フッ素系コーティングの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Fluorinated Coating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755248

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

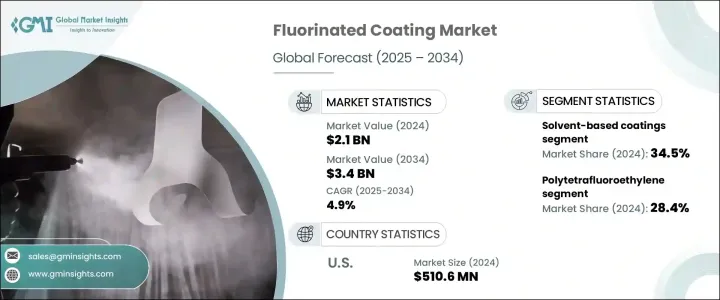

世界のフッ素系コーティング市場は2024年に21億米ドルと評価され、CAGR 4.9%で成長し、2034年には34億米ドルに達すると推定されています。

これらのコーティングは主に、優れた耐久性、熱安定性、化学薬品や腐食に対する耐性を提供するフッ素樹脂材料を用いて配合されます。これらの特性により、さまざまな作業環境において長持ちする高性能コーティングを必要とする産業にとって不可欠なものとなっています。極端な温度から化学反応性の高い環境まで、フッ素系コーティングは、特に高湿度や環境ストレスの多い地域で高い性能を発揮し続けています。

環境劣化に耐える高度な素材への需要が高まるにつれ、フッ素系コーティングは、素材の効率性と長寿命を優先するセクターで採用が拡大しています。さらに、交通機関や土木インフラへの投資により、主要資産の耐用年数を延ばすと同時に長期的なメンテナンスコストを削減するよう設計された保護コーティングの使用が拡大しています。技術革新、持続可能性に向けた規制のシフト、環境負荷の低減を求める動きは、水性塗料やUV硬化型塗料など、環境に配慮したコーティングソリューションの採用をメーカーに促しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 21億米ドル |

| 予測金額 | 34億米ドル |

| CAGR | 4.9% |

製品タイプ別では、ポリテトラフルオロエチレン(PTFE)が2024年の世界市場の28.4%以上を占める。低表面エネルギーと非反応性で知られるPTFEは、最小限の摩擦、熱耐久性、強力な耐薬品性を必要とする用途の定番材料となっています。PTFEの用途は、極端な温度や腐食剤にさらされることが一般的な、幅広い最終用途分野に及んでいます。PTFEは、応力下でも安定した挙動を示すため、製造工程で広く使用されており、機械的摩耗や化学薬品にさらされる部品に最適です。

技術別に分類すると、溶剤系塗料は2024年に市場シェアの約34.5%を占めました。長年にわたる優位性は、優れた接着性、耐用年数の延長、厳しい使用条件下での回復力に起因します。これらの塗料は過酷な環境下でも高い信頼性を発揮するため、機械的・熱的負荷の高い分野で広く使用されています。揮発性有機化合物(VOC)排出に関する規制の圧力にもかかわらず、溶剤系塗料はその工業的優位性から確固たる存在感を保ち続けています。しかし、環境に優しいソリューションへの関心の高まりにより、業界情勢は徐々に変化しつつあります。水系塗料は、特に排出規制が強化されている地域で支持を集めており、UV硬化型塗料は、その速硬化性と低エネルギー要件のおかげで、精密製造においてますます実用的になってきています。

基材別では、金属が2024年の世界市場で主導的地位を占めています。金属は製造業で広く使用されており、風雨や化学物質、熱にさらされるため、フッ素系コーティングに適しています。これらのコーティングは腐食や酸化に対するバリアとなり、構造部品や機器の寿命を延ばすのに不可欠です。プラスチック、複合材料、コンクリートなどの基材も、特に耐候性仕上げを必要とするインフラプロジェクトで需要が伸びています。

性能属性に関しては、耐薬品性が2024年の市場をリードしました。多くの産業分野では腐食性の強い化学薬品が使用されており、こうした環境で使用される機器には、そのような暴露に耐えるコーティングが施されていなければならないです。フッ素系コーティングは、表面の劣化、機器の故障、汚染のリスクを防ぐため、好まれています。フッ素系コーティングは、タンク、パイプライン、処理装置の信頼性の高いライニングとして機能し、安定した操業と安全性を保証します。熱安定性、電気絶縁性、低摩擦表面などの特性も、特に高精度・高性能用途での採用に大きく貢献しています。

用途別では、航空宇宙・防衛分野が2024年に支配的なカテゴリーに浮上しました。これらの産業は過酷な環境に耐える材料を必要としており、フッ素系コーティングは耐熱性、軽量性能、長期的な保護を提供することでその需要に応えています。一方、腐食性物質や高温にさらされる機械にコーティングが広く使用されていることから、産業用機器が市場で最大のシェアを占めています。また、食品関連分野も、こびりつきにくく、お手入れが簡単な表面への需要が商業用および住宅用で伸びているため、引き続き好調を維持しています。

地域別分析では、米国のフッ素系コーティング市場は2024年に5億1,060万米ドルを突破しました。北米では、確立された産業基盤、着実な技術進歩、製品性能への継続的な注力を背景に、同国が引き続きリードしています。高品質で耐久性のある塗料へのニーズは、インフラや製造部門の継続的な開発によってさらに高まっています。また、メンテナンスの容易な素材を好む消費者動向も、家庭用および屋外製品用途の成長を支えています。

市場は緩やかな統合が続いており、いくつかの主要企業が大きなシェアを占めています。競合の焦点は、製品の技術革新、規制への対応、特定の業界向けにカスタマイズされたソリューションです。主要企業は一貫して表面保護機能を強化し、成長率の高い応用分野への進出を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国

- 主要輸入国

注:上記の貿易統計は主要国についてのみ提供されます

- 影響要因

- 市場促進要因

- 市場抑制要因

- 市場機会

- 市場の課題

- 製品概要

- フッ素ポリマーの化学と構造

- パフォーマンス特性

- 耐薬品性

- 熱安定性

- 非粘着性および低摩擦性

- 耐候性と耐久性

- 他のコーティング技術との比較

- 製造プロセス分析

- 樹脂生産

- 処方技術

- 応募方法

- 硬化プロセス

- 品質管理手順

- 規制情勢

- 成長可能性分析

- 価格分析(USD/トン) 2021年~2034年

- 持続可能性と環境影響評価

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 市場シェア分析

- 戦略枠組み

- 合併と買収

- ジョイントベンチャーとコラボレーション

- 新製品開発

- 拡大戦略

- 競合ベンチマーキング

- ベンダー情勢

- 競合ポジショニングマトリックス

- 戦略的ダッシュボード

- 特許分析とイノベーション評価

- 新規参入者の市場参入戦略

- 配電網分析

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- ポリテトラフルオロエチレン

- 純粋なPTFEコーティング

- PTFEベースの複合コーティング

- 改質PTFEコーティング

- ポリフッ化ビニリデン

- PVDFホモポリマーコーティング

- PVDFコポリマーコーティング

- 改質PVDFコーティング

- フッ素化エチレンプロピレン

- ペルフルオロアルコキシアルカン

- エチレンテトラフルオロエチレン

- エチレンクロロトリフルオロエチレン

- ポリクロロトリフルオロエチレン

- その他

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 溶剤系コーティング

- 水性コーティング

- 粉体コーティング

- UV硬化コーティング

- その他

第7章 市場推計・予測:基材別、2021年~2034年

- 主要動向

- 金属

- 鋼鉄

- アルミニウム

- その他

- プラスチック・複合材料

- ガラス

- コンクリート・石材

- その他

第8章 市場推計・予測:パフォーマンス属性別、2021年~2034年

- 主要動向

- 耐薬品性

- 耐候性

- 非粘着性/低摩擦

- 熱安定性

- 電気絶縁

- 腐食防止

- その他

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 産業機器

- 化学処理装置

- 石油・ガス機器

- 食品加工機器

- 医薬品機器

- その他

- 建築・建設

- 建築用コーティング

- 屋根材

- ファサードと外装

- その他

- 自動車・輸送

- 外装部品

- 内装部品

- 内装用途

- その他

- 調理器具と食品接触

- ノンスティック調理器具

- ベーキングウェア

- 食品加工機器

- その他

- 電子・電気

- PCBコーティング

- ワイヤーおよびケーブルコーティング

- 半導体アプリケーション

- その他

- 航空宇宙および防衛

- 海洋

- ヘルスケアと医療

- その他

第10章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 工業製造業

- 化学薬品

- 石油・ガス

- 発電

- その他

- 建築・建設

- 自動車・輸送

- 消費財

- 調理器具とキッチン用品

- 家電製品

- その他

- エレクトロニクスおよび半導体

- 航空宇宙および防衛

- 食品・飲料

- ヘルスケア&医薬品

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第12章 企業プロファイル

- 3M Company

- AFT Fluorotec

- AGC Chemicals Americas

- AGC Inc.

- AkzoNobel N.V.

- Arkema

- Beckers Group

- Daikin Industries

- Dow

- DuPont

- Fluorotherm Polymers

- Gujarat Fluorochemicals

- Jotun A/S

- Nippon Paint Holdings

- PPG Industries, Inc.

- Sherwin-Williams Company

- Solvay S.A.

- The Chemours Company

- Whitford Corporation

目次

The Global Fluorinated Coating Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 3.4 billion by 2034. These coatings are primarily formulated using fluoropolymer materials that offer outstanding durability, thermal stability, and resistance to chemicals and corrosion. These properties make them vital for industries that demand long-lasting, high-performance coatings across various operational environments. From extreme temperatures to chemically reactive surroundings, fluorinated coatings continue to demonstrate strong performance, particularly in regions prone to high humidity and environmental stress.

As the demand for advanced materials capable of resisting environmental degradation grows, these coatings are seeing increased adoption across sectors that prioritize efficiency and longevity in materials. Moreover, investments in transportation and civil infrastructure have led to greater use of protective coatings designed to increase the service life of key assets while also reducing long-term maintenance costs. Technological innovations, regulatory shifts toward sustainability, and the push for lower environmental impact are encouraging manufacturers to adopt eco-conscious coating solutions, including water-based and UV-curable alternatives.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $3.4 Billion |

| CAGR | 4.9% |

In terms of product type, polytetrafluoroethylene (PTFE) accounted for over 28.4% of the global market in 2024. Known for its low surface energy and non-reactive nature, PTFE has become a staple material for applications that require minimal friction, thermal endurance, and strong chemical resistance. Its utility spans a broad spectrum of end-use sectors where exposure to extreme temperatures and corrosive agents is common. PTFE is widely used in manufacturing processes due to its stable behavior under stress, making it ideal for components exposed to mechanical wear or chemical exposure.

When categorized by technology, solvent-based coatings captured nearly 34.5% of the market share in 2024. Their long-standing dominance is attributed to superior adhesion, extended service life, and resilience in tough operating conditions. These coatings perform reliably under aggressive environments, which explains their widespread use in sectors involving high mechanical and thermal loads. Despite regulatory pressure around volatile organic compound (VOC) emissions, solvent-based coatings continue to maintain a solid presence due to their industrial advantages. However, rising interest in eco-friendly solutions is gradually shifting the industry landscape. Waterborne coatings are gaining traction, especially in regions enforcing stricter emission norms, while UV-curable coatings are becoming increasingly viable in precision manufacturing thanks to their rapid curing and low energy requirements.

Based on substrate, metal held the leading position in the global market in 2024. Metals are extensively used in manufacturing, and their exposure to weather, chemicals, and heat makes them suitable candidates for fluorinated coatings. These coatings provide a barrier against corrosion and oxidation, making them essential for extending the life of structural components and equipment. Other substrates such as plastics, composites, and concrete are also witnessing growing demand, particularly in infrastructure projects requiring weather-resistant finishes.

Regarding performance attributes, chemical resistance led the market in 2024. Many industrial sectors handle aggressive chemicals, and equipment used in these settings must be coated to withstand such exposure. Fluorinated coatings are preferred because they prevent surface degradation, equipment failure, and contamination risks. Their ability to act as reliable linings for tanks, pipelines, and processing equipment ensures uninterrupted operation and safety. Properties like thermal stability, electrical insulation, and low-friction surfaces also contribute significantly to their adoption, particularly in high-precision and high-performance applications.

By application, the aerospace and defense segment emerged as the dominant category in 2024. These industries require materials that can endure extreme environments, and fluorinated coatings meet that demand by offering heat resistance, lightweight performance, and long-term protection. Meanwhile, industrial equipment claimed the largest share of the market due to the widespread use of coatings in machinery exposed to corrosive substances and elevated temperatures. The food-related segment also remains strong as demand for non-stick, easy-clean surfaces grows in commercial and residential applications.

In regional analysis, the United States fluorinated coating market surpassed USD 510.6 million in 2024. The country continues to lead in North America, backed by a well-established industrial base, steady technological advancements, and an ongoing focus on product performance. The need for high-quality, durable coatings is further amplified by the continuous development of infrastructure and manufacturing sectors. Consumer trends favoring easy-maintenance materials also support growth in household and outdoor product applications.

The market remains moderately consolidated, with several key players commanding significant shares. Competitive focus revolves around product innovation, regulatory compliance, and customized solutions tailored for specific industries. Leading companies are consistently enhancing surface protection capabilities and expanding their reach across high-growth application areas.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Impact forces

- 3.4.1 Market drivers

- 3.4.2 Market restraints

- 3.4.3 Market opportunities

- 3.4.4 market challenges

- 3.5 Product overview

- 3.5.1 Fluoropolymer chemistry & structure

- 3.5.2 Performance characteristics

- 3.5.3 Chemical resistance properties

- 3.5.4 Thermal stability

- 3.5.5 Non-stick & low friction properties

- 3.5.6 Weather resistance & durability

- 3.5.7 Comparison with other coating technologies

- 3.6 Manufacturing process analysis

- 3.6.1 Resin production

- 3.6.2 Formulation techniques

- 3.6.3 Application methods

- 3.6.4 Curing processes

- 3.6.5 Quality control procedures

- 3.7 Regulatory landscape

- 3.8 Growth potential analysis

- 3.9 Pricing analysis (USD/Tons) 2021-2034

- 3.10 Sustainability & environmental impact assessment

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Market share analysis

- 4.2 Strategic framework

- 4.2.1 Mergers & acquisitions

- 4.2.2 Joint ventures & collaborations

- 4.2.3 New product developments

- 4.2.4 Expansion strategies

- 4.3 Competitive benchmarking

- 4.4 Vendor landscape

- 4.5 Competitive positioning matrix

- 4.6 Strategic dashboard

- 4.7 Patent analysis & innovation assessment

- 4.8 Market entry strategies for new players

- 4.9 Distribution network analysis

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polytetrafluoroethylene

- 5.2.1 Pure PTFE coatings

- 5.2.2 PTFE-based composite coatings

- 5.2.3 Modified PTFE coatings

- 5.3 Polyvinylidene fluoride

- 5.3.1 PVDF homopolymer coatings

- 5.3.2 PVDF copolymer coatings

- 5.3.3 Modified PVDF coatings

- 5.4 Fluorinated ethylene propylene

- 5.5 Perfluoroalkoxy alkane

- 5.6 Ethylene tetrafluoroethylene

- 5.7 Ethylene chlorotrifluoroethylene

- 5.8 Polychlorotrifluoroethylene

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solvent-based coatings

- 6.3 Water-based coatings

- 6.4 Powder coatings

- 6.5 UV-curable coatings

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Substrate, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Metal

- 7.2.1 Steel

- 7.2.2 Aluminum

- 7.2.3 Others

- 7.3 Plastic & composites

- 7.4 Glass

- 7.5 Concrete & masonry

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Performance Attribute, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Chemical resistance

- 8.3 Weather resistance

- 8.4 Non-stick/low friction

- 8.5 Thermal stability

- 8.6 Electrical insulation

- 8.7 Corrosion protection

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Industrial equipment

- 9.2.1 Chemical processing equipment

- 9.2.2 Oil & gas equipment

- 9.2.3 Food processing equipment

- 9.2.4 Pharmaceutical equipment

- 9.2.5 Others

- 9.3 Building & construction

- 9.3.1 Architectural coatings

- 9.3.2 Roofing materials

- 9.3.3 Facades & cladding

- 9.3.4 Others

- 9.4 Automotive & transportation

- 9.4.1 Exterior components

- 9.4.2 Interior components

- 9.4.3 Under-the-hood applications

- 9.4.4 Others

- 9.5 Cookware & food contact

- 9.5.1 Non-Stick cookware

- 9.5.2 Bakeware

- 9.5.3 Food processing equipment

- 9.5.4 Others

- 9.6 Electronics & electrical

- 9.6.1 PCB coatings

- 9.6.2 Wire & cable coatings

- 9.6.3 Semiconductor applications

- 9.6.4 Others

- 9.7 Aerospace & defense

- 9.8 Marine

- 9.9 Healthcare & medical

- 9.10 Others

Chapter 10 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Industrial manufacturing

- 10.2.1 Chemical

- 10.2.2 Oil & gas

- 10.2.3 Power generation

- 10.2.4 Others

- 10.3 Building & construction

- 10.4 Automotive & transportation

- 10.5 Consumer goods

- 10.5.1 Cookware & kitchenware

- 10.5.2 Appliances

- 10.5.3 Others

- 10.6 Electronics & semiconductors

- 10.7 Aerospace & defense

- 10.8 Food & beverage

- 10.9 Healthcare & pharmaceutical

- 10.10 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 3M Company

- 12.2 AFT Fluorotec

- 12.3 AGC Chemicals Americas

- 12.4 AGC Inc.

- 12.5 AkzoNobel N.V.

- 12.6 Arkema

- 12.7 Beckers Group

- 12.8 Daikin Industries

- 12.9 Dow

- 12.10 DuPont

- 12.11 Fluorotherm Polymers

- 12.12 Gujarat Fluorochemicals

- 12.13 Jotun A/S

- 12.14 Nippon Paint Holdings

- 12.15 PPG Industries, Inc.

- 12.16 Sherwin-Williams Company

- 12.17 Solvay S.A.

- 12.18 The Chemours Company

- 12.19 Whitford Corporation

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日