|

市場調査レポート

商品コード

1755304

自律走行シミュレーションソリューションの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Autonomous Vehicle Simulation Solutions Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自律走行シミュレーションソリューションの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月29日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

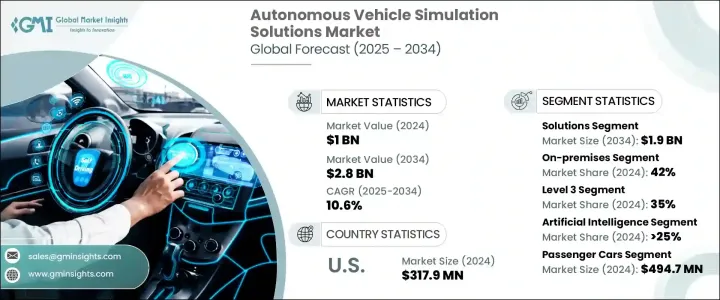

自律走行シミュレーションソリューションの世界市場規模は、2024年に10億米ドルとなり、CAGR 10.6%で成長し、2034年には28億米ドルに達すると予測されています。

この市場は、自律走行システムの進化、評価、展開をサポートする上で極めて重要な役割を果たしています。シミュレーション・プラットフォームは今や開発プロセスの不可欠な一部となっており、自動車メーカーや技術プロバイダーは、制御された再現可能な仮想環境で複雑な自動運転機能をテストし、検証することができます。このようなプラットフォームは現実世界の運転シナリオを再現するため、エンジニアは車両が道路を走るずっと前に重要な課題を特定し、解決することができます。自律走行システムがますます高度化し、微妙になっていくにつれて、設計、開発、安全性検証のすべてのフェーズでシミュレーションツールが必要とされています。

交通安全が依然として大きな課題となっている現在、シミュレーション技術は、交通事故による負傷者や死亡者の数を減らすための実用的なソリューションとして注目されています。従来の試験方法は、特に危険なシナリオや一般的でないシナリオを再現する場合、多くの場合、時間とコストがかかり、危険も伴います。シミュレーションは、人命を危険にさらすことなく何千ものエッジケースを分析できる、物理的なテストに代わるコスト効率と拡張性を提供することで、このギャップを埋めるものです。交通事故の大半をヒューマンエラーが占める中、人間のドライバーよりも安全で予測可能な自動運転システムの開発が急務となっています。シミュレーションベースのツールは、現実世界では再現できないような危険な条件や稀な条件も含め、無限の多様な条件下でこれらのシステムをテストすることを可能にします。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 10億米ドル |

| 予測金額 | 28億米ドル |

| CAGR | 10.6% |

人工知能、機械学習、高性能コンピューティング技術の進歩に伴い、シミュレーションプラットフォームはより高度で正確、かつスケーラブルになってきています。今日のソリューションは、基本的な環境モデリングにとどまらず、自律走行車開発のライフサイクル全体をサポートするリアルタイムのドライバーインザループテストやクラウドパワーによるシミュレーションを可能にしています。複雑なシナリオの生成から意思決定アルゴリズムの検証まで、これらのツールは業界が安全な自律走行システムを構築しテストする方法を変革しています。

コンポーネント別に見ると、市場はソリューションとサービスに区分されます。2024年には、ソリューションセグメントが世界市場の68%を占め、2034年までに19億米ドルの売上が見込まれています。このセグメントでは、主にダイナミックな仮想環境を提供する機能により、高度なソフトウェアに対する需要が急速に伸びています。これらのソフトウェアプラットフォームにより、エンジニアは交通シナリオから様々な環境条件下でのシステム応答まで、あらゆるシミュレーションを行うことができます。開発者はこれらのツールを使って、現実世界の課題を再現し、システム性能を最適化し、物理的なリスクや制限なしに規制へのコンプライアンスを確保します。

展開形態別に見ると、市場はオンプレミス型、クラウド型、ハイブリッド型に分けられます。2024年の市場シェアはオンプレミスソリューションが42%で、このセグメントを独占しています。高いデータ機密性、低遅延コンピューティング、シミュレーションパラメーターの完全制御を必要とする企業は、これらのセットアップを好みます。これは特に、リアルタイムシミュレーションや、機密性の高い独自技術のテストを行う企業に当てはまる。

自律性レベルに関しては、市場にはレベル1からレベル5以上の分類があります。レベル3のセグメント(条件付き自動化)は、2024年の市場の35%を占めています。このレベルでは、特定の条件下で車両がほとんどの運転機能を処理することが求められるが、促されている場合は依然として人間の介入に依存しています。レベル3システムでは、手動制御と自動制御の間でより複雑な移行シナリオが導入されるため、シミュレーションは、システム間の安全なハンドオフを保証するために、これらのライフサイクルの移行をテストする上で重要な役割を果たします。これらのシステムをサポートするサービス分野は、予測期間中に約9.5%のCAGRで拡大する見込みです。

技術別では、人工知能、機械学習、AR/VR、ビッグデータ分析、その他が対象となります。人工知能セグメントは2024年に25%以上のシェアで市場をリードしました。AIは、インテリジェントなシナリオ生成と予測モデリングを可能にすることで、シミュレーション環境を強化します。これにより、シミュレーションの応答性、現実性が高まり、車両、歩行者、環境間の複雑な相互作用を表現できるようになります。また、AIはシミュレーションの効率的な拡張にも役立ち、開発者はより幅広い条件でシステムの訓練と検証を行うことができます。

車両タイプに基づき、市場は乗用車、商用車、二輪車・宅配ボットに分類されます。乗用車セグメントは2024年に最大となり、4億9,470万米ドルを創出しました。一般消費者向け自動車に半自律走行機能が搭載されるようになり、アダプティブクルーズコントロール、レーンキープ、自律駐車などの運転支援機能の検証にはシミュレーションソリューションが不可欠です。これらのソリューションは、メーカーが実社会への配備前にこれらのシステムの信頼性と安全性を確保するのに役立ちます。

地域別では、米国が北米市場をリードし、2024年の売上高は3億1,790万米ドルでした。この成長の原動力となっているのは、技術革新の強固なエコシステムと、自律走行車のテストと配備を支援する有利な政策です。国内の主要企業は、開発期間を短縮し、物理的テストに伴うリスクを軽減するために、シミュレーション技術に積極的に投資しています。米国の規制状況もシミュレーションベースの検証を促進しており、同国を世界情勢のフロントランナーとして位置付けています。

市場の主要企業は、パートナーシップ、合併、買収、研究開発投資などの戦略的イニシアチブを推進し、シミュレーション能力の強化を図っています。こうした取り組みは、AI、機械学習、デジタルツインテクノロジーを組み合わせた最先端のプラットフォームを開発し、テストカバレッジ、拡張性、精度を向上させることに重点を置いています。また、各社はOEMや規制機関と緊密に連携し、自社のソリューションを進化する業界標準に合わせ、自律走行車の商用化を加速させています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- クラウドプラットフォームプロバイダー

- シナリオ生成・管理サービスプロバイダー

- ハードウェアインザループ(HiL)およびソフトウェアインザループ(SiL)テストプロバイダー

- デジタルツインおよび仮想車両サービスプロバイダー

- 検証および安全性コンプライアンスサービスプロバイダー

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- サプライヤーの情勢

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- AI駆動型シナリオ生成とテスト

- リアルタイムセンサーフュージョンシミュレーション

- クラウドベースのシミュレーションとスケーラビリティ

- デジタルツインと仮想プロトタイピング

- 新興技術

- 物理ベースとデータ駆動型のハイブリッドシミュレーションモデル

- 車内リアルタイム検証のためのエッジAI

- 生成AIを用いた合成データ生成

- データの整合性とシミュレーションのトレーサビリティのためのブロックチェーン

- 先端材料科学

- 現在の技術動向

- 価格動向

- ユースケース

- 最良のシナリオ

- 主なニュースと取り組み

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 影響要因

- 促進要因

- AIと機械学習アルゴリズムの進歩

- ADASと自律システムの複雑化

- 高忠実度のセンサーモデリングと環境のリアリズムの必要性

- 仮想テストのスケーラビリティと費用対効果

- 業界の潜在的リスク&課題

- 現実世界の複雑さとエッジケースを再現する際の課題

- 高忠実度シミュレーションのための高い計算要件

- 市場機会

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

- 持続可能性と環境側面

- 持続可能な慣行

- 生産におけるエネルギー効率

- 環境に優しい取り組み

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- ソフトウェア

- シナリオ生成ツール

- センサーシミュレーションソフトウェア

- 3Dモデリングと視覚化

- 物理ベースのシミュレータ

- AI & MLシミュレーションプラットフォーム

- サービス

- コンサルティングおよび統合サービス

- サポートとメンテナンス

- シミュレーション・アズ・ア・サービス(SaaS)

第6章 市場推計・予測:自律レベル別、2021-2034

- 主要動向

- レベル1

- レベル2

- レベル3

- レベル4

- レベル5以上

第7章 市場推計・予測:技術別、2021-2034

- 主要動向

- 人工知能

- 機械学習

- 拡張現実/仮想現実(AR/VR)

- ビッグデータ分析

- その他

第8章 市場推計・予測:車両別、2021-2034

- 主要動向

- 乗用車

- サダン

- ハッチバック

- SUV

- 商用車

- 軽商用車

- 大型商用車

- バスと長距離バス

- 二輪車と配達ロボット

第9章 市場推計・予測:展開別、2021-2034

- 主要動向

- オンプレミス

- クラウドベース

- ハイブリッド

第10章 市場推計・予測:用途別、2021-2034

- 主要動向

- テストと検証

- トレーニングと教育

- システム統合

- データの注釈とラベル付け

- パフォーマンスの最適化

第11章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 自動車OEM

- ティア1およびティア2サプライヤー

- テクノロジー企業

- 政府および規制機関

第12章 市場推計・予測:地域別、2021-2034

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベルギー

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- シンガポール

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第13章 企業プロファイル

- aiMotive

- Altair

- Ansys

- Applied Intuition

- Aptiv

- AVL List

- Cambridge Systematics

- Cognata

- Dassault

- dSPACE

- Foretellix

- Green Hills

- Hexagon

- IPG Automotive

- LG

- LHP Engineering

- MathWorks

- Mechanical Simulation

- rFpro

- Siemens

- Synopsys

The Global Autonomous Vehicle Simulation Solutions Market was valued at USD 1 billion in 2024 and is estimated to grow at a CAGR of 10.6% to reach USD 2.8 billion by 2034. This market plays a pivotal role in supporting the evolution, evaluation, and deployment of autonomous driving systems. Simulation platforms are now an essential part of the development process, allowing automotive manufacturers and technology providers to test and validate complex automated driving functions in controlled and repeatable virtual environments. These platforms replicate real-world driving scenarios, enabling engineers to identify and resolve critical challenges long before vehicles hit the road. As autonomous systems become increasingly advanced and nuanced, simulation tools are needed across all phases of design, development, and safety validation.

In a world where road safety remains a major concern, simulation technologies are seen as a practical solution to reduce the staggering toll of traffic-related injuries and fatalities. Traditional testing methods are often time-consuming, expensive, and risky, especially when recreating dangerous or uncommon scenarios. Simulations bridge this gap by offering a cost-effective and scalable alternative to physical testing, where thousands of edge cases can be analyzed without endangering human life. With human error accounting for the majority of traffic incidents, there is a growing urgency to develop automated systems that can operate more safely and predictably than human drivers. Simulation-based tools make it possible to test these systems under an infinite variety of conditions, including those that are too hazardous or rare to replicate in the real world.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1 Billion |

| Forecast Value | $2.8 Billion |

| CAGR | 10.6% |

As artificial intelligence, machine learning, and high-performance computing technologies continue to progress, simulation platforms have become more advanced, accurate, and scalable. Today's solutions go far beyond basic environmental modeling; they enable real-time, driver-in-the-loop testing and cloud-powered simulations that support the full lifecycle of autonomous vehicle development. From generating complex scenarios to validating decision-making algorithms, these tools are transforming how the industry builds and tests safe autonomous systems.

By component, the market is segmented into solutions and services. In 2024, the solutions segment accounted for 68% of the global market and is expected to generate USD 1.9 billion in revenue by 2034. The demand for advanced software in this segment is growing rapidly, primarily due to its ability to offer dynamic virtual environments. These software platforms allow engineers to simulate everything from traffic scenarios to system responses under various environmental conditions. Developers use these tools to replicate real-world challenges, optimize system performance, and ensure regulatory compliance without physical risks or limitations.

Deployment-wise, the market is divided into on-premises, cloud-based, and hybrid models. On-premises solutions dominated the segment with a 42% market share in 2024. Companies requiring high data confidentiality, low-latency computing, and full control over simulation parameters prefer these setups. This is especially true for firms conducting real-time simulations or testing sensitive, proprietary technologies.

In terms of autonomy level, the market includes level 1 through more than level 5 classifications. The level 3 segment-conditional automation-held 35% of the market in 2024. This level requires the vehicle to handle most driving functions under specific conditions but still relies on human intervention when prompted. As level 3 systems introduce more complex transition scenarios between manual and automated control, simulation plays a critical role in testing these life-cycle transitions to ensure safe handoffs between systems. The services segment supporting these systems is expected to expand at a CAGR of around 9.5% over the forecast period.

By technology, the market covers Artificial Intelligence, Machine Learning, AR/VR, Big Data Analytics, and others. The Artificial Intelligence segment led the market with over 25% share in 2024. AI enhances simulation environments by enabling intelligent scenario generation and predictive modeling. It makes simulations more responsive, realistic, and capable of representing complex interactions among vehicles, pedestrians, and the environment. AI also helps scale simulations efficiently, allowing developers to train and validate systems on a wider range of conditions.

Based on vehicle type, the market is categorized into passenger cars, commercial vehicles, and two-wheelers & delivery bots. The passenger cars segment was the largest in 2024, generating USD 494.7 million. With the rising integration of semi-autonomous features in consumer vehicles, simulation solutions are essential for validating driver-assistance functions like adaptive cruise control, lane keeping, and autonomous parking. These solutions help manufacturers ensure the reliability and safety of these systems before real-world deployment.

Regionally, the U.S. led the North American market with revenue of USD 317.9 million in 2024. This growth is fueled by a robust ecosystem of innovation and favorable policies supporting autonomous vehicle testing and deployment. Leading domestic companies are actively investing in simulation technologies to accelerate their development timelines and reduce risks associated with physical testing. Regulatory frameworks in the U.S. also promote simulation-based validation, positioning the country as a front-runner in the global landscape.

Key market players are pursuing strategic initiatives such as partnerships, mergers, acquisitions, and R&D investments to enhance their simulation capabilities. These efforts are focused on developing cutting-edge platforms that combine AI, machine learning, and digital twin technologies to improve test coverage, scalability, and accuracy. Companies are also working closely with OEMs and regulatory bodies to align their solutions with evolving industry standards and accelerate the commercialization of autonomous vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model.

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Autonomy level

- 2.2.4 Technology

- 2.2.5 Vehicle

- 2.2.6 Deployment

- 2.2.7 Application

- 2.2.8 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Cloud platform providers

- 3.1.1.2 Scenario generation & management service providers

- 3.1.1.3 Hardware-in-the-loop (HiL) & software-in-the-loop (SiL) testing providers

- 3.1.1.4 Digital twin & virtual vehicle service providers

- 3.1.1.5 Validation & safety compliance service providers

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.2.1 Current technological trends

- 3.2.1.1 AI-driven scenario generation and testing

- 3.2.1.2 Real-time sensor fusion simulation

- 3.2.1.3 Cloud-based simulation and scalability

- 3.2.1.4 Digital twin and virtual prototyping

- 3.2.2 Emerging Technologies

- 3.2.2.1 Physics-based and data-driven hybrid simulation models

- 3.2.2.2 Edge AI for in-vehicle real-time validation

- 3.2.2.3 Synthetic data generation using generative AI

- 3.2.2.4 Blockchain for data integrity and simulation traceability

- 3.2.3 Advanced material sciences

- 3.2.1 Current technological trends

- 3.3 Pricing trend

- 3.4 Use cases

- 3.5 Best-case scenario

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.7.4 Latin America

- 3.7.5 Middle East & Africa

- 3.8 Impact on forces

- 3.8.1 Growth drivers

- 3.8.1.1 Advancements in AI and machine learning algorithms

- 3.8.1.2 Growing complexity of ADAS and autonomous systems

- 3.8.1.3 Need for high-fidelity sensor modeling and environmental realism

- 3.8.1.4 Scalability and cost-effectiveness of virtual testing

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Challenges in replicating real-world complexity and edge cases

- 3.8.2.2 High computational requirements for high-fidelity simulations

- 3.8.3 Market opportunity

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Energy efficiency in production

- 3.12.3 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Scenario generation tools

- 5.2.2 Sensor simulation software

- 5.2.3 3D modeling and visualization

- 5.2.4 Physics-based simulators

- 5.2.5 AI & ML simulation platforms

- 5.3 Services

- 5.3.1 Consulting & integration services

- 5.3.2 Support & maintenance

- 5.3.3 Simulation-as-a-Service (SaaS)

Chapter 6 Market Estimates & Forecast, By Autonomy level, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Level 1

- 6.3 Level 2

- 6.4 Level 3

- 6.5 Level 4

- 6.6 Level 5 and above

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Artificial intelligence

- 7.3 Machine learning

- 7.4 Augmented reality / virtual reality (AR/VR)

- 7.5 Big data analytics

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Sadan

- 8.2.2 Hatchback

- 8.2.3 SUV

- 8.3 Commercial vehicles

- 8.3.1 Light commercial vehicle

- 8.3.2 Heavy commercial vehicle

- 8.3.3 Buses & coaches

- 8.4 Two-wheelers & delivery bots

Chapter 9 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 On-premises

- 9.3 Cloud-based

- 9.4 Hybrid

Chapter 10 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 Testing & validation

- 10.3 Training & education

- 10.4 System integration

- 10.5 Data annotation & labeling

- 10.6 Performance optimization

Chapter 11 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 11.1 Key trends

- 11.2 Automotive OEMs

- 11.3 Tier 1 & tier 2 suppliers

- 11.4 Tech companies

- 11.5 Government & regulatory bodies

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 12.1 North America

- 12.1.1 U.S.

- 12.1.2 Canada

- 12.2 Europe

- 12.2.1 UK

- 12.2.2 Germany

- 12.2.3 France

- 12.2.4 Italy

- 12.2.5 Spain

- 12.2.6 Belgium

- 12.2.7 Sweden

- 12.3 Asia Pacific

- 12.3.1 China

- 12.3.2 India

- 12.3.3 Japan

- 12.3.4 Australia

- 12.3.5 Singapore

- 12.3.6 South Korea

- 12.3.7 Southeast Asia

- 12.4 Latin America

- 12.4.1 Brazil

- 12.4.2 Mexico

- 12.4.3 Argentina

- 12.5 MEA

- 12.5.1 South Africa

- 12.5.2 Saudi Arabia

- 12.5.3 UAE

Chapter 13 Company Profiles

- 13.1 aiMotive

- 13.2 Altair

- 13.3 Ansys

- 13.4 Applied Intuition

- 13.5 Aptiv

- 13.6 AVL List

- 13.7 Cambridge Systematics

- 13.8 Cognata

- 13.9 Dassault

- 13.10 dSPACE

- 13.11 Foretellix

- 13.12 Green Hills

- 13.13 Hexagon

- 13.14 IPG Automotive

- 13.15 LG

- 13.16 LHP Engineering

- 13.17 MathWorks

- 13.18 Mechanical Simulation

- 13.19 rFpro

- 13.20 Siemens

- 13.21 Synopsys