|

市場調査レポート

商品コード

1755249

3Dプリンター義肢の市場機会、成長促進要因、産業動向分析、2025年~2034年予測3D Printed Prosthetics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 3Dプリンター義肢の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月23日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

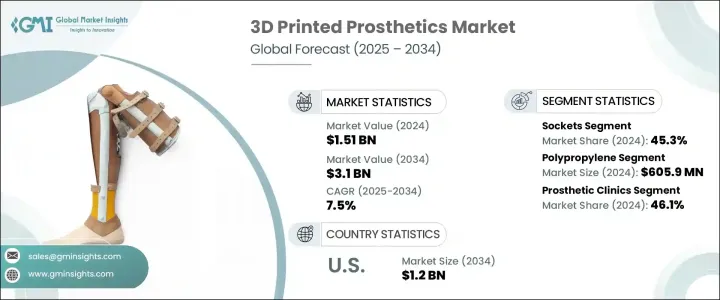

世界の3Dプリンター義肢市場は、2024年には15億1,000万米ドルと評価され、2034年にはCAGR 7.5%で成長し31億米ドルに達すると予測されています。

従来の製造方法(多くの場合、時間とコストがかかり、何度もフィッティングを行う必要がある)とは異なり、3Dプリンティング技術は、より迅速でコスト効率の高いアプローチを提供します。このようなカスタムソリューションは、製造時間を短縮すると同時に、全体的なユーザーエクスペリエンスを向上させます。パーソナライゼーションは、成長とともにニーズが頻繁に変化し、より頻繁に交換が必要となる小児患者にとって特に価値があります。義肢装具における高度な3Dプリンティングは、個別化された医療機器に対する世界のヘルスケア需要に応える上で大きな飛躍となります。

積層造形法(SLA)、選択的レーザー焼結法(SLS)、溶融積層造形法(FDM)などの積層造形における技術の進歩により、耐久性があり、軽量で機能的な補綴部品の作成が可能になっています。米国FDAなどの規制機関から複数の3Dプリンター製補綴器具が承認されたことで、この技術は信頼性と勢いを増し続けています。医療グレードのポリマーや合金などの生体適合材料が利用可能になったことで、補綴デバイスの耐久性、快適性、適応性がさらに向上しました。こうした技術革新は生産サイクルを短縮するだけでなく、義肢装具の品質と精度を高め、医療関係者や患者にとってより身近なものとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 15億1,000万米ドル |

| 予測金額 | 31億米ドル |

| CAGR | 7.5% |

ポリプロピレンは、その良好な強度対重量比、耐疲労性、化学的安定性により、2024年に6億590万米ドルを稼ぎ出す材料セグメントをリードしました。医療製造に広く採用されているポリプロピレンは、その生体適合性と滅菌に耐える能力が評価されています。ポリプロピレンは、補綴用ソケット、手術用ガイド、装具用サポーターの製造に広く使用されています。3Dプリンターによる軽量で個別化された医療ソリューションの需要が高まるにつれ、ポリプロピレンの利用は拡大し続けています。その柔らかさと機能性の融合により、患者中心の設計に好まれる選択肢となっています。

補綴クリニックセグメントは2024年に46.1%のシェアを占めました。これらの専門センターは、特に糖尿病や血管疾患などの慢性疾患による切断率が高い地域で、増加する患者数を管理するために3Dプリントを統合することが増えています。クリニックでは、3Dプリンティングの効率性により、迅速な修正や頻繁な交換が可能になるため、特に小児患者にとって重要な利点があります。このような施設は、多くの場合、リハビリ、トレーニング、フォローアップサービスを提供するオールインワンのプロバイダーとして機能し、3Dプリンター義肢の採用を促進しています。一元化されたアプローチは、ユーザーエクスペリエンスを簡素化し、長期的なソリューションを求める患者の信頼を築きます。

米国の3Dプリンター義肢市場は、肥満、糖尿病、末梢動脈疾患の増加により、2034年までに12億米ドルに達すると予測され、高度な補綴ソリューションの緊急ニーズが高まっています。遠隔医療、クラウドベースのワークフロー、遠隔患者スキャンなどのデジタルヘルス技術革新の統合は、3Dプリンター義肢拡大のための肥沃な土壌を作り出しています。これらの開発により、臨床医はより正確でタイムリーなケアを提供できるようになり、ヘルスケア全体への普及に貢献しています。

3Dプリンター義肢業界を形成する主要企業には、YouBionic、WillowWood、Mercuris、Limbitless Solutions、Stratasys、Bionic Prosthetics and Orthotics、Create Prosthetics、UNYQ、Protosthetics、Prothea、Open Bionics、Eqwal Group(Steeper Group)、Materialise、Exone、Motoricaなどがあります。市場の足場を固めるため、3Dプリンター義肢分野の企業は複数の戦略的アプローチを実施しています。主な焦点は、高度なソフトウェアとスキャン技術を活用した製品のカスタマイズの拡大です。企業はまた、素材の品質と快適性を向上させるための研究開発にも投資しています。病院、リハビリテーションセンター、研究機関との戦略的なコラボレーションは、アクセスの向上とイノベーションの加速に役立っています。さらに、企業は、遠隔地からの四肢スキャニングやクラウドベースのデザインなど、デジタルワークフローを強化し、生産を合理化するとともに、オンラインプラットフォームや地域化された印刷ハブを通じて地理的な拡大を図っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- パーソナライズされた手頃な価格の義肢ソリューションの需要の増加

- 3Dプリンティングと材料の技術的進歩

- 糖尿病、外傷、血管疾患による四肢切断の発生率の上昇

- 非営利団体や人道支援団体からの支援の増加

- 業界の潜在的リスク&課題

- 標準化された規制と品質管理の欠如

- 熟練した専門家と技術的知識の不足

- 促進要因

- 成長可能性分析

- ギャップ分析

- テクノロジーの情勢

- 将来の市場動向

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 特許分析

- 価格分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 競争市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 手足

- ソケット

- 関節

- その他のタイプ

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- ポリプロピレン

- ポリエチレン

- アクリル

- ポリウレタン

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- リハビリセンター

- 義肢クリニック

- その他の用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- メキシコ

- ブラジル

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Bionic Prosthetics and Orthotics

- Create Prosthetics

- Eqwal Group(Steeper Group)

- Exone

- Limbitless Solutions

- Materialise

- Mercuris

- Motorica

- Open Bionics

- Prothea

- Protosthetics

- Stratasys

- UNYQ

- WillowWood

- YouBionic

The Global 3D Printed Prosthetics Market was valued at USD 1.51 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 3.1 billion by 2034, driven by the increasing demand for highly personalized prosthetic solutions, as patients seek devices tailored to their specific anatomy and day-to-day needs. Unlike conventional manufacturing methods-which are often slow and expensive and involve numerous fitting sessions-3D printing technology offers a faster and more cost-efficient approach. These custom solutions improve the overall user experience while cutting down production time. Personalization is especially valuable for pediatric patients, whose needs change frequently as they grow, requiring replacements more often. Advanced 3D printing in prosthetics is a major leap forward in meeting global healthcare demands for individualized medical devices.

Technological advancements in additive manufacturing, including Stereolithography (SLA), Selective Laser Sintering (SLS), and Fused Deposition Modeling (FDM), are enabling the creation of durable, lightweight, and functional prosthetic components. With the approval of multiple 3D printed prosthetic devices by regulatory bodies like the U.S. FDA, the technology continues gaining credibility and momentum. The availability of biocompatible materials such as medical-grade polymers and alloys has further enhanced the durability, comfort, and adaptability of prosthetic devices. These innovations not only reduce production cycles but also elevate the quality and precision of prosthetics, making them more accessible for medical professionals and patients alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.51 Billion |

| Forecast Value | $3.1 Billion |

| CAGR | 7.5% |

Polypropylene led the material segment generating USD 605.9 million in 2024, owing to its favorable strength-to-weight ratio, fatigue resistance, and chemical stability. Widely adopted in medical manufacturing, polypropylene is valued for its biocompatibility and ability to withstand sterilization. It is extensively used to fabricate prosthetic sockets, surgical guides, and orthotic supports. As demand rises for lightweight and personalized medical solutions via 3D printing, the utilization of polypropylene continues to expand. Its blend of softness and functionality makes it a preferred choice in patient-centric designs.

The prosthetic clinics segment held a 46.1% share in 2024. These specialized centers are increasingly integrating 3D printing to manage growing patient volumes, especially in regions with high rates of amputation caused by chronic conditions like diabetes and vascular disease. Clinics benefit from 3D printing's efficiency, as it allows for quick modifications and frequent replacements-particularly vital for pediatric patients. These facilities often serve as all-in-one providers, offering rehabilitation, training, and follow-up services, encouraging greater adoption of 3D printed prosthetics. Their centralized approach simplifies the user experience and builds trust among patients seeking long-term solutions.

U.S. 3D Printed Prosthetics Market is expected to reach USD 1.2 billion by 2034 driven by rising incidences of obesity, diabetes, and peripheral artery disease, underscoring the urgent need for advanced prosthetic solutions. The integration of digital health innovations such as telehealth, cloud-based workflows, and remote patient scanning is creating fertile ground for the expansion of 3D printed prosthetics. These developments allow clinicians to deliver more accurate and timely care, contributing to broader adoption across the healthcare landscape.

Key players shaping the 3D Printed Prosthetics Industry include YouBionic, WillowWood, Mercuris, Limbitless Solutions, Stratasys, Bionic Prosthetics and Orthotics, Create Prosthetics, UNYQ, Protosthetics, Prothea, Open Bionics, Eqwal Group (Steeper Group), Materialise, Exone, and Motorica. To strengthen their market foothold, companies in the 3D printed prosthetics space are implementing multiple strategic approaches. A primary focus is expanding product customization by leveraging advanced software and scanning technologies. Firms are also investing in R&D to improve material quality and comfort. Strategic collaborations with hospitals, rehabilitation centers, and research institutions are helping to increase access and accelerate innovation. In addition, companies are enhancing digital workflows, such as remote limb scanning and cloud-based design, to streamline production and expand geographically through online platforms and localized printing hubs.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for personalized and affordable prosthetic solutions

- 3.2.1.2 Technological advancements in 3D printing and materials

- 3.2.1.3 Rising incidence of limb loss due to diabetes, trauma, and vascular diseases

- 3.2.1.4 Growing support from non-profits and humanitarian initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of standardized regulations and quality control

- 3.2.2.2 Limited availability of skilled professionals and technical knowledge

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Gap analysis

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Regulatory landscape

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.8 Patent analysis

- 3.9 Pricing analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Limbs

- 5.3 Sockets

- 5.4 Joints

- 5.5 Other types

Chapter 6 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Polypropylene

- 6.3 Polyethylene

- 6.4 Acrylics

- 6.5 Polyurethane

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Rehabilitation centers

- 7.4 Prosthetic clinics

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Bionic Prosthetics and Orthotics

- 9.2 Create Prosthetics

- 9.3 Eqwal Group (Steeper Group)

- 9.4 Exone

- 9.5 Limbitless Solutions

- 9.6 Materialise

- 9.7 Mercuris

- 9.8 Motorica

- 9.9 Open Bionics

- 9.10 Prothea

- 9.11 Protosthetics

- 9.12 Stratasys

- 9.13 UNYQ

- 9.14 WillowWood

- 9.15 YouBionic