|

市場調査レポート

商品コード

1755281

二次元遷移金属炭化物窒化物の市場機会と成長促進要因、産業動向分析、2025年~2034年予測2D Transition Metal Carbides Nitrides Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 二次元遷移金属炭化物窒化物の市場機会と成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月29日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

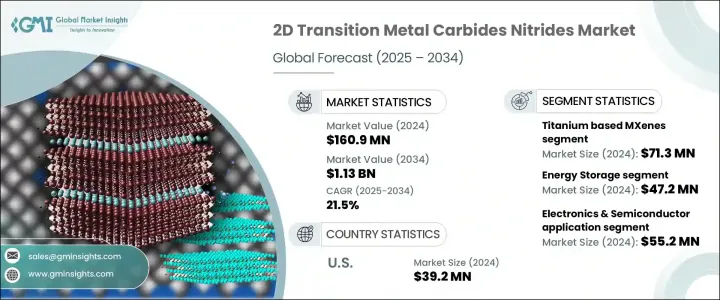

世界の二次元遷移金属炭化物窒化物市場は、2024年に1億6,090万米ドルと評価され、CAGR 21.5%で成長し、2034年には11億3,000万米ドルに達すると推定されています。

次世代エレクトロニクス、エネルギー貯蔵システム、高性能複合材料への応用が急速に進んでおり、産業全体で先端ナノ材料への需要が高まっていることが、この成長に拍車をかけています。MXENとして知られるこれらの二次元材料は、金属伝導性、構造的柔軟性、多目的な表面化学のユニークな組み合わせにより脚光を浴びています。高い導電性と機械的強度を維持しながら、その表面を設計することができるため、商業システムへの統合に特に適しています。世界の研究機関による最先端の調査と技術革新は、MXenesの商業的即応性を高め続け、複数の産業用途へのスムーズな適合を可能にしています。

チタンベースのMXenセグメントは2024年に7,130万米ドルとなり、2025~2034年の間に20.9%のCAGRを記録すると予想されています。これらのMXenは、その卓越した導電性、親水性、レイヤーバイレイヤー構造が認められており、幅広い用途に非常に適しています。高いエネルギー密度と安定性をサポートするその能力は、エネルギー貯蔵システム、電磁干渉シールド、バイオセンシング技術において価値あるコンポーネントとして位置づけられています。プロセス中の非拡散的挙動と最小限の毒性は、特にエレクトロニクスと防衛関連技術における採用の拡大をさらに後押ししています。これらの材料に対する広範な研究上の関心が商業化の努力を後押しし、影響力の大きいセグメントへの展開を加速させています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 1億6,090万米ドル |

| 予測金額 | 11億3,000万米ドル |

| CAGR | 21.5% |

エネルギー貯蔵用途セグメントでは、2024年の市場規模は4,720万米ドルで、2034年のCAGRは26.4%と予測されています。超大表面積と優れた導電性により、MXENは高性能スーパーコンデンサの理想的な候補です。その調整可能な層間間隔は、高速イオン輸送をサポートし、電気自動車や電力網のようなスケーラブルなストレージソリューションにとって極めて重要な充放電効率を高めています。サステイナブルエネルギーインフラへの世界のシフトの高まりは、効率的でスケーラブルなエネルギー貯蔵材料への需要を加速しており、MXENはその高い機能性と適応性により重要な役割を果たしています。

エレクトロニクス半導体用途セグメントは、2024年に5,520万米ドルを占め、29.6%の市場シェアを獲得し、市場推定・予測期間中のCAGRは20.7%と予測されています。MXENは、その卓越した電気的性能と調整可能な表面特性により、このセグメントでますます不可欠なものとなっています。これらの特性は、先端半導体デバイスの小型化、熱管理、回路集積の改善に貢献しています。より高速で効率的なデバイスを求める消費者の需要の高まりに後押しされた半導体セクタの継続的な拡大が、幅広い電子部品へのMXENの採用を後押ししています。

米国では、二次元遷移金属炭化物窒化物市場は2024年に3,920万米ドルと評価され、2025~2034年にかけてCAGR 21.9%で成長すると予測されています。この地域は、材料科学とナノテクノロジーにおける政府の重要な支援に加え、エレクトロニクスと防衛製造における強力な基盤から利益を得ています。これらの要因は、国内生産能力と強固な輸出入力学と相まって、米国をこの発展途上の市場における主要参入企業にしています。研究への投資、学術機関との提携、成熟した産業エコシステムの存在が、さまざまな領域でのMXenesの急速な普及をさらに後押ししています。

中国は、先端材料の主要なエンドユーザーであるクリーンエネルギーと電気自動車部門の拡大に牽引され、世界市場において強力な骨格を維持し続けています。同国は、特にアジア太平洋と欧州において、MXENをベースとする部品と技術のサプライチェーンで重要な役割を果たしています。中国は戦略的に材料革新に注力し、大規模な生産能力を有しているため、これらの新興材料に対する国内外の需要を満たすことができます。

世界的には、市場参入企業はバイオエレクトロニクス、次世代エネルギーデバイス、機能性コーティングなどのセグメントにおける研究主導型の製品開発に向けて投資を進めています。各社は、提供する材料のカスタマイズと品質を優先し、さまざまな使用事例でイノベーションを推進しています。共同開発、独自の合成方法、独占ライセンス契約は、利害関係者が競合を強化するのに役立っており、今後10年間のMXENのさらなる進歩と広範な商業利用を後押ししています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- 産業の潜在的リスク・課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向s

- 地域別

- 製品別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- サステイナブルプラクティス

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- 競合情勢

- 製品ポートフォリオと仕様

- SWOT分析

- 企業の市場シェア分析

- 企業による世界の市場シェア

- 地域市場シェア分析

- 製品ポートフォリオシェア分析

- 戦略的取り組み

- 合併と買収

- パートナーシップとコラボレーション

- 製品の発売と革新

- 拡大計画と投資

- 企業ベンチマーク

- 製品イノベーションのベンチマーク

- 価格戦略の比較

- 配電網の比較

- 顧客サービスとサポートの比較

第5章 市場推定・予測:材料別、2021~2034年

- 主要動向

- チタンベースのMXenes

- Ti3C2

- Ti2C

- Ti3CN

- その他のチタンベースのMXenes

- ニオブベースのMXenes

- ニオブ2炭素

- Nb4C3

- その他のニオブベースのMXene

- バナジウムベースのMXenes

- V2C

- V4C3

- その他のバナジウムベースのMXene

- モリブデンベースのMXenes

- モリブデンC

- その他のモリブデンベースのMXene

- タンタルベースのMXenes

- Ta4C3

- その他のタンタルベースのMXene

- その他のMXeneタイプ

第6章 市場推定・予測:合成方法別、2021~2034年

- 主要動向

- フッ化水素酸(HF)エッチング

- フッ化塩+HClエッチング

- LiF+HCl

- NaF+HCl

- KF+HCl

- その他のフッ化物塩の組み合わせ

- 電気化学エッチング

- 溶融塩エッチング

- その他の合成方法

第7章 市場推定・予測:形態別、2021~2034年

- 主要動向

- 粉末

- 分散液/インク

- 水性分散液

- 有機溶媒分散液

- その他の分散タイプ

- 膜

- 自立型フィルム

- 支援映画

- その他のフィルムタイプ

- 複合材料

- その他の形式

第8章 市場推定・予測:用途別、2021~2034年

- 主要動向

- エネルギー貯蔵

- 電池

- リチウムイオン電池

- ナトリウムイオン電池

- その他の電池タイプ

- スーパーコンデンサ

- その他のエネルギー貯蔵用途

- 電池

- エレクトロニクスとオプトエレクトロニクス

- 透明導電フィルム

- 電界効果トランジスタ

- 電磁干渉(EMI)シールド

- その他の電子機器用途

- センサとバイオセンサ

- ガスセンサ

- バイオセンサ

- 圧力/ひずみセンサ

- その他のセンサ用途

- 触媒

- 電極触媒作用

- 光触媒

- その他の触媒用途

- 環境修復

- 水の浄化

- ガス分離

- その他の環境用途

- バイオメディカル用途

- ドラッグデリバリー

- バイオイメージング

- 光熱療法

- その他の生物医療的用途

- 複合材料とコーティング

- その他

第9章 市場推定・予測:最終用途産業別、2021~2034年

- 主要動向

- エレクトロニクスと半導体

- エネルギーと電力

- ヘルスケアと医薬品

- 自動車・輸送

- 環境と水処理

- 航空宇宙と防衛

- 調査と学術

- その他

第10章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他の中東・アフリカ

第11章 企業プロファイル

- Drexel University(Technology Transfer)

- 2D Materials Pte Ltd.

- Nanochemazone

- ACS Material, LLC

- Alfa Chemistry

- American Elements

- Sigma-Aldrich(Merck KGaA)

- Ossila Ltd.

- Nanografi Nano Technology

- SkySpring Nanomaterials, Inc.

- Cheap Tubes Inc.

The Global 2D Transition Metal Carbides Nitrides Market was valued at USD 160.9 million in 2024 and is estimated to grow at a CAGR of 21.5% to reach USD 1.13 billion by 2034. The rising demand for advanced nanomaterials across industries is fueling this growth, with applications rapidly emerging in next-generation electronics, energy storage systems, and high-performance composite materials. Known as MXenes, these two-dimensional materials are gaining prominence due to their unique combination of metallic conductivity, structural flexibility, and versatile surface chemistry. The ability to engineer their surfaces while retaining high conductivity and mechanical strength makes them especially suitable for integration into commercial systems. Cutting-edge research and innovation from global institutions continue to enhance their commercial readiness, enabling the smooth adaptation of MXenes across multiple industrial applications.

The titanium-based MXenes segment stood at USD 71.3 million in 2024 and is expected to record a CAGR of 20.9% between 2025 and 2034. These MXenes are recognized for their outstanding conductivity, hydrophilic nature, and layer-by-layer structure, making them highly relevant for a wide array of applications. Their capability to support high energy density and stability positions them as valuable components in energy storage systems, electromagnetic interference shielding, and biosensing technologies. Their non-diffusive behavior during processes and minimal toxicity further support their growing adoption, particularly in electronics and defense-related technologies. The widespread research interest in these materials is driving commercialization efforts, helping accelerate their deployment across high-impact sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $160.9 million |

| Forecast Value | $1.13 billion |

| CAGR | 21.5% |

In the energy storage application segment, the market was valued at USD 47.2 million in 2024 and is projected to grow at a CAGR of 26.4% through 2034. Thanks to their ultra-large surface area and superior conductivity, MXenes are ideal candidates for high-performance supercapacitors. Their tunable interlayer spacing supports fast ion transport and enhances charge-discharge efficiency, which is crucial for scalable storage solutions such as electric vehicles and power grids. The growing global shift toward sustainable energy infrastructure is accelerating the demand for efficient and scalable energy storage materials, where MXenes play a critical role due to their high functionality and adaptability.

The electronics and semiconductor application segment accounted for USD 55.2 million in 2024, capturing a market share of 29.6%, and is estimated to register a CAGR of 20.7% during the forecast period. MXenes are increasingly indispensable in this field owing to their exceptional electrical performance and tunable surface characteristics. These attributes contribute to improved miniaturization, heat management, and circuit integration in advanced semiconductor devices. The continued expansion of the semiconductor sector, driven by growing consumer demand for faster and more efficient devices, is propelling the inclusion of MXenes in a wide range of electronic components.

In the United States, the 2D transition metal carbides nitrides market was valued at USD 39.2 million in 2024 and is projected to grow at a CAGR of 21.9% from 2025 to 2034. The region benefits from significant government backing in materials science and nanotechnology, along with a strong base in electronics and defense manufacturing. These factors, combined with domestic production capabilities and robust import-export dynamics, make the U.S. a key player in this evolving market. Investments in research, partnerships with academic institutions, and the presence of a mature industrial ecosystem further support the rapid adoption of MXenes across various domains.

China continues to maintain a strong foothold in the global market, driven by its expanding clean energy and electric vehicle sectors, which are major end-users of advanced materials. The country plays a crucial role in the supply chain for MXene-based components and technologies, particularly in the Asia Pacific and European regions. China's strategic focus on materials innovation and its large-scale production capabilities enable it to meet both domestic and international demand for these emerging materials.

Globally, leading market participants are channeling investments toward research-driven product development in areas such as bioelectronics, next-gen energy devices, and functional coatings. Companies are prioritizing customization and quality in their material offerings, pushing innovation across various use cases. Collaborative developments, proprietary synthesis methods, and exclusive licensing agreements are helping stakeholders solidify their competitive edge, fueling further advancements and broader commercial uptake of MXenes in the coming decade.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Form

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Competitive landscape

- 4.1.1 Company overview

- 4.1.2 Product portfolio and specifications

- 4.1.3 SWOT analysis

- 4.2 Company market share analysis, 2024

- 4.2.1 Global market share by company

- 4.2.2 Regional market share analysis

- 4.2.3 Product portfolio share analysis

- 4.3 Strategic initiative

- 4.3.1 Mergers and acquisitions

- 4.3.2 Partnerships and collaborations

- 4.3.3 Product launches and innovations

- 4.3.4 Expansion plans and investments

- 4.4 Company benchmarking

- 4.4.1 Product innovation benchmarking

- 4.4.2 Pricing strategy comparison

- 4.4.3 Distribution network comparison

- 4.4.4 Customer service and support comparison

Chapter 5 Market Estimates & Forecast, By Material Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Titanium based MXenes

- 5.2.1 Ti3C2

- 5.2.2 Ti2C

- 5.2.3 Ti3CN

- 5.2.4 Other Titanium based MXenes

- 5.3 Niobium based MXenes

- 5.3.1 Nb2C

- 5.3.2 Nb4C3

- 5.3.3 Other Niobium based MXenes

- 5.4 Vanadium Based MXenes

- 5.4.1 V2C

- 5.4.2 V4C3

- 5.4.3 Other Vanadium based MXenes

- 5.5 Molybdenum based MXenes

- 5.5.1 Mo2C

- 5.5.2 Other Molybdenum based MXenes

- 5.6 Tantalum based MXenes

- 5.6.1 Ta4C3

- 5.6.2 Other tantalum based MXenes

- 5.7 Other MXene types

Chapter 6 Market Estimates & Forecast, By Synthesis Method, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Hydrofluoric acid (HF) etching

- 6.3 Fluoride salt + HCl etching

- 6.3.1 LiF + HCl

- 6.3.2 NaF + HCl

- 6.3.3 KF + HCl

- 6.4 Other fluoride salt combinations

- 6.5 Electrochemical etching

- 6.6 Molten salt etching

- 6.7 Other synthesis methods

Chapter 7 Market Estimates & Forecast, By Form, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Powder

- 7.3 Dispersion/ink

- 7.3.1 Aqueous dispersions

- 7.3.2 Organic solvent dispersions

- 7.3.3 Other dispersion types

- 7.4 Film

- 7.4.1 Free standing films

- 7.4.2 Supported films

- 7.4.3 Other film types

- 7.5 Composite materials

- 7.6 Other forms

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Energy storage

- 8.2.1 Batteries

- 8.2.1.1 Lithium ion batteries

- 8.2.1.2 Sodium ion batteries

- 8.2.1.3 Other battery types

- 8.2.2 Supercapacitors

- 8.2.3 Other energy storage applications

- 8.2.1 Batteries

- 8.3 Electronics & optoelectronics

- 8.3.1 Transparent conductive films

- 8.3.2 Field effect transistors

- 8.3.3 Electromagnetic interference (emi) shielding

- 8.3.4 Other electronics applications

- 8.4 Sensors & biosensors

- 8.4.1 Gas sensors

- 8.4.2 Biosensors

- 8.4.3 Pressure/strain sensors

- 8.4.4 Other sensor applications

- 8.5 Catalysis

- 8.5.1 Electrocatalysis

- 8.5.2 Photocatalysis

- 8.5.3 Other catalytic applications

- 8.6 Environmental remediation

- 8.6.1 Water purification

- 8.6.2 Gas separation

- 8.6.3 Other environmental applications

- 8.7 Biomedical applications

- 8.7.1 Drug delivery

- 8.7.2 Bioimaging

- 8.7.3 Photothermal therapy

- 8.7.4 Other biomedical applications

- 8.8 Composites & coatings

- 8.9 Other applications

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Electronics & semiconductor

- 9.3 Energy & power

- 9.4 Healthcare & pharmaceuticals

- 9.5 Automotive & transportation

- 9.6 Environmental & water treatment

- 9.7 Aerospace & defense

- 9.8 Research & academia

- 9.9 Other end use industries

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Drexel University (Technology Transfer)

- 11.2 2D Materials Pte Ltd.

- 11.3 Nanochemazone

- 11.4 ACS Material, LLC

- 11.5 Alfa Chemistry

- 11.6 American Elements

- 11.7 Sigma-Aldrich (Merck KGaA)

- 11.8 Ossila Ltd.

- 11.9 Nanografi Nano Technology

- 11.10 SkySpring Nanomaterials, Inc.

- 11.11 Cheap Tubes Inc.