|

市場調査レポート

商品コード

1755307

燃料電池UAVの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Fuel Cell UAV Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 燃料電池UAVの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月20日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

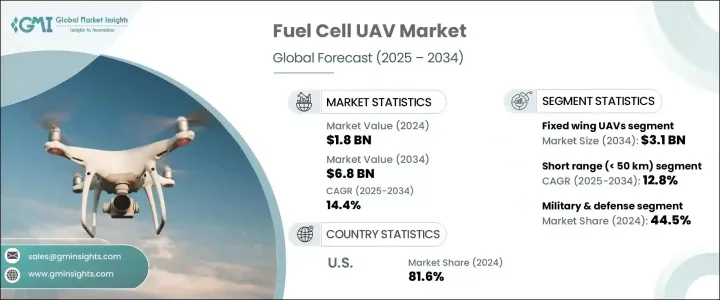

燃料電池UAVの世界市場は、2024年には18億米ドルと評価され、燃料電池技術に対する政府や機関の支援の増加や、監視・偵察システムの需要の高まりによって、CAGR 14.4%で成長し、2034年には68億米ドルに達すると予測されています。

しかし、市場は、中国からの輸入品に対する関税を含む米国政権の貿易政策による課題に直面し、水素貯蔵システム、燃料電池スタック、複合材料などの主要部品のコスト上昇につながりました。このため、世界のサプライチェーンが混乱し、価格設定に影響を与え、研究開発努力が鈍化しました。

このような状況にもかかわらず、燃料電池UAVセクターは、UAVが提供する数多くの利点に牽引され、大きな成長を続けています。優れた耐久性、騒音の低減、飛行時間の延長など、防衛、環境監視、災害対応などの重要な業務に特に適しています。頻繁な燃料補給を必要とせず、長時間にわたって静かに作動する能力は、燃料電池UAVを従来のものと差別化する重要な特徴になりつつあり、監視、偵察、緊急活動に不可欠なツールとして位置づけられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 18億米ドル |

| 予測金額 | 68億米ドル |

| CAGR | 14.4% |

燃料電池UAV技術の進歩に伴い、固定翼UAVが市場成長に大きく貢献することが予想され、2034年には31億米ドルに達すると予測されます。これらのUAVは、高い空力効率と大型の水素燃料電池システムを搭載できることが重要な長時間のミッションに特に適しています。燃料消費に妥協することなく長時間の飛行を維持できることから、国境監視、環境監視、防衛作戦など、広大な地域をカバーする必要がある用途では不可欠な存在となっています。これらのUAVをより長時間のミッションに投入できることは、特に耐久性が重要な作戦において戦略的な優位性をもたらします。

短距離用燃料電池UAV分野は、2034年までCAGR 12.8%で成長すると予測されています。短距離用燃料電池UAVは、従来のものと比べて迅速な燃料補給が可能で飛行時間が長いため、人気が高まっています。これらのUAVは、産業検査や公共安全業務など、限られた運用区域で持続的かつ信頼性の高い性能を必要とする用途に最適です。技術が向上するにつれて、UAVはより多用途で効率的なものとなり、さまざまな産業での採用が進んでいます。

ドイツ燃料電池UAV 2034年までCAGR13.7%で成長すると予測されるドイツ市場は、脱炭素化と持続可能性に焦点を当てた国家政策と、グリーンテクノロジーの技術革新を奨励するEU支援の研究プログラムに後押しされています。ドイツは、二酸化炭素排出量の削減と持続可能な航空ソリューションの推進に取り組んでおり、水素を動力源とするUAV技術への投資を促進しています。さらに、防衛請負業者、航空宇宙企業、学術機関の連携により、同国はグリーンUAV技術のリーダーとして位置づけられており、先進的 UAV研究開発の拠点となっています。

世界の燃料電池UAV産業における主な市場プレーヤーには、Hylium Industries、AeroVironment、FlightWave Aerospace、Doosan Mobility Innovation、ISS Group、Aurora Flight Sciences、MMCUAV、Elbit Systemsが含まれます。市場ポジションを強化するため、燃料電池UAVセクターの企業は、UAVの効率と耐久性を高める最先端の燃料電池技術の開発に注力しています。政府や官民パートナーシップと協力することで、資金や技術リソースを入手し、開発コストを削減することができます。研究開発を進めることで、これらの企業はイノベーションを推進し、水素を燃料とするUAVの普及に貢献しています。また、世界のカーボンニュートラルの目標に沿って、航空宇宙・防衛分野における持続可能なソリューションを重視しており、環境に優しい技術に対する需要の高まりに確実に応えています。さらに、学術機関や防衛関連企業との協力関係を築くことで、グリーンUAV革命の最前線に立ち続けることができます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 監視および偵察アプリケーションの需要の増加

- クリーンで持続可能な推進技術への投資の増加

- 商業・産業用途での採用が増加

- 政府の支援と軍事近代化プログラム

- 燃料電池技術に対する政府および機関の支援の増加

- 業界の潜在的リスク&課題

- 燃料電池システムの高コスト

- 規制と空域制限

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:無人機の種類別、2021年~2034年

- 主要動向

- 固定翼無人航空機

- 回転翼無人航空機

- ハイブリッドVTOL無人航空機

第6章 市場推計・予測:範囲別、2021年~2034年

- 主要動向

- 短距離(50 km未満)

- 中距離(50~200 km)

- 長距離(200 km以上)

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 軍事・防衛

- 商業・産業

- 配送と物流

- 航空監視と地図作成

- 農薬散布

- 環境モニタリング

- その他

- 民間/政府

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- AeroVironment

- Aurora Flight Sciences

- Doosan Mobility Innovation

- Elbit Systems

- FlightWave Aerospace

- Hylium Industries

- ISS Group

- JOUAV

- MMCUAV

The Global Fuel Cell UAV Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 14.4% to reach USD 6.8 billion by 2034, driven by increasing government and institutional support for fuel cell technologies, as well as rising demand for surveillance and reconnaissance systems. However, the market faced challenges due to the U.S. administration's trade policies, including tariffs on Chinese imports, which led to higher costs for key components such as hydrogen storage systems, fuel cell stacks, and composite materials. This disrupted global supply chains, impacted pricing, and slowed research and development efforts.

Despite this, the fuel cell UAV sector continues to experience significant growth, driven by the numerous advantages these UAVs offer. These include superior endurance, reduced noise emissions, and extended flight durations, making them particularly suitable for critical operations, including defense, environmental monitoring, and disaster response. Their ability to operate silently for longer periods without needing frequent refueling is becoming a key feature that differentiates fuel cell UAVs from their traditional counterparts, positioning them as essential tools for surveillance, reconnaissance, and emergency operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $6.8 Billion |

| CAGR | 14.4% |

As fuel cell UAV technology advances, fixed-wing UAVs are anticipated to become a major contributor to market growth, projected to reach USD 3.1 billion by 2034. These UAVs are particularly favored for long-duration missions, where high aerodynamic efficiency and the capacity to carry larger hydrogen fuel cell systems are crucial. Their ability to maintain extended flight times without compromising on fuel consumption is making them indispensable in applications like border surveillance, environmental monitoring, and defense operations, where coverage over vast geographic areas is necessary. The ability to deploy these UAVs for longer missions provides strategic advantages, particularly in operations where endurance is critical.

The short-range fuel cell UAV segment is projected to grow at a CAGR of 12.8% through 2034, short-range fuel cell UAVs are gaining popularity due to their quick refueling capability and longer flight times compared to their traditional counterparts. These UAVs are ideal for industrial inspections, public safety tasks, and other applications that require sustained, reliable performance in confined operational areas. As technology improves, these UAVs become more versatile and efficient, driving their adoption in various industries.

Germany Fuel Cell UAV Market is expected to grow at a CAGR of 13.7% through 2034 fueled by national policies focused on decarbonization and sustainability, along with EU-backed research programs that encourage innovation in green technologies. Germany's commitment to reducing carbon emissions and promoting sustainable aviation solutions drives investments in hydrogen-powered UAV technologies. Furthermore, collaborations between defense contractors, aerospace companies, and academic institutions are positioning the country as a leader in green UAV technologies, making it a hub for advanced UAV research and development.

Key market players in the Global Fuel Cell UAV Industry include Hylium Industries, AeroVironment, FlightWave Aerospace, Doosan Mobility Innovation, ISS Group, Aurora Flight Sciences, MMCUAV, and Elbit Systems. To strengthen their market position, companies in the fuel cell UAV sector focus on developing cutting-edge fuel cell technology that enhances the efficiency and endurance of UAVs. Collaborating with governments and public-private partnerships allows them to access funding and technical resources, reducing development costs. By advancing R&D efforts, these companies are driving innovation and contributing to the adoption of hydrogen-powered UAVs. They also emphasize sustainable solutions in aerospace and defense, in line with global carbon neutrality goals, ensuring that their products meet the growing demand for eco-friendly technologies. Additionally, forging collaborations with academic institutions and defense contractors helps them remain at the forefront of the green UAV revolution.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1.1 Supply chain reconfiguration

- 3.2.4.1.2 Pricing and product strategies

- 3.2.4.1.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growing demand for surveillance and reconnaissance applications

- 3.3.1.2 Rising investments in clean and sustainable propulsion technologies

- 3.3.1.3 Increasing adoption in commercial and industrial applications

- 3.3.1.4 Government support and military modernization programs

- 3.3.1.5 Rising government and institutional support for fuel cell technology

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High cost of fuel cell systems

- 3.3.2.2 Regulatory and airspace restrictions

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 Pestel analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By UAV Type, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Fixed wing UAVs

- 5.3 Rotary wing UAVs

- 5.4 Hybrid VTOL UAVs

Chapter 6 Market Estimates & Forecast, By Range, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Short range (< 50 km)

- 6.3 Medium range (50-200 km)

- 6.4 Long range (>200 km)

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Military & defense

- 7.3 Commercial & industrial

- 7.3.1 Delivery and logistics

- 7.3.2 Aerial surveillance and mapping

- 7.3.3 Pesticide spraying

- 7.3.4 Environmental monitoring

- 7.3.5 Others

- 7.4 Civil/government

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AeroVironment

- 9.2 Aurora Flight Sciences

- 9.3 Doosan Mobility Innovation

- 9.4 Elbit Systems

- 9.5 FlightWave Aerospace

- 9.6 Hylium Industries

- 9.7 ISS Group

- 9.8 JOUAV

- 9.9 MMCUAV