|

市場調査レポート

商品コード

1755247

固体ロケットモーターの市場機会、成長促進要因、産業動向分析、2025~2034年予測Solid Rocket Motors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 固体ロケットモーターの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年05月23日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

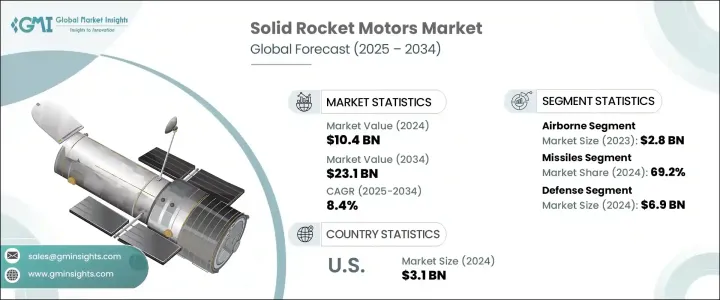

固体ロケットモーターの世界市場規模は、2024年には104億米ドルとなり、世界の防衛予算の増加や最新のミサイル・ロケットシステムの必要性により、CAGR 8.4%で成長し、2034年には231億米ドルに達すると予測されています。

固体ロケットモーターは、そのシンプルさ、高推力出力、高速点火、長寿命により、軍事・航空宇宙用途に理想的なものとして支持を集めています。経済・政治開発はサプライチェーンに影響を与え、部品コストを上昇させ、市場動向にさらに影響を与えています。このような課題にもかかわらず、各国は国家安全保障構想やミサイル技術に多額の投資を続けており、信頼性が高く拡張性の高い推進システムへの需要が高まっています。

固体ロケットモーターは、地対空ミサイル、戦術弾道ミサイル、迎撃ミサイルシステムに適したコンパクトなフォームファクターで高性能を提供する、防衛プログラム全体に不可欠なコンポーネントです。モジュール式で適応性の高い推進技術は、コストを最適化しながら特定のミッション要件をサポートするため、不可欠なものとなっています。この市場は、機動性、射程距離、発射精度を高めるための継続的な技術革新から利益を得ています。各国が抑止力と宇宙機能への注力を強化する中、固体モーターは世界の防衛・航空宇宙インフラにとって不可欠な存在であり続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 104億米ドル |

| 予測金額 | 231億米ドル |

| CAGR | 8.4% |

衛星打上げロケット分野は、コスト効率と信頼性の高い打上げソリューションへのニーズの高まりにより、2024年には30.8%のシェアを占めると予測されています。固体推進システムは、その最小限のメンテナンスと配備の容易さから、小型から中型の打ち上げプラットフォームで広く支持されています。衛星配備における官民双方の取り組みが拡大する中、迅速かつ信頼性の高い軌道打ち上げのニーズを満たすために、固体ロケットモーターがますます使用されるようになっています。

2024年、防衛分野は69億米ドルを生み出し、固体ロケットモーター市場において支配的な最終用途カテゴリーとしての地位を確立しました。先進的な戦術兵器システムとミサイルのアップグレードに対する一貫した需要は、迅速な対応能力と技術的優位性を優先する世界の軍事力の直接的な結果です。固体ロケットモーターは、高い推力対重量比、最小限のメンテナンス要件、信頼性の高い保管で知られており、これらの目的に合致しています。いくつかの地域で進行中の軍隊の近代化は、戦略的防衛イニシアティブと相まって、固体推進システムの採用をさらに加速させています。

米国の固体ロケットモーター2024年の市場規模は31億米ドルで、米国は固体推進技術の世界的リーダーとしての役割を強化しています。国防と航空宇宙プログラムへの旺盛な予算配分が、この勢いを後押しし続けています。極超音速システム、次世代ミサイルプラットフォーム、再使用可能な打ち上げロケットへの投資は、固体モーター技術の国内生産と技術革新に拍車をかけています。米軍の先進ミサイルシステム配備に向けた積極的なスケジュールや、NASAが深宇宙探査に再び重点を置くことで、コンパクトで高効率の推進ソリューションに対する需要が高まっています。

Aerojet Rocketdyne社、L3Harris Technologies社、Northrop Grumman社、RAFAEL Advanced Defense Systems Ltd.社などの大手企業は、さまざまなプラットフォームで政府および民間アプリケーションをサポートする固体モーターシステムを革新しています。市場での地位を固めるため、主要企業は、様々な打ち上げシステムや防衛システムにおいて柔軟性と拡張性を高めるモジュラーモーター技術に投資しています。企業は、製造効率の向上、製造コストの削減、次世代複合材料の研究開発の拡大に注力しています。宇宙機関や防衛機関との協力は、進化するミッションプロファイルに合わせて固体推進ソリューションを調整するのに役立ち、戦略的な契約や買収は市場浸透の深化を可能にします。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 世界の防衛費の増加

- 衛星打ち上げ計画の急増

- 有利な政府契約と研究開発資金

- 極超音速および戦術ミサイルシステムへの採用

- 推進剤と材料の技術的進歩

- 業界の潜在的リスク&課題

- 厳格な規制と安全遵守

- 開発コストが高く、再利用性が限られている

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:打ち上げプラットフォーム別、2021年~2034年

- 主要動向

- 空軍

- 陸軍

- 海軍

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 衛星打ち上げロケット

- ミサイル

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 防衛

- 宇宙機関

- 商業スペース

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Anduril Industries

- AVIO SPA

- BrahMos Aerospace Private Limited

- General Dynamics Corporation

- Hanwha Group

- ISRO

- L3Harris Technologies, Inc.

- Lockheed Martin Corporation

- Mitsubishi Heavy Industries

- Nammo AS

- Northrop Grumman

- RAFAEL Advanced Defense Systems Ltd.

- ROKETSAN

- Roxel Group

- Tata Advanced Systems Limited

- URSA MAJOR TECHNOLOGIES INC

The Global Solid Rocket Motors Market was valued at USD 10.4 billion in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 23.1 billion by 2034, driven by rising global defense budgets and the need for modern missile and launch vehicle systems. Solid rocket motors are gaining traction due to their simplicity, high-thrust output, fast ignition, and long shelf life, making them ideal for military and aerospace use. Economic and political developments have affected supply chains and increased component costs, further influencing market trends. Despite these challenges, countries continue to invest heavily in national security initiatives and missile technologies, reinforcing the demand for reliable and scalable propulsion systems.

Solid rocket motors are vital components across defense programs, offering high performance in a compact form factor suitable for surface-to-air, tactical ballistic, and interceptor missile systems. Modular and adaptable propulsion technologies are becoming essential as they support specific mission requirements while optimizing cost. The market benefits from ongoing innovations to enhance maneuverability, range, and launch precision. As nations intensify their focus on deterrence and space capabilities, solid motors remain an indispensable part of defense and aerospace infrastructure worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.4 Billion |

| Forecast Value | $23.1 Billion |

| CAGR | 8.4% |

The satellite launch vehicle segment is projected to hold a 30.8% share in 2024, driven by the growing need for cost-efficient, high-reliability launch solutions. Solid propulsion systems are widely favored in small to medium-sized launch platforms due to their minimal maintenance and ease of deployment. As both public and private initiatives in satellite deployment grow, solid rocket motors are increasingly used to meet the needs of rapid and dependable orbital launches.

In 2024, the defense segment generated USD 6.9 billion, establishing itself as the dominant end-use category in the solid rocket motors market. The consistent demand for advanced tactical weapon systems and missile upgrades is a direct result of global military forces prioritizing rapid response capabilities and technological superiority. Solid rocket motors, known for their high thrust-to-weight ratio, minimal maintenance requirements, and dependable storage, align well with these objectives. Ongoing modernization of armed forces across several regions, coupled with strategic defense initiatives, has further amplified the adoption of solid propulsion systems.

United States Solid Rocket Motors Market generated USD 3.1 billion in 2024, reinforcing the country's role as a global leader in solid propulsion technologies. A robust budget allocation toward national defense and aerospace programs continues to drive this momentum. Investments in hypersonic systems, next-generation missile platforms, and reusable launch vehicles are helping fuel domestic production and innovation in solid motor technologies. The U.S. military's aggressive timeline for deploying advanced missile systems and NASA's renewed emphasis on deep space exploration are pushing demand for compact, high-efficiency propulsion solutions.

Leading firms such as Aerojet Rocketdyne, L3Harris Technologies, Inc., Northrop Grumman, and RAFAEL Advanced Defense Systems Ltd. are innovating solid motor systems that support government and commercial applications across various platforms. To solidify their market position, key companies are investing in modular motor technologies that provide enhanced flexibility and scalability across different launch and defense systems. Firms focus on improving manufacturing efficiencies, reducing production costs, and expanding R&D in next-gen composite materials. Collaborations with space and defense agencies help tailor solid propulsion solutions to evolving mission profiles, while strategic contracts and acquisitions enable deeper market penetration.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increased defense expenditure globally

- 3.7.1.2 Surge in satellite launch programs

- 3.7.1.3 Favorable government contracts and R&D funding

- 3.7.1.4 Adoption in hypersonic and tactical missile systems

- 3.7.1.5 Technological advancements in propellants and materials

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Stringent regulatory and safety compliance

- 3.7.2.2 High development costs and limited reusability

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Launch Platform, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Airborne

- 5.3 Ground-based

- 5.4 Naval

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Satellite launch vehicles

- 6.3 Missiles

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Defense

- 7.3 Space agencies

- 7.4 Commercial space

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Anduril Industries

- 9.2 AVIO SPA

- 9.3 BrahMos Aerospace Private Limited

- 9.4 General Dynamics Corporation

- 9.5 Hanwha Group

- 9.6 ISRO

- 9.7 L3Harris Technologies, Inc.

- 9.8 Lockheed Martin Corporation

- 9.9 Mitsubishi Heavy Industries

- 9.10 Nammo AS

- 9.11 Northrop Grumman

- 9.12 RAFAEL Advanced Defense Systems Ltd.

- 9.13 ROKETSAN

- 9.14 Roxel Group

- 9.15 Tata Advanced Systems Limited

- 9.16 URSA MAJOR TECHNOLOGIES INC