血液透析用人工血管の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Hemodialysis Vascular Grafts Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755295

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

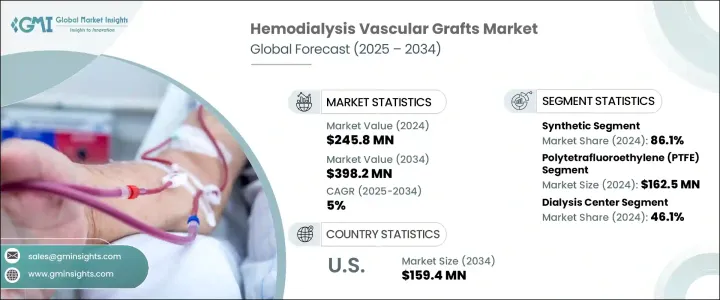

血液透析用人工血管の世界市場は、2024年に2億4,580万米ドルと評価され、CAGR 5%で成長し、2034年には3億9,820万米ドルに達すると予測されています。

これらの医療機器は、血液透析を受ける患者、特に動静脈瘻の適応とならない末期腎不全(ESRD)の患者にバスキュラーアクセスを提供する上で重要な役割を果たしています。糖尿病、高血圧、高齢化によってESRDの世界の負担が増加していることが、血液透析治療に対するニーズの高まりにつながっています。さらに、生体工学やハイブリッド材料の開発などの移植片技術の革新により、これらの移植片の耐久性、柔軟性、生体適合性が向上しており、その結果、合併症の発生が少なく、移植片の開存期間が延長し、先進国市場でも新興国市場でも広く臨床採用されています。

慢性腎臓病(CKD)とESRDの増加は、世界人口の高齢化と相関しています。バスキュラーアクセスが限られていることが多い高齢患者は、人工血管や生物学的人工血管への依存度が高くなり、グラフトベースの透析アクセスに対する需要がさらに高まっています。新興諸国における透析センターの増加は、ヘルスケアサービスへのアクセス向上とともに、人工血管の利用を増加させています。政府の取り組みや腎医療への投資の増加も、高度なグラフト技術をより安価で入手しやすくすることに貢献しており、腎ヘルスケアインフラの世界の成長を支えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 2億4,580万米ドル |

| 予測金額 | 3億9,820万米ドル |

| CAGR | 5% |

2024年には、合成グラフト部門が86.1%の大きなシェアを占めて市場をリードしました。合成血液透析グラフトは、成熟に数週間を要する動静脈瘻とは異なり、すぐに使用できます。この即時利用可能性により、合成グラフトは急性透析や緊急透析の状況に欠かせないものとなっています。さらに、発泡ポリテトラフルオロエチレン(ePTFE)やポリウレタンなどの合成材料は、これらのグラフトの性能、柔軟性、耐久性を向上させています。表面治療やヘパリン結合コーティングは血栓症や感染のリスクを低減し、合成グラフトを長期透析療法により効果的なものにしています。特に病院や救急現場での緊急血液透析アクセスに対する需要の高まりにより、成熟時間が短く、生物学的移植片よりも好まれることが多い合成移植片の採用が増加しています。

透析センターセグメントは2024年に46.1%のシェアを占めました。世界の慢性腎臓病と末期腎臓病患者の増加が、透析センターの急成長に拍車をかけています。これらの施設が拡張し、より多くの患者を受け入れるようになると、血液透析グラフトなどのバスキュラーアクセスソリューションの需要が増加します。大量透析センターでは、患者のために信頼性が高く効果的なバスキュラーアクセスオプションが必要です。人工血液透析グラフトは、動静脈瘻と比較して成熟時間が短く、このような環境では特に有益であり、好ましい選択肢となっています。その結果、透析センターは合成グラフトを頻繁にストックするようになり、このセグメントの成長に寄与しています。

米国の血液透析用人工血管市場は2034年までに1億5,940万米ドルに達します。米国は糖尿病と高血圧の有病率が高く、慢性腎臓病と末期腎不全の主な原因となっています。これらの疾患の罹患率の増加は、長期透析を必要とする患者の増加を意味し、バスキュラーアクセスソリューションの需要を促進しています。メディケアをはじめとする連邦政府のヘルスケアプログラムは、透析治療とバスキュラーアクセス手技に包括的な保険適用を提供しているため、血液透析グラフトは患者にとってより身近なものとなっています。このような償還政策は、医療提供者が先進的なグラフト技術を採用する動機付けとなり、市場の成長をさらに後押ししています。

世界の血液透析用人工血管業界の主な市場企業には、Artivion、Becton Dickinson and Company、BIOVIC、Cook Medical、CryoLife、Getinge、Laminate Medical Technologies、LeMaitre、Merit Medical Systems、ParaGen Technologies、Proteon Therapeutics、Terumo Medical、Vascudyne、Vascular Genesis、W.L. Gore &Associatesなどがあります。血液透析用人工血管市場の企業は、市場での地位を高めるためにいくつかの重要な戦略を採用しています。これらの戦略には、移植片の性能、生体適合性、寿命を向上させるための研究開発への多額の投資が含まれます。メーカーはまた、患者の多様なニーズに対応するため、先端材料やハイブリッド移植片を導入して製品ポートフォリオを拡大することにも注力しています。ヘルスケアプロバイダー、病院、透析センターとの提携は、各社が新市場に参入し、製品の入手しやすさを向上させるのに役立っています。さらに足場を固めるため、企業は透析サービスの需要が伸びている新興市場に参入し、地理的なリーチを広げています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 末期腎疾患(ESRD)の有病率の上昇

- 移植材料と技術の進歩

- 高齢化人口の増加

- ヘルスケアインフラと透析センターの拡大

- 業界の潜在的リスク&課題

- 血管移植手術とデバイスの高コスト

- 感染症、血栓症、移植不全などの合併症のリスク

- 促進要因

- 成長可能性分析

- テクノロジーの情勢

- 将来の市場動向

- 規制情勢

- ギャップ分析

- 特許分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 競争市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 合成

- 生物学的

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- ポリテトラフルオロエチレン(PTFE)

- ポリウレタン

- ポリエステル

- 生物学的

- ハイブリッド

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- 透析センター

- その他の用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- メキシコ

- ブラジル

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Artivion

- Becton Dickinson and Company

- BIOVIC

- Cook Medical

- CryoLife

- Getinge

- Laminate Medical Technologies

- LeMaitre

- Merit Medical Systems

- ParaGen Technologies

- Proteon Therapeutics

- Terumo Medical

- Vascudyne

- Vascular Genesis

- W L Gore &Associates

目次

The Global Hemodialysis Vascular Grafts Market was valued at USD 245.8 million in 2024 and is estimated to grow at a CAGR of 5% to reach USD 398.2 million by 2034. These medical devices play a vital role in providing vascular access for patients undergoing hemodialysis, particularly those with end-stage renal disease (ESRD) who are not suitable candidates for arteriovenous fistulas. The increasing global burden of ESRD, driven by diabetes, hypertension, and aging populations, is contributing to a growing need for hemodialysis treatments. Moreover, innovations in graft technology, such as the development of bioengineered and hybrid materials, are enhancing the durability, flexibility, and biocompatibility of these grafts, which results in fewer complications, prolonged graft patency, and broader clinical adoption in both developed and emerging markets.

The rise in chronic kidney disease (CKD) and ESRD correlates with an aging global population. Elderly patients, who often have limited vascular access, rely more on synthetic or biological vascular grafts, further boosting the demand for graft-based dialysis access. The growth of dialysis centers in developing countries, along with enhanced healthcare service access, is increasing the utilization of vascular grafts. Government initiatives and rising investments in renal care also contribute to making advanced graft technologies more affordable and accessible, supporting global growth in renal healthcare infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $245.8 Million |

| Forecast Value | $398.2 Million |

| CAGR | 5% |

In 2024, the synthetic graft segment led the market with a significant share of 86.1%. Synthetic hemodialysis grafts offer immediate use, unlike arteriovenous fistulas, which require weeks for maturation. This immediate availability makes synthetic grafts essential for acute or emergency dialysis situations. Furthermore, synthetic materials such as expanded polytetrafluoroethylene (ePTFE) and polyurethane have improved the performance, flexibility, and durability of these grafts. Surface treatments and heparin-bonded coatings reduce the risk of thrombosis and infection, making synthetic grafts more effective for long-term dialysis therapies. The growing demand for emergency hemodialysis access, especially in hospitals and emergency settings, is increasing the adoption of synthetic grafts, which have shorter maturation times and are often preferred over their biological counterparts.

The dialysis centers segment held a 46.1% share in 2024. The rise in chronic kidney disease and end-stage renal disease cases worldwide has spurred the rapid growth of dialysis centers. As these facilities expand to accommodate more patients, the demand for vascular access solutions such as hemodialysis grafts increases. High-volume dialysis centers require reliable, effective vascular access options for their patients. Synthetic hemodialysis grafts, with their shorter maturation times compared to arteriovenous fistulas, are particularly beneficial in these settings, making them a preferred option. As a result, dialysis centers are frequently stocking synthetic grafts, contributing to the segment's growth.

U.S. Hemodialysis Vascular Grafts Market will reach USD 159.4 million by 2034. The U.S. faces a high prevalence of diabetes and hypertension, which are leading causes of chronic kidney disease and end-stage renal disease. The increasing incidence of these conditions means more patients require long-term dialysis, thereby driving demand for vascular access solutions. Medicare and other federal healthcare programs offer comprehensive coverage for dialysis treatments and vascular access procedures, which makes hemodialysis grafts more accessible to patients. These reimbursement policies incentivize healthcare providers to adopt advanced graft technologies, further fueling the market's growth.

Key market players in the Global Hemodialysis Vascular Grafts Industry include Artivion, Becton Dickinson and Company, BIOVIC, Cook Medical, CryoLife, Getinge, Laminate Medical Technologies, LeMaitre, Merit Medical Systems, ParaGen Technologies, Proteon Therapeutics, Terumo Medical, Vascudyne, Vascular Genesis, and W.L. Gore & Associates. Companies in the hemodialysis vascular grafts market are employing several key strategies to enhance their market position. These strategies include significant investments in research and development to improve graft performance, biocompatibility, and longevity. Manufacturers are also focusing on expanding their product portfolios by introducing advanced materials and hybrid grafts to meet the diverse needs of patients. Collaborations with healthcare providers, hospitals, and dialysis centers are helping companies penetrate new markets and improve product accessibility. To further strengthen their foothold, companies are increasing their geographic reach by entering emerging markets with growing demand for dialysis services.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of end-stage renal disease (ESRD)

- 3.2.1.2 Advancements in graft materials and technology

- 3.2.1.3 Growing geriatric population

- 3.2.1.4 Expanding healthcare infrastructure and dialysis centers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of vascular graft procedures and devices

- 3.2.2.2 Risk of complications such as infections, thrombosis, and graft failure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Future market trends

- 3.6 Regulatory landscape

- 3.7 Gap analysis

- 3.8 Patent analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Synthetic

- 5.3 Biological

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Polytetrafluoroethylene (PTFE)

- 6.3 Polyurethane

- 6.4 Polyester

- 6.5 Biological

- 6.6 Hybrid

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Dialysis centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Artivion

- 9.2 Becton Dickinson and Company

- 9.3 BIOVIC

- 9.4 Cook Medical

- 9.5 CryoLife

- 9.6 Getinge

- 9.7 Laminate Medical Technologies

- 9.8 LeMaitre

- 9.9 Merit Medical Systems

- 9.10 ParaGen Technologies

- 9.11 Proteon Therapeutics

- 9.12 Terumo Medical

- 9.13 Vascudyne

- 9.14 Vascular Genesis

- 9.15 W L Gore & Associates

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日