防衛エレクトロニクスの陳腐化市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Defense Electronics Obsolescence Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755312

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

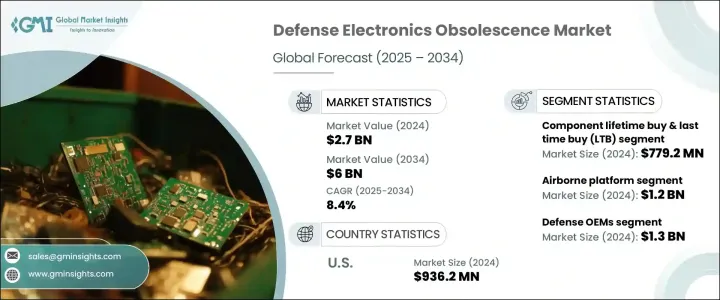

防衛エレクトロニクスの陳腐化の世界市場規模は、2024年には27億米ドルとなり、世界の防衛予算の増加、デジタルツイン技術と予測分析の利用の増加により、CAGR 8.4%で成長し、2034年には60億米ドルに達すると予測されています。

軍備が近代化を続ける一方で、長く使用されるプラットフォームに大きく依存するようになり、電子部品が旧式化した老朽化システムをサポートする必要性が重要になっています。持続可能性、システムのアップグレード、コンポーネントの互換性に向けた取り組みが強化され、ライフサイクル管理と陳腐化緩和ソリューションに対する需要が高まっています。これと並行して、調達改革と産業基盤の強靭性強化を目的とした戦略は、防衛部門全体で国内調達とデジタル変革を促しています。

長年にわたり、構造的な近代化戦略とレガシーシステムの継続的な使用により、古い電子機器の保守とサポートへの注目が高まっています。積極的なライフサイクル管理を推進する政策は、電子部品の陳腐化を予測するための、より機敏で技術的に進んだアプローチにつながりました。プラットフォームの長寿命化が重視された結果、DMSMS(製造ソースの減少と材料不足)プログラムが強化されました。防衛プラットフォームは何十年も現役であり続けるため、短い部品寿命サイクルと長いシステム寿命のミスマッチにより、陳腐化管理が不可欠となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 27億米ドル |

| 予測金額 | 60億米ドル |

| CAGR | 8.4% |

コンポーネントのライフタイムおよびラストタイムバイ(LTB)セグメントは、2024年に7億7,920万米ドルと評価されました。これらの戦略は、特に商用オフザシェルフ(COTS)部品が防衛プラットフォーム全体で使用されているため、レガシーシステムのサポートを確保する必要性の高まりに対処するのに役立ちます。電子部品のライフサイクルが5~10年に制限されることが多い中、ライフタイムやラストタイム購入は、40年以上使用され続ける可能性のあるプラットフォームとのギャップを埋めるのに役立ちます。地政学的不確実性、輸出制限、半導体不足は、供給の途絶を避けるためにLTB戦略への依存を加速させています。

航空機プラットフォームセグメントは2024年に12億米ドルと評価されました。航空プラットフォームの長寿命化要求の高まりが、アビオニクス、レーダーシステム、電子戦(EW)アップグレードへの投資に拍車をかけています。新しい技術を既存のシステムに統合する際の互換性の課題が、フォームフィット機能交換やレガシーコンポーネントのエミュレーションの必要性を高めています。さらに、UAVと支援航空機は、手頃な価格で入手できるCOTS部品に依存しているため、早期に陳腐化しやすく、強力なアフターマーケット調達に依存しています。

米国の防衛エレクトロニクスの陳腐化市場規模は2024年に9億3,620万米ドルでした。防衛機関による予測分析とデジタルツインテクノロジーの急速な導入と並んで、維持プログラムおよび近代化イニシアティブへの投資が市場を押し上げています。

同市場の有力企業には、 Lynx, RTX, Thales Group, SMT Corp, Mercury Systems, Leonardo, Northrop Grumman, Boeing Defense, Teledyne Technologies, TT Electronics, Lockheed Martin, Saab RDS, L3Harris Technologies, Rheinmetall, AT Engine Controls, and Bae Systems.などがあります。市場の足場を固めるため、防衛エレクトロニクスの陳腐化市場はいくつかの重要な戦略を採用しています。その中には、政府との長期契約の確保や、コンポーネントの可用性を確保するための耐用年数や最終購入期間を重視することなどが含まれます。多くの企業は、陳腐化予測を改善するために、AIを活用した予測やデジタルツインなどのデジタルツールに多額の投資を行っています。海外調達先への依存度を下げるため、サプライチェーン全体での協力体制も強化されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 主要部品の価格変動

- サプライチェーンの再編

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界の対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 老朽化した軍事プラットフォーム

- 国防予算の増額

- エレクトロニクス技術の進歩

- 地政学的緊張と脅威の近代化

- デジタルツインと予測分析の導入拡大

- 業界の潜在的リスク&課題

- 限られた予測ツール

- 知的財産(IP)制限

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:ソリューションタイプ別、2021年~2034年

- 主要動向

- 陳腐化監視と予測

- コンポーネント生涯購入と最終購入(LTB)

- 再設計および改修ソリューション

- エミュレーションとシミュレーション

- 代替調達(アフターマーケット、ブローカー)

- ソフトウェアとファームウェアのアップデート

第6章 市場推計・予測:プラットフォーム別、2021年~2034年

- 主要動向

- 空軍

- 海軍

- 陸軍

- 空間

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 防衛OEM

- MROプロバイダー

- 政府および防衛機関

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- AT Engine Controls

- Bae Systems

- Boeing Defense

- L3Harris Technologies

- Leonardo

- Lockheed Martin

- Lynx

- Mercury Systems

- Northrop Grumman

- Rheinmetall

- RTX

- Saab RDS

- SMT Corp

- Teledyne Technologies

- Thales Group

- TT Electronics

目次

The Global Defense Electronics Obsolescence Market was valued at USD 2.7 billion in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 6 billion by 2034, driven by a rising global defense budget and the increasing use of digital twin technology and predictive analytics. As military forces continue modernizing while relying heavily on long-serving platforms, the need to support aging systems with obsolete electronic components has become critical. Efforts toward sustainability, system upgrades, and component compatibility have intensified, prompting demand for lifecycle management and obsolescence mitigation solutions. In parallel, procurement reforms and strategies aimed at reinforcing industrial base resilience are encouraging domestic sourcing and digital transformation across the defense sector.

Over the years, structural modernization strategies and the continued use of legacy systems have prompted increased focus on maintaining and supporting older electronics. Policies promoting proactive lifecycle management have led to a more agile and technologically advanced approach to forecasting electronic component obsolescence. The emphasis on platform longevity has resulted in robust DMSMS (Diminishing Manufacturing Sources and Material Shortages) programs. As defense platforms remain active for decades, the mismatch between short component life cycles and long system lifespans has made obsolescence management essential.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.7 Billion |

| Forecast Value | $6 Billion |

| CAGR | 8.4% |

The component lifetime and last-time buy (LTB) segment was valued at USD 779.2 million in 2024. These strategies help address the growing need to secure legacy system support, especially as commercial off-the-shelf (COTS) parts are used across defense platforms. With electronic component lifecycles often limited to 5-10 years, lifetime and last-time buys help bridge the gap with platforms that may remain in service for over four decades. Geopolitical uncertainties, restricted exports, and semiconductor shortages accelerate reliance on LTB strategies to avoid supply disruptions.

The airborne platform segment was valued at USD 1.2 billion in 2024. Increased demand for extended service life of air platforms has fueled investments in avionics, radar systems, and electronic warfare (EW) upgrades. Compatibility challenges with integrating newer technologies into existing systems have amplified the need for form-fit-function replacements and legacy component emulation. Additionally, UAVs and support aircraft depend on COTS parts for affordability, making them vulnerable to early obsolescence and dependent on strong aftermarket sourcing.

United States Defense Electronics Obsolescence Market generated USD 936.2 million in 2024 driven by an aging military fleet that requires constant support for outdated electronic systems. Investments in sustainment programs and modernization initiatives, alongside the rapid implementation of predictive analytics and digital twin technologies by defense agencies, are pushing the market forward.

The prominent players in the market include Lynx, RTX, Thales Group, SMT Corp, Mercury Systems, Leonardo, Northrop Grumman, Boeing Defense, Teledyne Technologies, TT Electronics, Lockheed Martin, Saab RDS, L3Harris Technologies, Rheinmetall, AT Engine Controls, and Bae Systems. To strengthen its market foothold, the Defense Electronics Obsolescence Market is adopting several key strategies. These include securing long-term government contracts and emphasizing lifetime and last-time buys to ensure component availability. Many are investing heavily in digital tools like AI-powered forecasting and digital twins to improve obsolescence prediction. Collaborations across supply chains are being strengthened to reduce dependency on foreign sources.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 industry ecosystem analysis

- 3.2 trump administration tariffs

- 3.2.1 impact on trade

- 3.2.1.1 trade volume disruptions

- 3.2.1.2 retaliatory measures

- 3.2.2 impact on the industry

- 3.2.2.1 supply-side impact

- 3.2.2.1.1 price volatility in key components

- 3.2.2.1.2 supply chain restructuring

- 3.2.2.1.3 production cost implications

- 3.2.2.2 demand-side impact (selling price)

- 3.2.2.2.1 price transmission to end markets

- 3.2.2.2.2 market share dynamics

- 3.2.2.2.3 consumer response patterns

- 3.2.2.1 supply-side impact

- 3.2.3 key companies impacted

- 3.2.4 strategic industry responses

- 3.2.4.1 supply chain reconfiguration

- 3.2.4.2 pricing and product strategies

- 3.2.4.3 policy engagement

- 3.2.5 outlook and future considerations

- 3.2.1 impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Aging military platforms

- 3.3.1.2 Increasing defense budgets

- 3.3.1.3 Technological advancement in electronics

- 3.3.1.4 Geopolitical tensions & threat modernization

- 3.3.1.5 Growing adoption of digital twin & predictive analytics

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Limited forecasting tools

- 3.3.2.2 Intellectual property (IP) restrictions

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Solution Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Obsolescence monitoring & forecasting

- 5.3 Component lifetime buy & last-time buy (LTB)

- 5.4 Redesign & retrofit solutions

- 5.5 Emulation & simulation

- 5.6 Alternative sourcing (aftermarket, brokers)

- 5.7 Software & firmware updates

Chapter 6 Market Estimates and Forecast, By Platform, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Airborne

- 6.3 Naval

- 6.4 Land

- 6.5 Space

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Defense OEMs

- 7.3 MRO providers

- 7.4 Government & defense agencies

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AT Engine Controls

- 9.2 Bae Systems

- 9.3 Boeing Defense

- 9.4 L3Harris Technologies

- 9.5 Leonardo

- 9.6 Lockheed Martin

- 9.7 Lynx

- 9.8 Mercury Systems

- 9.9 Northrop Grumman

- 9.10 Rheinmetall

- 9.11 RTX

- 9.12 Saab RDS

- 9.13 SMT Corp

- 9.14 Teledyne Technologies

- 9.15 Thales Group

- 9.16 TT Electronics

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日