|

市場調査レポート

商品コード

1755254

化学アンカー市場の機会、成長促進要因、産業動向分析、2025年~2034年予測Chemical Anchors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 化学アンカー市場の機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月29日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

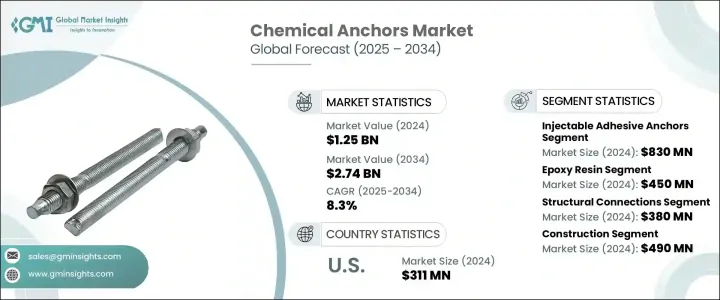

化学アンカーの世界市場規模は、2024年に12億5,000万米ドルとなり、CAGR 8.3%で成長し、2034年には27億4,000万米ドルに達すると予測されています。

この成長は、世界の建設活動の増加によるところが大きいです。都市人口が拡大し、都市が急速に発展するにつれて、高度な建設技術と近代的なインフラに対する需要が高まり続けています。これに対応するため、化学アンカーは、さまざまな複雑さや大きさの建築物において、さまざまな構造要素を固定するための不可欠な部品となっています。これらのアンカーソリューションは、構造用途において強力で長持ちする結合を提供し、住宅、商業、工業の各分野で支持を集めています。

都市化が進むにつれ、厳しい環境下でも性能と安全性を確保できるアンカーシステムの必要性が高まっています。より複雑な構造物が建設され、持続可能性への注目が高まる中、エンジニアや請負業者は、信頼性の高いファスナーとして化学アンカーに注目しています。化学アンカーは、特にコンクリートや鉄筋に高い強度で接着することができるため、インフラ開発や改修プロジェクトに採用されることが世界的に増えています。動的・静的荷重に対応できるため、特に現代の建設要件に適しています。各社は現在、厳しい安全基準を満たす高性能アンカーソリューションの製造に注力しており、多様な用途での採用が進んでいます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 12億5,000万米ドル |

| 予測金額 | 27億4,000万米ドル |

| CAGR | 8.3% |

製品タイプ別に見ると、市場は注射用接着性アンカー、カプセル接着性アンカー、化学アンカー固定具に区分されます。注射用接着性アンカー分野は、2024年の評価額が8億3,000万米ドルで市場をリードし、2034年までCAGR 8.9%で成長すると予想されています。その優位性は、使いやすさ、複数の建設用途における汎用性、要求の厳しい場面での優れた性能に起因しています。これらのアンカーは、正確な耐荷重性能と迅速な施工時間が要求される分野でも、強力で安定した接着を提供する能力で支持されています。樹脂配合の技術的進歩も、より速い硬化と信頼性の向上を可能にし、人気上昇に貢献しています。

樹脂の種類別では、市場はビニルエステル樹脂、エポキシアクリレート、エポキシ樹脂、ポリエステル樹脂、ハイブリッドシステムに分類されます。エポキシ樹脂セグメントは2024年に4億5,000万米ドルと評価され、予測期間中にCAGR 9%で拡大すると予測されています。エポキシ樹脂ベースの化学アンカーは、高い機械的強度、化学薬品に対する優れた耐性、高負荷環境下での信頼性の高い接着性により、重建設環境で広く好まれています。また、これらの樹脂は硬化が速く、極端な環境条件下でも優れた性能を発揮するため、構造的完全性が重要なプロジェクトでは最適な選択肢となります。

用途別に分析すると、市場には構造用接合部、鉄筋接合部、重機取り付け、ファサード取り付け、手すりと安全バリア、耐震補強、その他が含まれます。構造用接合部は2024年に3億8,000万米ドルを記録し、2025年から2034年にかけてCAGR 8.8%で成長すると予測されています。この分野は、幅広い建築形式において安定性と安全性を確保する上で重要な役割を果たすため、大きなシェアを占めています。高層ビルや近代的なインフラシステムの進化に伴い、構造接合部における強力なアンカーソリューションの需要は着実に伸びています。このような用途に化学アンカーを使用することで、荷重を確実に伝達し、周囲の材料への影響を最小限に抑えることができます。

建設分野は2024年に4億9,000万米ドルで最大の最終用途産業として浮上し、CAGR 7.8%で成長し、39.5%の市場シェアを獲得すると予測されています。急速な都市開発の動向、商業用不動産の拡大、安全で持続可能な建設慣行への注目の高まりなどが、このセグメントの隆盛に寄与しています。建築業者や開発業者は、その適応性、強度、近代的建築要件への適合性から、化学アンカーへの信頼を高めています。設計の複雑化と構造高さの上昇が続く中、信頼性の高いアンカー・ソリューションへのニーズは引き続き高いです。

地域別では、米国の化学アンカー市場は2024年に3億1,100万米ドルとなり、2034年までCAGR 8%で成長すると予測されています。インフラのアップグレードの増加と耐震補強基準の採用が需要を促進しています。さらに、建設規制の更新や住宅・商業施設の改修投資の増加も市場成長を支えています。トップメーカーの技術強化やイノベーションも、化学アンカーの応用範囲を拡大し、市場浸透の新たな機会を提供しています。

業界をリードする企業は、絶え間ない技術革新、ブランド開発、幅広い国際流通チャネルを通じて競争力を維持しています。これらの企業は、優れた耐荷重性、硬化時間の短縮、さまざまな環境条件下での信頼性の高い性能を提供する高度な配合物の製造に注力しています。持続可能性と世界の安全基準への準拠を重視する大手メーカーは、製品ラインを進化する規制要件に合わせています。さらに、パートナーシップ、合併、戦略的買収を通じた拡大努力により、新興市場および成熟市場で存在感を強めています。この業界はまた、専門的な技術サポート、高度なトレーニングプログラム、多様な建設ニーズに合わせた統合ソリューションによって形成されています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向s

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)

(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 注入型接着アンカー

- カプセル接着アンカー

- 化学アンカー固定具

第6章 市場推計・予測:樹脂の種類別、2021年~2034年

- 主要動向

- エポキシ樹脂

- エポキシアクリレート

- ポリエステル樹脂

- ビニルエステル樹脂

- ハイブリッドシステム

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 構造的接続

- 鉄筋接合部

- 重機の取り付け

- ファサードの設置

- 手すりと安全柵

- 耐震補強

- その他

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 建設

- 住宅用

- 商業用

- 産業用

- インフラ

- 高速道路と橋

- ダムとトンネル

- 鉄道

- その他

- 製造業

- 海洋およびオフショア

- 石油・ガス

- 鉱業

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東およびアフリカ

第10章 企業プロファイル

- Hilti Corporation

- Sika AG

- Simpson Strong-Tie Company, Inc.

- Illinois Tool Works Inc.(ITW)

- BASF SE

- 3M Company

- Henkel AG &Co. KGaA

- Fischer Group

- Powers Fasteners(Stanley Black &Decker)

- MKT Fastening LLC

- DEWALT(Stanley Black &Decker)

- Mapei S.p.A.

- Rawlplug

- EJOT Holding GmbH &Co. KG

- CELO Fixings

- Chemfix Products Ltd

- FIXDEX Fastening Technology

- Evonik Industries AG

- Good Use Hardware Co., Ltd.

- Ripple Construction Products Pvt Ltd.

The Global Chemical Anchors Market was valued at USD 1.25 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 2.74 billion by 2034. This growth is largely driven by the increasing volume of construction activity worldwide. As urban populations expand and cities develop rapidly, the demand for advanced construction techniques and modern infrastructure continues to rise. In response, chemical anchors are becoming essential components for securing various structural elements in buildings of varying complexity and size. These anchoring solutions provide strong, long-lasting bonds in structural applications and are gaining traction across residential, commercial, and industrial sectors.

As urbanization intensifies, there is a growing need for anchoring systems that ensure both performance and safety in demanding environments. With more complex structures being built and an increased focus on sustainability, engineers and contractors are turning to chemical anchors for reliable fastening. They are particularly effective in delivering high-strength adhesion to concrete and reinforcement bars, which is why they are being increasingly adopted in infrastructure development and renovation projects globally. Their ability to handle dynamic and static loads makes them especially suitable for modern-day construction requirements. Companies are now concentrating on manufacturing high-performance anchoring solutions that meet stringent safety standards, driving adoption across diverse applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.25 billion |

| Forecast Value | $2.74 billion |

| CAGR | 8.3% |

In terms of product types, the market is segmented into injectable adhesive anchors, capsule adhesive anchors, and chemical anchor fixings. The injectable adhesive anchors segment led the market in 2024 with a valuation of USD 830 million and is expected to grow at a CAGR of 8.9% through 2034. Its dominance is attributed to its ease of use, versatility across multiple construction applications, and superior performance in demanding scenarios. These anchors are favored for their ability to provide strong, consistent bonding, even in areas that require precise load-bearing performance and fast installation times. Technological advancements in resin formulations have also contributed to their rising popularity by enabling faster curing and improved reliability.

Based on resin types, the market is categorized into vinyl ester resin, epoxy acrylate, epoxy resin, polyester resin, and hybrid systems. The epoxy resin segment was valued at USD 450 million in 2024 and is anticipated to expand at a CAGR of 9% during the forecast period. Epoxy-based chemical anchors are widely preferred in heavy construction environments due to their high mechanical strength, excellent resistance to chemicals, and dependable bonding in high-load settings. These resins also offer rapid curing capabilities and perform well under extreme environmental conditions, making them the go-to option in projects where structural integrity is critical.

When analyzed by application, the market includes structural connections, rebar connections, heavy equipment mounting, facade installations, handrails and safety barriers, seismic retrofitting, and others. The structural connections segment recorded a value of USD 380 million in 2024 and is projected to grow at a CAGR of 8.8% from 2025 to 2034. This segment holds a significant share as it fulfills a crucial role in ensuring stability and safety across a broad range of construction formats. With the evolution of high-rise buildings and modern infrastructure systems, the demand for strong anchoring solutions in structural joints is growing steadily. The use of chemical anchors in these applications allows for secure load transfer and minimal disruption to surrounding materials.

The construction segment emerged as the largest end-use industry in 2024, valued at USD 490 million, and is forecasted to grow at a CAGR of 7.8%, capturing a market share of 39.5%. The growing trend of rapid urban development, expansion in commercial real estate, and increased focus on safe and sustainable construction practices have all contributed to the segment's prominence. Builders and developers increasingly rely on chemical anchors for their adaptability, strength, and compatibility with modern construction requirements. As design complexity and structural heights continue to rise, the need for reliable anchoring solutions will remain high.

In terms of regional performance, the United States chemical anchors market was valued at USD 311 million in 2024 and is anticipated to grow at a CAGR of 8% through 2034. The rise in infrastructure upgrades, coupled with the increasing adoption of seismic retrofitting standards, is fueling demand. Additionally, market growth is supported by updates in construction regulations and rising investments in residential and commercial renovations. Technological enhancements and innovations from top manufacturers are also expanding the application scope of chemical anchors, offering new opportunities for market penetration.

Leading industry players maintain a competitive edge through continuous innovation, brand development, and broad international distribution channels. These companies focus on producing advanced formulations that offer superior load-bearing capabilities, faster curing times, and reliable performance under varying environmental conditions. With an emphasis on sustainability and compliance with global safety standards, major manufacturers are aligning their product lines with evolving regulatory requirements. Moreover, expansion efforts through partnerships, mergers, and strategic acquisitions are enabling them to strengthen their presence across emerging and mature markets. The industry is also shaped by specialized technical support, advanced training programs, and integrated solutions tailored to diverse construction needs.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Resin type

- 2.2.4 Application

- 2.2.5 End use industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Injectable adhesive anchors

- 5.3 Capsule adhesive anchors

- 5.4 Chemical anchor fixings

Chapter 6 Market Estimates & Forecast, By Resin Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Epoxy resin

- 6.3 Epoxy acrylate

- 6.4 Polyester resin

- 6.5 Vinyl ester resin

- 6.6 Hybrid systems

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Structural connections

- 7.3 Rebar connections

- 7.4 Heavy equipment mounting

- 7.5 Facade installations

- 7.6 Handrails and safety barriers

- 7.7 Seismic retrofitting

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Construction

- 8.2.1 Residential

- 8.2.2 Commercial

- 8.2.3 Industrial

- 8.3 Infrastructure

- 8.3.1 Highways and bridges

- 8.3.2 Dams and tunnels

- 8.3.3 Railways

- 8.3.4 Others

- 8.4 Manufacturing

- 8.5 Marine and offshore

- 8.6 Oil & gas

- 8.7 Mining

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Hilti Corporation

- 10.2 Sika AG

- 10.3 Simpson Strong-Tie Company, Inc.

- 10.4 Illinois Tool Works Inc. (ITW)

- 10.5 BASF SE

- 10.6 3M Company

- 10.7 Henkel AG & Co. KGaA

- 10.8 Fischer Group

- 10.9 Powers Fasteners (Stanley Black & Decker)

- 10.10 MKT Fastening LLC

- 10.11 DEWALT (Stanley Black & Decker)

- 10.12 Mapei S.p.A.

- 10.13 Rawlplug

- 10.14 EJOT Holding GmbH & Co. KG

- 10.15 CELO Fixings

- 10.16 Chemfix Products Ltd

- 10.17 FIXDEX Fastening Technology

- 10.18 Evonik Industries AG

- 10.19 Good Use Hardware Co., Ltd.

- 10.20 Ripple Construction Products Pvt Ltd.