|

市場調査レポート

商品コード

1755251

光衛星の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Optical Satellite Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 光衛星の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月23日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

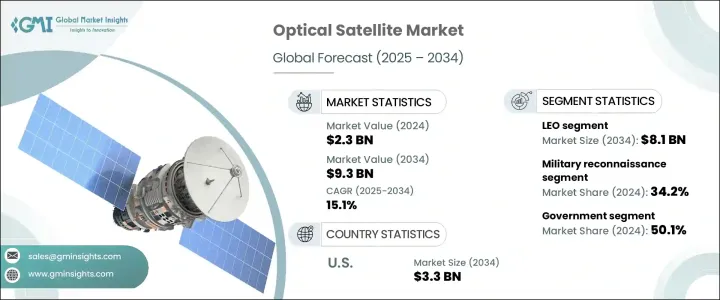

世界の光衛星市場は、2024年には23億米ドルと評価され、特に地球観測と監視アプリケーションのための商業衛星サービスの需要増加に牽引され、CAGR 15.1%で成長し、2034年には93億米ドルに達すると推定されています。

光学衛星が軌道上で普及するにつれて、メーカーは生産コストの上昇に結びついた新たなハードルに直面しています。最近の関税政策により、半導体、精密光学センサー、航空宇宙グレードの材料などの重要部品にコスト圧力がかかり、多くのメーカーは国内調達に軸足を移さざるを得なくなっています。このシフトは、資本支出の増加とプロジェクトスケジュールの延長をもたらし、すでに複雑な衛星生産サイクルを管理している企業に負担を強いています。さらに、サプライチェーンの混乱が続いているため、遅延や予算超過が発生し、安定した生産が課題となっています。

高解像度の地球観測(EO)画像に対する需要の高まりは、衛星・宇宙産業の運用状況を急速に変化させています。環境監視、インフラ開発、災害管理、農業分析などの用途で、商業部門と公共部門の両方が現在、高精細光学画像に大きく依存しています。精密農業は特にこのような能力の恩恵を受けており、衛星はマルチスペクトル画像を通して土壌の健康状態、作物の成長、土地利用について実用的な洞察を提供しています。これらの衛星は、ほぼリアルタイムのデータ配信を可能にし、農作業の精度と効率を向上させ、世界のアグリテック市場での採用をさらに後押ししています。画像処理能力の向上と、実用的なデータの迅速な取得が相まって、光衛星の導入需要が高まり続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 23億米ドル |

| 予測金額 | 93億米ドル |

| CAGR | 15.1% |

低軌道(LEO)セグメントは、2034年までに81億米ドルに達する見込みです。LEOは地球に近いため、特に高解像度の地表イメージングを必要とするミッションでは、光学衛星を配備するのに適した軌道となっています。政府が支援するイニシアティブは、民間セクターの能力と統合して、ターゲットを絞った衛星配備を支援しています。これらの協力関係は、地形分析、気候モデリング、戦略的諜報活動のための詳細な画像を収集し、市場拡大におけるLEOセグメントの影響力を強化しています。

作物監視アプリケーションは、正確な農業診断の重要性の高まりを背景に、2034年までに23億米ドルに達すると予想されています。光学衛星は、マルチスペクトル画像を使って作物ストレスの初期兆候を検出し、収量減を防ぐのに役立っています。精密農業の成長とデジタル農業の進歩が相まって、リアルタイムの洞察を提供し、土地管理戦略の最適化を支援するEO対応ソリューションへの需要が高まり続けています。

英国の光衛星市場は、2034年までCAGR 14.1%で成長すると予測されています。英国政府による地球観測技術への継続的な投資により、衛星ベースのモニタリングに新たな機会が生まれています。環境の変化を追跡し、監視システムを強化し、気候の回復力と持続可能性をめぐる政策に情報を提供するために使用される高品質の画像ソリューションに対する国家需要が増加しています。

世界の光衛星市場の主要企業には、Lockheed Martin Corporation, Airbus, Thales Alenia Space, and Maxar Technologiesなどがあります。これらの企業は、市場での存在感を維持し、成長させるために戦略的施策を実施しています。主な焦点は、衛星フリートの拡大と高度な光学系による画像解像度能力の向上にあります。これらの企業は、政府機関や民間宇宙企業との共同プログラムに投資して、長期契約を確保し、次世代システムを共同開発しています。多額の研究開発費、部品の現地調達、製造の合理化努力は、材料費の高騰や製造上の課題への対応に役立っています。さらに、多くの企業がソフトウェアプラットフォームを強化し、より高速な画像処理と分析統合をサポートすることで、エンドユーザーにより大きな価値を提供しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 促進要因

- 高解像度の地球観測データに対する需要の高まり

- 国家安全保障と監視への投資の増加

- 商用衛星の急速な成長

- 画像処理とデータ処理における技術の進歩

- 気候変動監視と環境保護の取り組みの拡大

- 業界の潜在的リスク&課題

- 高い資本コストと運用コスト

- データの過負荷と処理の複雑さ

- 貿易への影響

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:軌道タイプ別、2021年~2034年

- 主要動向

- LEO

- MEO

- GEO

- その他

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 軍事偵察

- 作物の監視

- 都市計画

- 災害管理

- 鉱物マッピング

- 環境モニタリング

- その他

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 政府用

- 商業用

- アカデミック用

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Airbus

- China Aerospace Science and Technology Corp.

- Elbit Systems

- Hanwha Group

- Israeli Aerospace Industry

- ISRO

- Lockheed Martin Corporation

- Maxar Technologies

- Mitsubishi Electric Corporation

- OHB SE

- Satellogic

- Surrey Satellite Technology Ltd

- Thales Alenia Space

- Turksat

The Global Optical Satellite Market was valued at USD 2.3 billion in 2024 and is estimated to grow at a CAGR of 15.1% to reach USD 9.3 billion by 2034, driven by increasing demand for commercial satellite services, particularly for Earth observation and surveillance applications. As optical satellites become more prevalent in orbit, manufacturers are facing new hurdles tied to escalating production costs. Recent tariff policies have created cost pressures on critical components such as semiconductors, precision optical sensors, and aerospace-grade materials, forcing many manufacturers to pivot toward domestic sourcing. This shift has resulted in rising capital expenditure and extended project timelines, adding strain to companies already managing complex satellite production cycles. Additionally, persistent supply chain disruptions are causing delays and budget overruns, presenting a challenge for consistent output.

Heightened demand for high-resolution Earth Observation (EO) imagery is rapidly transforming the operational landscape of the satellite and space industry. Both commercial and public sectors now rely heavily on high-detail optical imaging for applications like environmental monitoring, infrastructure development, disaster management, and agricultural analysis. Precision farming has especially benefited from these capabilities, with satellites offering actionable insights on soil health, crop growth, and land use through multispectral imaging. These satellites allow for nearly real-time data delivery, improving the accuracy and efficiency of agricultural operations and further fueling adoption across global agritech markets. Enhanced imaging capabilities combined with quick turnaround times for actionable data continue to push the demand for optical satellite deployment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $9.3 Billion |

| CAGR | 15.1% |

The Low Earth Orbit (LEO) segment is poised to reach USD 8.1 billion by 2034. Its proximity to Earth makes LEO a preferred orbit for deploying optical satellites, especially for missions requiring high-resolution surface imaging. Government-backed initiatives integrated with private sector capabilities to support targeted satellite deployments. These collaborations gather detailed imagery for terrain analysis, climate modeling, and strategic intelligence, reinforcing the LEO segment's influence on market expansion.

The crop monitoring application is expected to hit USD 2.3 billion by 2034, backed by the rising importance of accurate agricultural diagnostics. Optical satellites are instrumental in detecting early signs of crop stress using multispectral imaging to prevent yield loss. The growth in precision agriculture, combined with advancements in digital farming, continues to boost demand for EO-enabled solutions that deliver real-time insights and help optimize land management strategies.

UK Optical Satellite Market is anticipated to grow at a CAGR of 14.1% through 2034. Ongoing investment in Earth observation technologies by the UK government has opened new opportunities for satellite-based monitoring. There's increasing national demand for high-quality imaging solutions used for tracking environmental changes, enhancing surveillance systems, and informing policies around climate resilience and sustainability.

Leading players in the Global Optical Satellite Market include Lockheed Martin Corporation, Airbus, Thales Alenia Space, and Maxar Technologies. These companies are implementing strategic measures to maintain and grow their market presence. A major focus lies in expanding satellite fleets and enhancing image resolution capabilities through advanced optics. They invest in collaborative programs with government agencies and private space firms to secure long-term contracts and co-develop next-generation systems. Significant R&D spending, localized sourcing of components, and efforts to streamline manufacturing are helping address rising material costs and production challenges. In addition, many players are enhancing their software platforms to support faster image processing and analytics integration delivering greater value to end-users.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.3 Trump administration tariffs analysis

- 3.3.1 Impact on trade

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.1.3 Impact on the industry

- 3.3.1.3.1 Supply-side impact (raw material)

- 3.3.1.3.1.1 Price volatility

- 3.3.1.3.1.2 Supply chain restructuring

- 3.3.1.3.1.3 Production cost implications

- 3.3.1.3.2 Demand-side impact

- 3.3.1.3.2.1 Price transmission to end markets

- 3.3.1.3.2.2 Market share dynamics

- 3.3.1.3.2.3 Consumer response patterns

- 3.3.1.3.1 Supply-side impact (raw material)

- 3.3.1.4 Key companies impacted

- 3.3.1.5 Strategic industry responses

- 3.3.1.5.1 Supply chain reconfiguration

- 3.3.1.5.2 Pricing and product strategies

- 3.3.1.5.3 Policy engagement

- 3.3.1.5.4 Outlook and future considerations

- 3.3.2 Growth drivers

- 3.3.2.1 Rising demand for high-resolution earth observation data

- 3.3.2.2 Increased investments in national security and surveillance

- 3.3.2.3 Rapid growth of commercial satellite

- 3.3.2.4 Technological advancements in imaging and data processing

- 3.3.2.5 Growing climate change monitoring and environmental protection initiatives

- 3.3.3 Industry pitfalls and challenges

- 3.3.3.1 High capital and operational costs

- 3.3.3.2 Data overload and processing complexity

- 3.3.1 Impact on trade

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Orbit Type, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 LEO

- 5.3 MEO

- 5.4 GEO

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Military reconnaissance

- 6.3 Crop monitoring

- 6.4 Urban planning

- 6.5 Disaster management

- 6.6 Mineral mapping

- 6.7 Environmental monitoring

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Government

- 7.3 Commercial

- 7.4 Academic

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Airbus

- 9.2 China Aerospace Science and Technology Corp.

- 9.3 Elbit Systems

- 9.4 Hanwha Group

- 9.5 Israeli Aerospace Industry

- 9.6 ISRO

- 9.7 Lockheed Martin Corporation

- 9.8 Maxar Technologies

- 9.9 Mitsubishi Electric Corporation

- 9.10 OHB SE

- 9.11 Satellogic

- 9.12 Surrey Satellite Technology Ltd

- 9.13 Thales Alenia Space

- 9.14 Turksat