに区分されます。このうち、4本配管式FCUは2024年に約30億米ドルと最大の売上シェアを占め、2025年から2034年にかけてCAGR 4.9%で成長すると予測されています。4本配管式システムは、暖房と冷房の両方を同時に供給できるため、異なるゾーンにまたがって多様な空調ニーズがある建物では機能的に有利です。この柔軟性により、ビル管理者は特定のスペースに合わせた正確な室内温度を維持することができます。これらのシステムは、複数の部屋や部署にわたって一貫した快適性を必要とする大規模な商業施設や施設に特に適しています。初期設置費用と設備コストは比較的高いですが、4本配管式FCUの優れた熱制御と適応性により、先進的なHVAC設計において好ましい選択肢となっています。

販売チャネル別に評価すると、市場は直接販売と間接販売に分けられます。2024年時点では、間接販売分野が全体の約63.6%を占め、圧倒的なシェアを占めており、予測期間中のCAGRは4.9%と予測されています。このセグメントの強みは、ディーラー、ディストリビューター、小売パートナーなどの仲介業者の広範なネットワークにあります。これらのチャネルは、メーカーが多様な地域や顧客基盤にリーチを広げるのに役立っています。地域の建設業者、建築業者、エンドユーザーとの確立された関係は、販売サイクルをより効率的で迅速なものにしています。さらに、販売代理店が提供する販売後のサポート、設置、メンテナンスなどの付加価値サービスは、このチャネルの魅力をさらに高めています。間接販売はまた、地域に特化したマーケティング戦略や深い市場知識からも恩恵を受け、地域市場におけるブランドの認知度や顧客の信頼を高めるのに役立っています。

米国のファンコイルユニット市場は、2024年に金額ベースで10億米ドルを突破し、2034年には16億米ドルに達すると予測されています。エネルギー効率の高い持続可能な建築システムへのシフトが進んでいることが、この成長の主な要因です。FCUは局所的な温度制御を可能にするため、集中型HVACシステムに比べて大幅なエネルギー節約に貢献し、グリーンビルディングの設計に組み込まれるケースが増えています。FCUは室内レベルで温度制御を最適化することで、エネルギーの浪費を最小限に抑え、持続可能なビルづくりを推進する全国的な目標に合致しています。このため、FCUは環境に配慮したインフラ整備の推進に不可欠な要素となっています。

世界のFCU市場は依然として非常に断片化されており、多数の地域企業が国際レベルで事業を展開しています。これらの企業を合わせると、市場全体の約10%から15%のシェアを占めています。現地の企業は、地域の規制や建築基準法の要件を満たすように製品を調整し、特定の地域の需要に応えることが多いです。また、地域の嗜好に合わせたカスタマイズ・ソリューションも提供しています。他方、国際的ブランドは、大規模生産、確立された国際的ネットワーク、市場での高い信頼性から、複数の地域で競争力を維持することができます。

目次

第1章 分析手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 販売代理店

- サプライヤーの情勢

- 利益率分析

- 技術概要

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 室内空気質に対する意識の高まり

- 都市化の進展

- 技術的進歩

- 業界の潜在的リスクと課題

- 初期費用が高め

- 規制とコンプライアンスの問題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 ファンコイルユニット市場の推計・予測:構成別(2021~2032年)

- 主要動向

- 2本配管式ファンコイルユニット

- 4本配管式ファンコイルユニット

第6章 ファンコイルユニット市場の推計・予測:方向別(2021~2032年)

- 主要動向

- 横型

- 壁掛け式

- ダクトブロワー型

- 天井カセット型

- 天井埋込型

- 縦型(床置型)

第7章 ファンコイルユニット市場の推計・予測:空気流量別(2021~2032年)

- 主要動向

- 500 m³/h以下

- 500 m³/h~1000 m³/h

- 1000 m³/h~1500 m³/h

- 1500 m³/h~2000 m³/h

- 2000 m³/h以上

第8章 ファンコイルユニット市場の推計・予測:最終用途別(2021~2032年)

- 主要動向

- 住宅用

- 商業用

- オフィススペース

- ホテル

- レストラン

- 病院

- 小売り

- スーパーマーケット

- デパート

- ブランドアウトレットストア

- 物流(倉庫)

- その他(製造業など)

- 産業

第9章 ファンコイルユニット市場の推計・予測:流通チャネル別(2021~2032年)

- 主要動向

- 直接販売

- 間接販売

第10章 ファンコイルユニット市場の推計・予測:地域別(2021~2032年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東・アフリカ

第11章 企業プロファイル

- Aermec

- Carrier Global Corporation

- Daikin Industries

- Dunham-Bush

- Emerson Electric

- Fujitsu General Limited

- Gree Electric Appliances

- Honeywell International

- Johnson Controls International

- Lennox International

- LG Electronics

- Mitsubishi Electric Corporation

- Samsung Electronics

- Trane Technologies

- TROX

The Global Fan Coil Unit Market was valued at USD 4.9 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 7.8 billion by 2034. This growth is primarily fueled by rising awareness about the importance of indoor air quality. As people spend a large portion of their time inside homes, offices, and other enclosed environments, concerns around air pollution and humidity control have become more prominent. Consumers are now looking for air conditioning solutions that not only cool or heat the air but also ensure cleaner, healthier indoor environments. FCUs equipped with high-performance air filtration and humidity regulation features are increasingly favored by both residential and commercial buyers. In environments such as offices, schools, and healthcare settings, better indoor air quality is closely linked with improved wellness and productivity, which further drives adoption.

Additionally, the trend of modernizing aging infrastructure to meet contemporary energy standards has created a strong demand for energy-efficient HVAC solutions like FCUs. As buildings remain one of the highest contributors to energy use globally, integrating efficient climate control systems has become essential for reducing energy footprints. Modern FCUs, particularly those integrated with smart technology, are gaining momentum as they offer enhanced control and automation features. Remote monitoring, occupancy-based settings, and integration with building management systems are making FCUs more attractive to facility managers and building owners. These intelligent systems help regulate energy usage more effectively, optimizing performance while minimizing operational expenses. They also offer real-time insights that allow for proactive maintenance and performance tuning, leading to long-term efficiency gains.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.9 Billion |

| Forecast Value | $7.8 Billion |

| CAGR | 4.8% |

By configuration, the fan coil unit market is segmented into two-pipe and four-pipe FCUs. Among these, the four-pipe segment accounted for the largest revenue share, valued at approximately USD 3 billion in 2024, and is expected to grow at a CAGR of 4.9% from 2025 to 2034. The ability of four-pipe systems to deliver both heating and cooling at the same time gives them a functional advantage in buildings with varied climate control needs across different zones. This flexibility enables building operators to maintain precise indoor temperatures tailored to specific spaces. These systems are particularly suitable for large-scale commercial or institutional facilities that require consistent comfort across multiple rooms or departments. Although the initial installation and equipment costs are relatively high, the superior thermal control and adaptability of four-pipe FCUs make them a preferred choice in advanced HVAC design.

When assessed by distribution channel, the market is divided into direct and indirect sales. The indirect sales segment held the dominant share in 2024, contributing roughly 63.6% of the overall revenue, and is forecasted to rise at a CAGR of 4.9% over the forecast period. The strength of this segment lies in its widespread network of intermediaries, including dealers, distributors, and retail partners. These channels help manufacturers expand their reach into diverse geographic locations and customer bases. Established relationships with local contractors, builders, and end-users make the sales cycle more efficient and responsive. Additionally, value-added services such as post-sale support, installation, and maintenance offered by distributors further enhance the attractiveness of this channel. Indirect sales also benefit from localized marketing strategies and in-depth market knowledge, which help boost brand visibility and customer trust in regional markets.

In the United States, the fan coil unit market surpassed USD 1 billion in value in 2024 and is projected to hit USD 1.6 billion by 2034. The increasing shift toward energy-efficient and sustainable building systems is a major factor behind this growth. FCUs are increasingly being incorporated into green building designs as they offer localized climate control, which contributes to significant energy savings compared to centralized HVAC systems. By optimizing temperature control at the room level, FCUs minimize energy waste and align with nationwide goals to promote sustainable building practices. This has made FCUs a vital component in the drive toward environmentally conscious infrastructure upgrades.

The global FCU market remains highly fragmented, with numerous regional players operating on an international level. Collectively, these companies account for approximately 10% to 15% of the total market share. Local firms often cater to specific regional demands, tailoring their offerings to meet local regulatory and building code requirements. They also provide customized solutions that appeal to regional preferences. On the other hand, global brands benefit from large-scale production, established international networks, and strong market credibility, enabling them to maintain competitiveness across multiple regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technological overview

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increased awareness of indoor air quality

- 3.7.1.2 Rising urbanization

- 3.7.1.3 Technological advancements

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High initial costs

- 3.7.2.2 Regulatory and compliance issues

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Fan Coil Unit Market Estimates & Forecast, By Configuration, 2021 - 2032 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Two pipe fan coil unit

- 5.3 Four pipe fan coil unit

Chapter 6 Fan Coil Unit Market Estimates & Forecast, By Orientation, 2021 - 2032 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Horizontal

- 6.2.1 Wall mounted

- 6.2.2 Ducted blower type

- 6.2.3 Ceiling cassette type

- 6.2.4 Ceiling concealed type

- 6.3 Vertical (floor mounted)

Chapter 7 Fan Coil Unit Market Estimates & Forecast, By Air Flow, 2021 - 2032 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Below 500 m³/h

- 7.3 500 m³/h - 1000 m³/h

- 7.4 1000 m³/h - 1500 m³/h

- 7.5 1500 m³/h - 2000 m³/h

- 7.6 Above 2000 m³/h

Chapter 8 Fan Coil Unit Market Estimates & Forecast, By End Use, 2021 - 2032 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Office spaces

- 8.3.2 Hotels

- 8.3.3 Restaurants

- 8.3.4 Hospitals

- 8.3.5 Retail

- 8.3.5.1 Supermarkets

- 8.3.5.2 Departmental stores

- 8.3.5.3 Brand outlet stores

- 8.3.6 Logistics (warehouse)

- 8.3.7 Others (manufacturing, etc.)

- 8.4 Industrial

Chapter 9 Fan Coil Unit Market Estimates & Forecast, By Distribution Channel, 2021 - 2032 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Fan Coil Unit Market Estimates & Forecast, By Region, 2021 - 2032 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Rest of Latin America

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Rest of MEA

Chapter 11 Company Profiles

- 11.1 Aermec

- 11.2 Carrier Global Corporation

- 11.3 Daikin Industries

- 11.4 Dunham-Bush

- 11.5 Emerson Electric

- 11.6 Fujitsu General Limited

- 11.7 Gree Electric Appliances

- 11.8 Honeywell International

- 11.9 Johnson Controls International

- 11.10 Lennox International

- 11.11 LG Electronics

- 11.12 Mitsubishi Electric Corporation

- 11.13 Samsung Electronics

- 11.14 Trane Technologies

- 11.15 TROX