|

市場調査レポート

商品コード

1755266

鉄道用すべり軸受の市場機会、成長促進要因、産業動向分析、2025~2034年予測Railway Sliding Bearing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 鉄道用すべり軸受の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年05月30日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

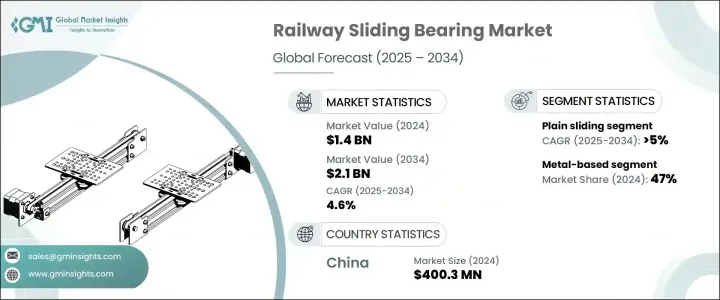

鉄道用すべり軸受の世界市場規模は、2024年に14億米ドルとなり、CAGR 4.6%で成長し、2034年には21億米ドルに達すると予測されています。

この成長は、世界の鉄道インフラプロジェクトの拡大と、高速鉄道システムの人気の高まりによるところが大きいです。輸送セグメントがより速く、より効率的で、よりサステイナブルソリューションへとシフトするにつれ、すべり軸受は最新の鉄道ネットワークに不可欠な部品となってきています。これらの軸受は、もはや基本的な機械部品とはみなされず、性能、安全性、信頼性を確保する上で重要な役割を果たしています。

各国が貨物通路、地下鉄、高速旅客線に多額の投資を行う中、過酷な運転条件に耐えるよう設計された高品位すべり軸受への信頼が高まっています。これには、高荷重、極端な速度、変動する環境ストレスなどが含まれます。すべり軸受は産業とともに進化しており、新材料、デジタル診断、輸送効率とインフラの回復力を向上させるという幅広い目標に沿った構造的進歩を取り入れています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 14億米ドル |

| 予測金額 | 21億米ドル |

| CAGR | 4.6% |

最小限のメンテナンス、優れた車軸効率、先進的な台車プラットフォームとの統合の必要性から、高性能軸受システムの需要が高まっています。メーカーは、複合材料を利用し、スマートモニタリング機能を組み込み、長期信頼性を高める革新的な軸受ソリューションを開発することで対応しています。このような変化により、すべり軸受セグメントは、インテリジェントで未来に対応した鉄道システムの進化を支える、技術先進の市場セグメントへと変貌を遂げつつあります。世界の鉄道戦略がスピード、持続可能性、耐久性にますます重点を置くようになっているため、軸受プロバイダはこれらの期待に応えるべく製品を適合させており、最新の鉄道エコシステムにおける価値を強化しています。

2024年、すべり軸受セグメントは27%のシェアを占め、2034年までCAGR 5%で成長すると予測されています。これらの軸受は、貨物鉄道と旅客鉄道の運行において重要な役割を果たし、アキシャル荷重とラジアル荷重の処理に不可欠なサポートを提供し、機械的摩擦を低減し、部品のスムーズな動きを促進します。信頼性の高い構造、コスト効率の高い製造、荷重処理能力により、すべり軸受は、さまざまな鉄道車両クラスの台車、ブレーキアセンブリー、サスペンション機構に使用され、好まれています。すべり軸受の効率は、列車の安定性向上やダウンタイムの短縮に直接貢献するため、鉄道産業では欠かせないものとなっています。

金属ベースのすべり軸受は2024年に47%のシェアを占め、2025~2034年にかけてCAGR 5%で成長する見込みです。これらの軸受は、卓越した機械的耐久性、耐摩耗性、耐熱性で知られており、厳しい鉄道環境に最適です。メタルベースのオプションは、アクスルサポートからサスペンションジョイント、ブレーキシステムまで、幅広い用途に使用されています。高速・高負荷条件下での信頼性の高い性能は、特にインフラのアップグレードが加速している市場で、その普及を後押しし続けています。大規模な貨物輸送や高速ネットワークに投資している地域では、長寿命と堅牢な構造上の利点を持つこの軸受に特に注目しています。

中国の鉄道用すべり軸受2024年のシェアは63.3%、市場規模は4億30万米ドル。同国の優位性は、貨物、地下鉄、高速鉄道の運行を網羅する、その広範な鉄道開発戦略に起因します。鉄道車両の規模と継続的なインフラ投資により、先進的なすべり軸受への需要が高まっています。地元の軸受メーカーは、国内と世界のプロジェクト要件に適合する高性能、自己潤滑性、耐腐食性のコンポーネントを製造する能力を強化しています。洗練された材料、厳しい公差のエンジニアリング、メンテナンスしやすい機能を使用し、中国はこの産業のこのセグメントでペースを作り続けています。

鉄道用すべり軸受の世界市場参入企業には、ジェイテクト、ティムケン、ミネベアミツミ、NTN、日本精工、GGB、ZKLグループ、シェフラーグループ、リーヘルグループ、AB SKFなどがあります。鉄道用すべり軸受セグメントでの市場ポジションを強化するため、各社は技術革新、材料の進歩、世界展開に注力しています。主要な戦略のひとつは、複合材料や自己潤滑性材料を使用した高性能軸受の開発であり、これによりメンテナンスを削減し、過酷な運転条件下での耐久性を向上させています。各社はまた、進化する台車技術に対応する耐荷重とシステム互換性を高めるため、精密エンジニアリングにも投資しています。鉄道OEMやインフラプロバイダとのコラボレーションにより、各社は特定の鉄道車両要件に対応するソリューションをカスタマイズしています。さらに、鉄道開発が進む市場でも、メーカー各社は足跡を広げています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主要動向

- 一次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- 鉄道インフラプロジェクトの拡大

- 高速鉄道の需要の高まり

- 貨物輸送の増加

- 軸受材料の技術的進歩

- 産業の潜在的リスク・課題

- 先進的軸受の初期コストが高め

- 厳格な品質基準と認証

- 市場機会

- 都市交通システムの拡大

- 予知保全のためのスマート軸受の採用

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向s

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- サステイナブルプラクティス

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

- カーボンフットプリントの考慮

- ユースケース

- 最良のシナリオ

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画と資金調達

第5章 市場推定・予測:製品別、2021~2034年

- 主要動向

- プレーンスライド

- 球面スライド

- 円筒形スライド

- フランジ付きスライド

- スラストスライド

- カスタム/複合材料

第6章 市場推定・予測:材料別、2021~2034年

- 主要動向

- 金属ベース

- ポリマーベース

- 複合材料軸受

- セラミックベース

第7章 市場推定・予測:電車別、2021~2034年

- 主要動向

- 貨物列車

- 旅客列車

- 高速列車

- ライトレール/トラム

- 地下鉄

- モノレール

第8章 市場推定・予測:流通チャネル別、2021~2034年

- 主要動向

- 直接販売

- 販売代理店

- オンラインプラットフォーム

第9章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- AB SKF

- ABC Bearings

- Beijing Bearing Manufacturing

- Boca Bearings

- China Railway Rolling Stock Corporation(CRRC)

- Emerson Bearing Company

- FAG Bearings

- GGB

- JTEKT Corporation

- Liebherr Group

- MinebeaMitsumi

- NSK

- NTN Industrial Bearings

- Rexnord Corporation

- RHP Bearings

- Schaeffler Group

- SKF USA

- Taikisha

- Timken Aerospace Bearings

- ZKL Group

The Global Railway Sliding Bearing Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 2.1 billion by 2034. This growth is largely driven by expanding rail infrastructure projects worldwide and the increasing popularity of high-speed rail systems. As the transportation sector shifts toward faster, more efficient, and more sustainable solutions, sliding bearings are becoming essential components in modern rail networks. These bearings are no longer regarded as basic mechanical parts-they now play a critical role in ensuring performance, safety, and reliability.

With countries investing heavily in freight corridors, metro rail, and high-speed passenger lines, there is a growing reliance on high-grade sliding bearings designed to withstand intense operational conditions. These include heavy loads, extreme speeds, and fluctuating environmental stresses. Sliding bearings are evolving alongside the industry, incorporating new materials, digital diagnostics, and structural advancements that align with broader goals of improving transportation efficiency and infrastructure resilience.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.1 Billion |

| CAGR | 4.6% |

The demand for high-performance bearing systems is rising due to the need for minimal maintenance, superior axle efficiency, and integration with advanced bogie platforms. Manufacturers are responding by developing innovative bearing solutions that utilize composite materials, incorporate smart monitoring features, and enhance long-term reliability. These changes are transforming the sliding bearing segment into a technology-forward market segment, supporting the evolution of intelligent and future-ready railway systems. As global rail strategies increasingly focus on speed, sustainability, and durability, bearing providers are adapting their offerings to meet these expectations, reinforcing their value in the modern rail ecosystem.

In 2024, the plain sliding bearings segment held a 27% share and is projected to grow at a CAGR of 5% throughout 2034. These bearings serve critical roles in freight and passenger rail operations, offering essential support for handling axial and radial loads, reducing mechanical friction, and facilitating smooth component movement. With their reliable structure, cost-effective manufacturing, and load-handling capability, plain sliding bearings remain a favored option for use in bogies, brake assemblies, and suspension mechanisms across various rail vehicle classes. Their efficiency contributes directly to improved train stability and reduced downtime, making them indispensable in the rail industry.

Metal-based sliding bearings represented 47% share in 2024 and are also expected to grow at a CAGR of 5% from 2025 - 2034. These bearings are known for their exceptional mechanical durability, wear resistance, and heat tolerance, making them ideal for rigorous rail environments. Metal-based options are widely implemented in applications ranging from axle supports to suspension joints and brake systems. Their reliable performance under high-speed and heavy-load conditions continues to drive their widespread use, particularly in markets where infrastructure upgrades are accelerating. Regions investing in large-scale freight and high-speed networks are particularly focused on these bearings for their extended lifespan and robust structural benefits.

China Railway Sliding Bearing Market held a 63.3% share and generated USD 400.3 million in 2024. The country's dominance stems from its expansive rail development strategy, which encompasses freight, metro, and high-speed train operations. The scale of its rolling stock and continued infrastructure investments have driven consistent demand for advanced sliding bearings. Local bearing manufacturers are enhancing their capabilities to produce high-performance, self-lubricating, and corrosion-resistant components that align with both domestic and global project requirements. Using sophisticated materials, tight-tolerance engineering, and maintenance-friendly features, China continues to set the pace in this segment of the industry.

Key industry participants in the Global Railway Sliding Bearing Market include JTEKT, The Timken Company, MinebeaMitsumi, NTN, NSK, GGB, ZKL Group, Schaeffler Group, Liebherr Group, and AB SKF. To strengthen their market position in the railway sliding bearing sector, companies are focusing on innovation, material advancement, and global expansion. One major strategy is the development of high-performance bearings using composite and self-lubricating materials that reduce maintenance and improve durability under extreme operating conditions. Firms are also investing in precision engineering to enhance load-bearing capacity and system compatibility with evolving bogie technologies. Collaborations with rail OEMs and infrastructure providers allow companies to customize solutions for specific rolling stock requirements. Additionally, manufacturers are expanding their footprint in emerging markets with strong rail development agendas.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Material

- 2.2.4 Train

- 2.2.5 Sales channel

- 2.2.6 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of rail infrastructure projects

- 3.2.1.2 Rising demand for high-speed rail

- 3.2.1.3 Increasing freight transportation

- 3.2.1.4 Technological advancements in bearing materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost of advanced bearings

- 3.2.2.2 Stringent quality standards & certifications

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of urban mobility systems

- 3.2.3.2 Adoption of smart bearings for predictive maintenance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.10 Export and import

- 3.11 Cost breakdown analysis

- 3.12 Patent analysis

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Use cases

- 3.15 Best-case scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Plain sliding

- 5.3 Spherical sliding

- 5.4 Cylindrical sliding

- 5.5 Flanged sliding

- 5.6 Thrust sliding

- 5.7 Custom/Composite

Chapter 6 Market Estimates & Forecast, By Material, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Metal-based

- 6.3 Polymer-based

- 6.4 Composite bearings

- 6.5 Ceramic-based

Chapter 7 Market Estimates & Forecast, By Train, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Freight trains

- 7.3 Passenger trains

- 7.4 High-Speed trains

- 7.5 Light Rail/Trams

- 7.6 Metro/Subway systems

- 7.7 Monorails

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Distributors/Dealers

- 8.4 Online platforms

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AB SKF

- 11.2 ABC Bearings

- 11.3 Beijing Bearing Manufacturing

- 11.4 Boca Bearings

- 11.5 China Railway Rolling Stock Corporation (CRRC)

- 11.6 Emerson Bearing Company

- 11.7 FAG Bearings

- 11.8 GGB

- 11.9 JTEKT Corporation

- 11.10 Liebherr Group

- 11.11 MinebeaMitsumi

- 11.12 NSK

- 11.13 NTN Industrial Bearings

- 11.14 Rexnord Corporation

- 11.15 RHP Bearings

- 11.16 Schaeffler Group

- 11.17 SKF USA

- 11.18 Taikisha

- 11.19 Timken Aerospace Bearings

- 11.20 ZKL Group