眼科用顕微鏡の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Ophthalmic Microscopes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755306

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

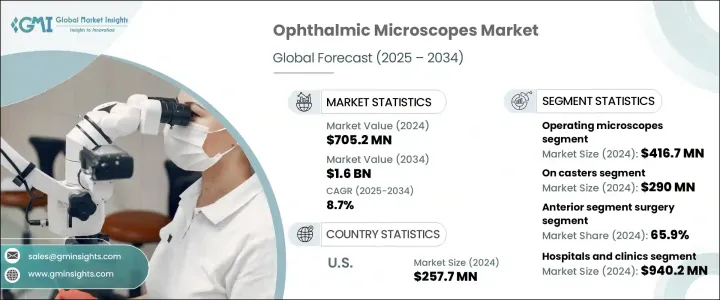

世界の眼科用顕微鏡市場は、2024年に7億520万米ドルと評価され、CAGR 8.7%で成長し、2034年には16億米ドルに達すると予測されています。

この大幅な成長は、眼科機器の技術的進歩の高まり、高齢者の増加、低侵襲眼科手術への嗜好の高まりに起因しています。白内障、緑内障、加齢黄斑変性などの眼に関連する疾患の流行は、先進的外科的介入に対する需要を加速させています。

最新の眼科用顕微鏡は、3D視覚化、光干渉断層計(OCT)、拡張現実オーバーレイを搭載し、手術の精度を高め、トレーニングを強化し、手術時間を短縮しています。人間工学に基づいて設計されたより優れた手術器具への需要が高まるにつれ、高精度光学系を備えたこれらの顕微鏡は進化を続け、より多機能になり、クリニックや病院で広く採用されるようになっています。

| 市場規模 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 7億520万米ドル |

| 予測金額 | 16億米ドル |

| CAGR | 8.7% |

これらの機器は、眼科手術、特に眼球の前眼部と後眼部の両方に関わる幅広い手術に不可欠です。外科医に高解像度の拡大画像を提供することで、白内障除去、角膜移植、網膜手術、緑内障治療などの精密で複雑な手術が容易になります。角膜、水晶体、網膜、硝子体などの繊細な構造を可視化できるため、外科医はこれらの手術を比類のない精度で行うことができます。この高精細画像により、最も複雑な手術であっても最小限のリスクで実施することができ、ミスの可能性を減らし、患者の転帰を改善することができます。

2024年には、手術用顕微鏡部門が市場をリードし、4億1,670万米ドルを稼ぎ出しました。特に高齢者の間で加齢に伴う眼疾患の発生率が増加しており、眼科手術の需要が急増しています。さらに、外来手術やデイケア手術の動向が、コンパクトで移動可能な多用途手術用顕微鏡の必要性を高めています。これらの手術用顕微鏡は、メンテナンスと移動が容易なモジュール型コンポーネントで設計されているため、外来手術センターに最適です。様々なクリニックに簡単に持ち運んで使用することができるため、ヘルスケアセグメントにおける柔軟で費用対効果の高いソリューションへのニーズの高まりに合致しています。

病院クリニックセグメントは2024年に最大のシェアを占め、2034年には9億4,020万米ドルに達すると予想されています。専門的な眼科サービスの需要が高まるにつれ、多くの病院や複数専門クリニックが眼科専用ユニットを設置し、さまざまな眼科処置に先進的手術用顕微鏡を必要としています。都市部のヘルスケアインフラ、特にヘルスケアハブへの投資の増加に伴い、眼科用顕微鏡の購入が顕著に増加しています。このような医療センターでは、高い手術精度、安全性、全体的な患者の転帰を保証する機器を優先しています。眼科用顕微鏡は視認性を高めるだけでなく、手術ミスや術後の合併症を最小限に抑え、需要を牽引しています。

米国の眼科用顕微鏡市場は、2024年には2億5,770万米ドルとなりました。白内障、緑内障、加齢黄斑変性などの眼科疾患の罹患率が上昇していることが、こうした先進的な機器の需要を押し上げています。さらに、米国における白内障手術に対する有利な償還施策が、ヘルスケアプロバイダによるハイエンド手術システムの採用を後押ししています。このような償還構造は、眼科手術の新技術への投資を加速させ、コスト回収を合理化します。さらに、米国は眼科用顕微鏡市場の大手メーカーやイノベーターの拠点としての役割も果たしています。

世界の眼科用顕微鏡市場で事業を展開している著名な企業には、ZEISS、Alcon、HAAG-STREIT GROUP、HAI Laboratories、Inami、KARL KAPS、Keeler、LABOMED、Leica、MOPTIM、Reichert、Rexxam、TAKAGI、TOPCONなどがあります。眼科用顕微鏡市場では、各社がその地位を固めるためにいくつかの重要な戦略を採用しています。これらには、進化する外科手術のニーズに対応するため、デジタル統合の強化、3Dイメージング機能、人間工学に基づいたデザインなど、製品機能の継続的な革新が含まれます。メーカー各社は、顕微鏡の機能性と精度を向上させるために先端技術に投資しており、眼科手術に欠かせないツールとなっています。市場シェアを拡大するため、多くの企業がヘルスケア機関やクリニックと戦略的パートナーシップや提携を結んでいます。また、新興市場を対象に、優れた品質を確保しつつ、現地のヘルスケア需要に対応した費用対効果の高いモデルを投入しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- 産業への影響要因

- 促進要因

- 眼疾患の有病率の上昇

- 低侵襲眼科手術の導入拡大

- 技術的進歩

- 白内障と屈折矯正手術件数の急増

- 産業の潜在的リスク・課題

- 先進的眼科用顕微鏡に関連する高コスト

- 厳格な規制要件

- 促進要因

- 成長可能性分析

- 規制情勢

- 米国

- 欧州

- 技術

- 償還シナリオ

- 価格分析

- 製品比較の展望

- ポーター分析

- PESTEL分析

- ギャップ分析

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推定・予測:製品タイプ別、2021~2034年

- 主要動向

- 手術用顕微鏡

- 検査用顕微鏡

第6章 市場推定・予測:モダリティ別、2021~2034年

- 主要動向

- キャスター付き

- 天井取り付け型

- 卓上型

- 壁掛け式

第7章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 前眼部手術

- 白内障手術

- 屈折矯正手術

- 緑内障手術

- 角膜手術

- レーザー眼科手術

- 後眼部手術

- ウイルス切除術

- 網膜剥離の修復

- 黄斑円孔修復

- 黄斑症手術

- 後部強膜切除術

- 放射状視神経切開術

- 黄斑転座手術

第8章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 病院とクリニック

- 外来手術センター

- その他

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- ZEISS

- Alcon

- HAAG-STREIT GROUP

- HAI Laboratories

- Inami

- KARL KAPS

- Keeler

- LABOMED

- Leica

- MOPTIM

- Reichert

- Rexxam

- TAKAGI

- TOPCON

目次

The Global Ophthalmic Microscopes Market was valued at USD 705.2 million in 2024 and is estimated to grow at a CAGR of 8.7% to reach USD 1.6 billion by 2034. The substantial growth can be attributed to the rising technological advancements in ophthalmic equipment, the increasing geriatric population, and the growing preference for minimally invasive ophthalmic surgeries. The prevalence of eye-related conditions like cataracts, glaucoma, and age-related macular degeneration is accelerating the demand for advanced surgical interventions.

Modern ophthalmic microscopes now feature 3D visualization, optical coherence tomography (OCT), and augmented reality overlays that improve the precision of surgeries, enhance training, and reduce surgical time. As the demand for better-equipped, ergonomically designed surgical instruments increases, these microscopes, with their high-precision optics, continue to evolve, becoming more multifunctional and widely adopted across clinics and hospitals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $705.2 Million |

| Forecast Value | $1.6 Billion |

| CAGR | 8.7% |

These devices are essential for a wide range of ophthalmic surgeries, particularly those involving both the anterior and posterior segments of the eye. By providing surgeons with high-resolution, magnified images, they facilitate precise and intricate procedures, such as cataract removal, corneal transplants, retinal surgeries, and glaucoma treatments. The ability to visualize delicate structures, such as the cornea, lens, retina, and vitreous, allows surgeons to perform these operations with unparalleled accuracy. This high-definition imaging ensures that even the most complex surgeries are conducted with minimal risk, reducing the likelihood of errors and improving patient outcomes.

In 2024, the operating microscope segment led the market, generating USD 416.7 million. With the increasing incidence of age-related eye diseases, particularly among the elderly, the demand for ophthalmic surgeries has surged. Moreover, the trend toward outpatient and daycare surgeries is driving the need for compact, mobile, and versatile operating microscopes. These microscopes are designed with modular components for easy maintenance and mobility, making them ideal for ambulatory surgery centers. Their ability to be easily transported and used across various clinics aligns with the growing need for flexible, cost-effective solutions in the healthcare sector.

The hospitals and clinics segment held the largest share in 2024 and is expected to reach USD 940.2 million by 2034. As demand for specialized ophthalmology services rises, many hospitals and multi-specialty clinics are establishing dedicated ophthalmic units, which require advanced surgical microscopes for a variety of eye procedures. With increasing investments in urban healthcare infrastructure, particularly in healthcare hubs, there has been a marked rise in the purchase of ophthalmic microscopes. These medical centers prioritize equipment that ensures high surgical accuracy, safety, and overall patient outcomes. Ophthalmic microscopes not only enhance visualization but also minimize surgical errors and postoperative complications, driving their demand.

U.S. Ophthalmic Microscopes Market was valued at USD 257.7 million in 2024. The rising incidence of ophthalmic conditions such as cataracts, glaucoma, and age-related macular degeneration is boosting the demand for these advanced devices. Furthermore, favorable reimbursement policies for cataract surgeries in the U.S. support the adoption of high-end surgical systems by healthcare providers. This reimbursement structure accelerates the investment in new technologies for ophthalmic procedures, streamlining cost recovery. Additionally, the U.S. serves as a hub for leading manufacturers and innovators in the ophthalmic microscopes market.

Prominent companies operating in the Global Ophthalmic Microscopes Market include ZEISS, Alcon, HAAG-STREIT GROUP, HAI Laboratories, Inami, KARL KAPS, Keeler, LABOMED, Leica, MOPTIM, Reichert, Rexxam, TAKAGI, and TOPCON. In the ophthalmic microscopes market, companies are employing several key strategies to solidify their positions. These include ongoing innovation in product features, such as enhanced digital integration, 3D imaging capabilities, and ergonomic designs, to cater to evolving surgical needs. Manufacturers are investing in advanced technologies to improve the functionality and precision of microscopes, making them indispensable tools for eye surgeries. To expand market share, many companies are forming strategic partnerships and collaborations with healthcare institutions and clinics. Additionally, firms are targeting emerging markets with cost-effective models that meet local healthcare demands while ensuring superior quality.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of ophthalmic disorders

- 3.2.1.2 Growing adoption of minimally invasive ophthalmic surgeries

- 3.2.1.3 Technological advancements

- 3.2.1.4 Surge in cataract and refractive surgery volumes

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with advanced ophthalmic microscopes

- 3.2.2.2 Stringent regulatory requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Pricing analysis

- 3.8 Product comparison outlook

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Gap analysis

- 3.12 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Operating microscopes

- 5.3 Examination microscopes

Chapter 6 Market Estimates and Forecast, By Modality, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 On casters

- 6.3 Ceiling-mounted

- 6.4 Table-top

- 6.5 Wall-mounted

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Anterior segment surgery

- 7.2.1 Cataract surgery

- 7.2.2 Refractive surgery

- 7.2.3 Glaucoma surgery

- 7.2.4 Corneal surgery

- 7.2.5 Laser eye surgery

- 7.3 Posterior segment surgery

- 7.3.1 Virectomy

- 7.3.2 Retinal detachment repair

- 7.3.3 Macular hole repair

- 7.3.4 Maculopathy surgery

- 7.3.5 Posterior scelerectomy

- 7.3.6 Radial optic neurotomy

- 7.3.7 Macular translocaion surgery

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and clinics

- 8.3 Ambulatory surgical centres

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ZEISS

- 10.2 Alcon

- 10.3 HAAG-STREIT GROUP

- 10.4 HAI Laboratories

- 10.5 Inami

- 10.6 KARL KAPS

- 10.7 Keeler

- 10.8 LABOMED

- 10.9 Leica

- 10.10 MOPTIM

- 10.11 Reichert

- 10.12 Rexxam

- 10.13 TAKAGI

- 10.14 TOPCON

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日