|

市場調査レポート

商品コード

1755268

ポリバッグメーラー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Polybag Mailers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ポリバッグメーラー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年05月21日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

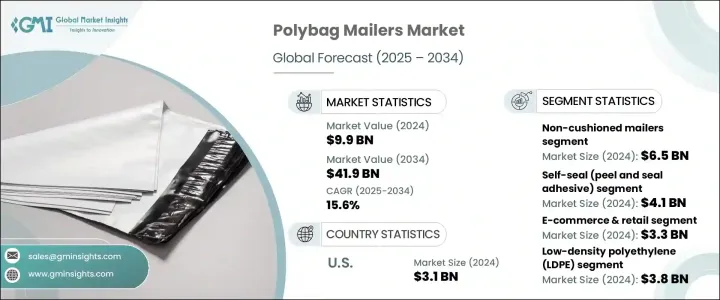

ポリバッグメーラーの世界市場規模は、2024年に99億米ドルとなり、CAGR 15.6%で成長し、2034年には419億米ドルに達すると予測されています。

米国がポリバッグメーラーを含む特定の輸入プラスチック製品に関税をかけたことで、市場は混乱しました。こうした貿易措置は輸入コストを上昇させ、サプライ・チェーンを混乱させ、小売業者や物流業者の営業経費を増加させました。国内メーカーは、海外との競合が少なくなる一方で、生産量の拡大やマテリアルハンドリング価格の上昇への対応という課題に直面しました。このシナリオにより、企業は調達先を多様化し、国内生産能力を増強するようになり、供給環境は再構築され、より弾力的になりました。

自動包装システムへの信頼の高まりが、ポリバッグメーラーの採用を後押ししています。ダブルシール粘着ストリップのような強化された製品機能は、特に電子機器、パーソナルケア、衣料品などのeコマースカテゴリーで標準になりつつあります。こうした機能アップグレードは、返品を容易にし、発送時間を短縮し、持続可能で便利な包装に対する消費者の期待の高まりに応えるものです。小包の量が増え続ける中、ブランドは効率的なロジスティクスをサポートし、顧客満足度を高めるコンパクトでオートメーション対応のメーラーを優先しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 99億米ドル |

| 予測金額 | 419億米ドル |

| CAGR | 15.6% |

材料の中では、低密度ポリエチレン(LDPE)が市場を独占し、2024年には38億米ドルを生み出しました。LDPEの手頃な価格、強度、適応性は、特にeコマースにおける中小企業にとって好ましい選択となっています。熱可塑性であるため、カスタマイズ、印刷、生産の柔軟性があります。セルフシールクロージャーと耐タンパーオプションは、今日の高まるリスク環境において不可欠な、配送中の製品セキュリティを強化します。LDPEの良好なコスト・パフォーマンス比は、拡張可能なパッケージング・ソリューションに選ばれる材料であり続けることを保証します。

製品タイプ別では、ノンクッションメーラーが最大の市場シェアを占め、2024年の市場規模は65億米ドルでした。ノンクッションメーラーの使用は、オンラインファッションや消費財の台頭とともに拡大しており、これらの商品は通常、最小限の内部保護を必要とします。これらの軽量でコスト効率の良いメーラーは、輸送費を削減し、大量の流通モデルをサポートします。新しいバリエーションには、リシーラブルクロージャーや二重粘着ストリップがあり、特にリバースロジスティクスが顧客サービスにおいて重要な役割を果たすセクターでは、合理化された返品処理をサポートしています。

米国のポリバッグメーラー市場は、ポリバッグメーラーのような軽量でフレキシブルなパッケージングソリューションへの需要の高まりにより、2024年に31億米ドルを創出しました。ポリバッグメーラーは、業務効率とフルフィルメントサイクルの短縮を重視することで、大手電子小売業者やロジスティクスプロバイダーの包装戦略の中心に位置づけられています。さらに、当日配送や翌日配送の人気が高まっていることから、企業は配送重量を減らし、ロジスティクスの敏捷性を向上させるコンパクトで費用対効果の高いパッケージを選ぶようになっています。

ポリバッグメーラーの世界市場における主なプレーヤーには、PAC Worldwide Corporation、Sealed Air、BRAVO PACK INC.、Jflexy Packaging、Crown Packaging Corp.、EcoEnclose LLC、Polycell International、Shenzhen Hongxiang Packaging Co.Ltd.、Novolex、Polypak Packaging、WH Packaging、Abriso Jiffy、ProAmpac、Pregis LLC、Intertape Polymer Group Inc.、International Plasticsなどがあります。各社は、オートメーション要件と持続可能性目標に沿ったメーラーを製造するため、研究開発に多額の投資を行っています。大手企業は、耐久性と耐タンパー性を高めながら、リサイクル可能な素材を製品ラインに組み込んでいます。多くの企業は、サプライチェーンのリスクを軽減し、需要急増への対応力を高めるため、国内での生産能力を拡大しています。さらに、eコマース・プラットフォームやサードパーティー・ロジスティクス・プロバイダーとの戦略的パートナーシップも、市場への浸透を後押ししています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- eコマース業界の急速な拡大

- 中小企業とD2Cブランドの成長

- 環境規制が材料革新を推進

- コスト効率の高いパッケージの需要の高まり

- 小売・アパレル業界での導入拡大

- 業界の潜在的リスク&課題

- 環境問題とプラスチック禁止

- リサイクルインフラのギャップ

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 低密度ポリエチレン(LDPE)

- 高密度ポリエチレン(HDPE)

- 共押出ポリエチレン

- リサイクルポリエチレン

- その他

第6章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- クッション付き封筒

- クッションなし封筒

第7章 市場推計・予測:クロージャータイプ別、2021年~2034年

- 主要動向

- セルフシール

- ヒートシール

- ジッパー/スライダーシール

- ボタンまたはタイ留め

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- eコマースと小売

- アパレル&フットウェア

- 電子機器とアクセサリー

- ヘルスケアと医薬品

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Abriso Jiffy

- BRAVO PACK INC.

- Crown Packaging Corp.

- EcoEnclose LLC

- International Plastics

- Intertape Polymer Group Inc.

- Jflexy Packaging

- Novolex

- PAC Worldwide Corporation

- Polycell International

- Polypak Packaging

- Pregis LLC

- ProAmpac

- Sealed Air

- Shenzhen Hongxiang Packaging Co., Ltd

- WH Packaging

The Global Polybag Mailers Market was valued at USD 9.9 billion in 2024 and is estimated to grow at a CAGR of 15.6% to reach USD 41.9 billion by 2034, driven by the continued surge in e-commerce, paired with increasing use across the retail and fashion industries. The market saw disruptions following US tariffs on certain imported plastic goods, including polybag mailers. These trade measures inflated import costs, disrupted supply chains, and increased operating expenses for retailers and logistics providers. While local manufacturers faced less overseas competition, they encountered challenges in scaling output and handling rising material prices. This scenario prompted businesses to diversify sourcing and ramp up domestic manufacturing capacity, leading to a reshaped and more resilient supply landscape.

Increased reliance on automated packaging systems drives polybag mailer adoption, as these products seamlessly integrate into high-speed packing lines. Enhanced product features like double-seal adhesive strips are becoming standard, particularly in e-commerce categories such as electronics, personal care, and clothing. These functional upgrades support easy returns, reduce shipping time, and meet growing consumer expectations for sustainable, convenient packaging. As parcel volumes continue to climb, brands prioritize compact, automation-ready mailers that support efficient logistics and enhance customer satisfaction.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.9 Billion |

| Forecast Value | $41.9 Billion |

| CAGR | 15.6% |

Among materials, low-density polyethylene (LDPE) dominated the market, generating USD 3.8 billion in 2024. LDPE's affordability, strength, and adaptability make it the preferred choice, especially for small and mid-sized enterprises in e-commerce. Its thermoplastic nature allows for customization, printing, and production flexibility. Self-sealing closures and tamper-resistant options enhance product security during delivery, essential in today's heightened risk environments. LDPE's favorable cost-to-performance ratio ensures it remains the material of choice for scalable packaging solutions.

By product type, non-cushioned mailers held the largest market share, valued at USD 6.5 billion in 2024. Their use has grown alongside the rise of online fashion and consumer goods, which typically require minimal interior protection. These lightweight, cost-efficient mailers help reduce shipping expenses and support high-volume distribution models. Newer variations include resealable closures and dual adhesive strips to support streamlined return handling, especially in sectors where reverse logistics play a critical role in customer service.

United States Polybag Mailers Market generated USD 3.1 billion in 2024, driven by the increasing demand for lightweight, flexible packaging solutions like polybag mailers. Focusing on operational efficiency and faster fulfillment cycles has placed polybag mailers at the center of packaging strategies for major e-retailers and logistics providers. In addition, the rising popularity of same-day and next-day deliveries is pushing companies to opt for compact, cost-effective packaging that reduces shipping weight and improves logistics agility.

Key players in the Global Polybag Mailers Market include PAC Worldwide Corporation, Sealed Air, BRAVO PACK INC., Jflexy Packaging, Crown Packaging Corp., EcoEnclose LLC, Polycell International, Shenzhen Hongxiang Packaging Co., Ltd, Novolex, Polypak Packaging, WH Packaging, Abriso Jiffy, ProAmpac, Pregis LLC, Intertape Polymer Group Inc., and International Plastics. Companies invest heavily in R&D to produce mailers that align with automation requirements and sustainability goals. Major players are integrating recycled and recyclable materials into their product lines while enhancing durability and tamper resistance. Many firms are expanding production capabilities domestically to reduce supply chain risks and improve responsiveness to demand spikes. Additionally, strategic partnerships with e-commerce platforms and third-party logistics providers are helping boost market penetration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and Future Considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rapid expansion of e-commerce industry

- 3.3.1.2 Growth of SMEs and D2C brands

- 3.3.1.3 Environmental regulations driving material innovation

- 3.3.1.4 Growing demand for cost effective packaging

- 3.3.1.5 Increasing adoption in retail and apparel industry

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Environmental concerns and plastic bans

- 3.3.2.2 Recycling infrastructure gaps

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Million & Million Units)

- 5.1 Key trends

- 5.2 Low-density polyethylene (LDPE)

- 5.3 High-density polyethylene (HDPE)

- 5.4 Co-extruded polyethylene

- 5.5 Recycled polyethylene

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Product, 2021 – 2034 (USD Million & Million Units)

- 6.1 Key trends

- 6.2 Cushioned mailers

- 6.3 Non-cushioned mailers

Chapter 7 Market Estimates and Forecast, By Closure Type, 2021 – 2034 (USD Million & Million Units)

- 7.1 Key trends

- 7.2 Self-seal

- 7.3 Heat seal

- 7.4 Zip/slider seal

- 7.5 Button or tie closure

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million & Million Units)

- 8.1 Key trends

- 8.2 E-commerce & retail

- 8.3 Apparel & footwear

- 8.4 Electronics & accessories

- 8.5 Healthcare & pharmaceuticals

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abriso Jiffy

- 10.2 BRAVO PACK INC.

- 10.3 Crown Packaging Corp.

- 10.4 EcoEnclose LLC

- 10.5 International Plastics

- 10.6 Intertape Polymer Group Inc.

- 10.7 Jflexy Packaging

- 10.8 Novolex

- 10.9 PAC Worldwide Corporation

- 10.10 Polycell International

- 10.11 Polypak Packaging

- 10.12 Pregis LLC

- 10.13 ProAmpac

- 10.14 Sealed Air

- 10.15 Shenzhen Hongxiang Packaging Co., Ltd

- 10.16 WH Packaging