ゲートドライバICの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Gate Driver IC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 185 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755289

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

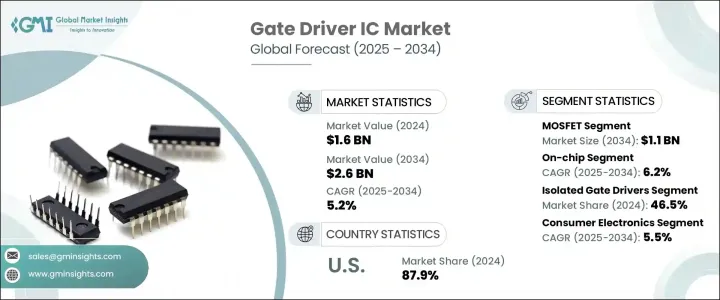

ゲートドライバICの世界市場規模は、2024年に16億米ドルとなり、CAGR 5.2%で成長し、2034年には26億米ドルに達すると予測されています。

成長の原動力は、産業オートメーションとロボティクスの導入が進むとともに、電気自動車とハイブリッド電気自動車(EV/HEV)の導入が増加していることです。産業界が製造、物流、プロセス制御の自動化を進めるにつれて、効率的で信頼性の高い電源管理ソリューションへのニーズが急増しています。ゲートドライバICは、自動化システムのモータードライブ、アクチュエータ、電力変換器に電力を供給するために不可欠であり、製造施設をスマートな生産拠点に変えるために不可欠なコンポーネントとなっています。

市場は旺盛な需要を目の当たりにしているが、トランプ政権下で課された関税による課題に直面しています。これらの関税、特に中国からの輸入品に対する関税は、世界の半導体サプライチェーンとゲートドライバICメーカーに影響を与えました。関税は生産コストとサプライチェーンの不確実性を増大させ、企業は代替調達戦略を模索したり、コストへの影響を最小化するために生産を多様化したりするよう促されました。こうした混乱は一時的に市場の成長を鈍化させたが、同時に主要企業がグローバル・サプライ・チェーンを見直すきっかけにもなりました。産業オートメーションが成長し、EVの普及が加速するにつれ、ゲートドライバIC市場は着実に拡大しています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 16億米ドル |

| 予測金額 | 26億米ドル |

| CAGR | 5.2% |

ゲートドライバIC市場は、さらにトランジスタタイプ別に区分され、MOSFET、IGBT、その他のカテゴリーがあります。このうち、MOSFETセグメントは2034年までに11億米ドルに達すると予測されています。MOSFET(Metal-Oxide-Semiconductor Field-Effect Transistor)は、パワーエレクトロニクス、特に家庭用電子機器、電源、さまざまな低~中電力アプリケーションで広く利用されています。その効率と多用途性により、さまざまな分野での進歩を促進する重要な部品となっています。GaNベース(窒化ガリウム)MOSFETの使用増加も市場成長に寄与しています。

ゲートドライバIC市場のもう1つの重要なセグメント分野は、オンチップとディスクリート構成を含む装着モードです。オンチップゲートドライバICセグメントは、2034年までCAGR 6.2%で成長すると予想され、よりコンパクトで統合されたソリューションに対する需要の高まりを反映しています。オンチップゲートドライバICは、制御機能と保護機能を同一チップ内に集積することで、システムの複雑さを大幅に軽減し、貴重なスペースを節約します。このため、小型パワーモジュール、ウェアラブル機器、携帯電子機器など、高集積化と小型化が求められるアプリケーションに特に適しています。

米国のゲートドライバIC 2024年のシェアは、電気自動車市場、航空宇宙エレクトロニクス、産業オートメーションが87.9%を占める。国内半導体製造を支援するCHIPS法はR&D資金を増加させ、ゲートドライバIC技術のイノベーションをさらに後押ししています。さらに、米国では電気自動車の新興企業や防衛関連企業が台頭しており、高性能ゲートドライバICの需要を押し上げています。

ゲートドライバICの世界市場における主要企業は、Infineon Technologies、Allegro Microsystems、Broadcom、Diodes Incorporated、Analog Devicesなどです。市場ポジションを強化するため、ゲートドライバIC市場の企業は、製品の性能とエネルギー効率を向上させるイノベーションに注力しています。大規模な研究開発投資により、スイッチング速度の高速化、高信頼性、熱管理の改善を実現する新しいゲートドライバIC技術が開発されました。自動車、航空宇宙、産業オートメーションなどの主要企業との戦略的提携により、各社は製品ラインナップの拡充を図っています。多くの企業は、関税などの地政学的要因の影響を緩和するためにサプライチェーンを多様化しており、一方で国内生産能力は需要の増加に対応しています。さらに、各企業は、産業用オートメーションや電気自動車の導入が急速に拡大している新興市場でのプレゼンス強化に取り組んでおり、世界な足場を固めるのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 電気自動車およびハイブリッド電気自動車(EV/HEV)の普及拡大

- 再生可能エネルギーシステムの需要の高まり

- 産業オートメーションとロボットの導入拡大

- 家電製品・家電の拡大

- スマートグリッドおよび配電システムにおけるゲートドライバICの統合

- 業界の潜在的リスク&課題

- 設計の複雑さと統合の課題

- 熱放散と熱管理の問題の増加

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:トランジスタの種類別、2021年~2034年

- 主要動向

- MOSFET

- IGBT

- その他

第6章 市場推計・予測:アタッチメントの形態別、2021年~2034年

- 主要動向

- オンチップ

- ディスクリート

第7章 市場推計・予測:分離タイプ別、2021年~2034年

- 主要動向

- 絶縁ゲートドライバ

- 光絶縁型

- 磁気絶縁型

- 容量絶縁型

- 非絶縁ゲートドライバ

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 家電

- 自動車

- エネルギーと電力

- 通信

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Allegro Microsystems

- Analog Devices

- Broadcom

- Diodes Incorporated

- Infineon Technologies

- Littelfuse

- Microchip Technology

- NXP Semiconductors

- Onsemi

- Renesas Electronics

- Rohm Semiconductor

- Semikron Danfoss

- Skyworks Solutions

- STMicroelectronics

- Texas Instruments

- Toshiba

- Vishay Intertechnology

- Wolfspeed

目次

The Global Gate Driver IC Market was valued at USD 1.6 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 2.6 billion by 2034. The growth is driven by the rising adoption of electric and hybrid electric vehicles (EV/HEV), alongside the growing implementation of industrial automation and robotics. As industries move toward greater automation in manufacturing, logistics, and process control, the need for efficient and reliable power management solutions has surged. Gate driver ICs are critical for powering motor drives, actuators, and power converters in automated systems, making them an essential component for transforming manufacturing facilities into smart production hubs.

While the market is witnessing robust demand, it has faced challenges due to tariffs imposed during the Trump administration. These tariffs, particularly on Chinese imports, impacted the global semiconductor supply chain and gate driver IC manufacturers, many of whom relied on Chinese components. The tariffs increased production costs and supply chain uncertainties, prompting businesses to seek alternative sourcing strategies or diversify their production to minimize cost impacts. These disruptions slowed market growth for a time but also led companies to rethink their global supply chains. As industrial automation grows and EV adoption accelerates, the market for gate driver ICs is steadily expanding.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 5.2% |

The gate driver IC market is further segmented by transistor type, which includes MOSFET, IGBT, and other categories. Among these, the MOSFET segment is expected to reach USD 1.1 billion by 2034. MOSFETs (Metal-Oxide-Semiconductor Field-Effect Transistors) are widely utilized in power electronics, particularly in consumer electronics, power supplies, and various low to mid-power applications. Their efficiency and versatility have made them a key component in driving advancements across several sectors. The increasing use of GaN-based (Gallium Nitride) MOSFETs has also contributed to market growth.

Another key area of segmentation in the gate driver IC market is the mode of attachment, which includes on-chip and discrete configurations. The on-chip gate driver IC segment is expected to grow at a CAGR of 6.2% through 2034, reflecting the increasing demand for more compact and integrated solutions. On-chip gate driver ICs integrate control and protection functions within the same chip, significantly reducing system complexity and saving valuable space. This makes them particularly suitable for applications that require high integration and miniaturization, such as in compact power modules, wearables, and portable electronics.

United States Gate Driver IC Market accounted for 87.9% share in 2024 driven by the electric vehicle market, aerospace electronics, and industrial automation. The CHIPS Act, which supports domestic semiconductor manufacturing, has increased R&D funding, helping to further drive innovation in gate driver IC technologies. Additionally, the rise of electric vehicle startups and defense contractors in the U.S. boosts the demand for high-performance gate driver ICs.

Key players in the Global Gate Driver IC Market include Infineon Technologies, Allegro Microsystems, Broadcom, Diodes Incorporated, and Analog Devices. To strengthen their market position, companies in the gate driver IC market focus on innovations that improve product performance and energy efficiency. Significant R&D investments developed new gate driver IC technologies that offer faster switching speeds, higher reliability, and better thermal management. Strategic collaborations with key players in industries like automotive, aerospace, and industrial automation are helping companies expand their product offerings. Many companies are diversifying their supply chains to mitigate the impact of geopolitical factors such as tariffs, while domestic production capacity meets rising demand. Moreover, companies are working to enhance their presence in emerging markets, where industrial automation and electric vehicle adoption are rapidly growing, helping to solidify their global footprint.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1.1 Supply chain reconfiguration

- 3.2.4.1.2 Pricing and product strategies

- 3.2.4.1.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growing adoption of electric and hybrid electric vehicles (EV/HEV)

- 3.3.1.2 Rising demand for renewable energy systems

- 3.3.1.3 Increasing deployment of industrial automation and robotics

- 3.3.1.4 Expansion of consumer electronics and home appliances

- 3.3.1.5 Integration of gate driver ICs in smart grid and power distribution systems

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High design complexity and integration challenges

- 3.3.2.2 Increased heat dissipation and thermal management issues

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 Pestel analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Transistor Type, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 MOSFET

- 5.3 IGBT

- 5.4 Others

Chapter 6 Market Estimates & Forecast, By Mode of Attachment, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 On-chip

- 6.3 Discrete

Chapter 7 Market Estimates & Forecast, By Isolation Type, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Isolated gate drivers

- 7.2.1 Opto-isolated

- 7.2.2 Magnetic-isolated

- 7.2.3 Capacitive-isolated

- 7.3 Non-Isolated gate drivers

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.3 Automotive

- 8.4 Energy & power

- 8.5 Telecommunications

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Allegro Microsystems

- 10.2 Analog Devices

- 10.3 Broadcom

- 10.4 Diodes Incorporated

- 10.5 Infineon Technologies

- 10.6 Littelfuse

- 10.7 Microchip Technology

- 10.8 NXP Semiconductors

- 10.9 Onsemi

- 10.10 Renesas Electronics

- 10.11 Rohm Semiconductor

- 10.12 Semikron Danfoss

- 10.13 Skyworks Solutions

- 10.14 STMicroelectronics

- 10.15 Texas Instruments

- 10.16 Toshiba

- 10.17 Vishay Intertechnology

- 10.18 Wolfspeed

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 185 Pages

- 納期

- 2~3営業日