|

市場調査レポート

商品コード

1755238

航空業界におけるIoTの市場機会、成長促進要因、産業動向分析、2025年~2034年予測IoT in Aviation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 航空業界におけるIoTの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月22日

発行: Global Market Insights Inc.

ページ情報: 英文 191 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

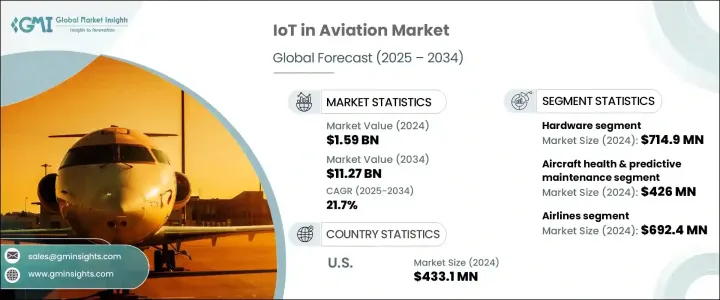

世界の航空業界におけるIoT市場は2024年に15億9,000万米ドルと評価され、CAGR21.7%で成長し、2034年までには112億7,000万米ドルに達すると予測されています。

業務効率化、コスト削減、リアルタイムの意思決定に対する需要の高まりが成長の原動力となっており、航空関係者は業務の近代化のためにIoTを導入しています。電子機器と半導体部品に対する関税の導入は、生産コストの大幅な上昇を引き起こし、IoTデバイスの可用性とサプライチェーンの俊敏性を混乱させました。こうしたコスト増はメーカーが吸収するか、エンドユーザーに転嫁され、普及が遅れました。アビオニクスハードウェアセンサー、接続モジュールなどの主要な航空機技術は特に影響を受け、国内調達へのシフトを促しました。国内サプライヤーは限られた能力しか提供できませんでしたが、この移行は短期的な摩擦を刺激したものの、最終的には米国市場における自立的な技術革新を促しました。この混乱は、重要技術分野における現地生産の課題と戦略的優位性を浮き彫りにしました。

リアルタイムのセンサー技術により、航空機運航会社は機内システムの監視、飛行経路の最適化、燃料消費の効率的な管理が可能になります。IoTが可能にする予知保全は、エンジンの健全性、構造的完全性、システム性能を追跡することで、ダウンタイムを削減し、安全性を高めます。空港や航空会社は、コネクテッドテクノロジーを活用した自動化によって乗務員計画や手荷物ロジスティクスを合理化し、運用コストの削減と信頼性の向上を実現します。IoTを通じて提供される旅客サービスの強化は、旅行者のブランドロイヤルティの強化にもつながります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 15億9,000万米ドル |

| 予測金額 | 112億7,000万米ドル |

| CAGR | 21.7% |

ハードウェア分野は、航空機システムとコントロールセンター間の堅牢なデータフローを可能にするセンサー、アクチュエーター、通信モジュールの需要が牽引し、2024年には7億1,490万米ドルに達しました。RFIDとビーコン技術は手荷物の追跡と在庫管理をサポートし、航空電子工学グレードのモジュールは飛行中の中断のない接続性を確保します。機内に設置されたエッジコンピューティングソリューションは、重要なデータをローカルで処理し、遅延や外部ネットワークへの依存を最小限に抑えます。これらの技術により、より安全な運航と、機内および地上でのサービス効率の向上が可能になります。

航空機の健全性・予知保全アプリケーション分野の2024年の市場規模は4億2,600万米ドルでした。この分野では、センサーデータと高度な分析を使用して、部品の摩耗、エンジン性能、システム診断をリアルタイムで評価します。予測モデリングは、予期せぬ故障を減らし、メンテナンス作業のより良い計画を可能にし、航空機資産の運用寿命を延ばすのに役立ちます。

米国の航空業界におけるIoT市場は、2024年に4億3,310万米ドルとなりました。同国は、航空インフラ全体にコネクテッドテクノロジーを幅広く統合しているため、主導的な役割を維持しています。GE Aviation、Cisco Systems Inc.、Siemens、Honeywell International Inc.、International Business Machines Corporationを含む主要航空宇宙企業は、航空機と空港運用のためのIoTシステムの開発を先導してきました。スマートキャビン環境、メンテナンスの自動化、空港の最適化における米国の航空業界の進歩により、米国は航空業界における世界のIoT導入の最前線に押し上げられました。

競争力を強化するため、IoT航空業界の主要企業は、センサーの革新、リアルタイム分析、エッジコンピューティングへの研究開発投資の拡大に注力しています。航空宇宙メーカーや空港当局との戦略的提携により、新規および既存の航空機へのIoTシステムの迅速な展開が可能になります。これらの企業は、フライトクリティカルなシステムにおける安全なデータ伝送を確保するため、サイバーセキュリティを優先しています。さらに、各社はAIを統合したIoTフレームワークに投資して、予測診断を提供し、旅客と貨物のオペレーションを合理化し、市場でのリーダーシップをさらに強固なものにしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- トランプ政権の関税分析(ハードウェア)

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 成長促進要因

- 運用効率の向上とコスト削減

- 乗客体験とパーソナライゼーションの向上

- 予知保全と安全性の進歩

- スマート空港とコネクテッドエコシステムの成長

- 業界の潜在的リスク・課題

- 高い導入コスト

- サイバーセキュリティの脆弱性

- 成長促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:ソリューション別、2021年~2034年

- 主要動向

- ハードウェア

- ソフトウェア

- サービス

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- サプライチェーン・物流

- 空港・地上業務

- 乗客体験・接続性

- 飛行運用・航空機管理

- 航空機の健全性と予測メンテナンス

- 航空機の製造・組立

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 航空会社

- 空港

- Mroプロバイダー

- 航空機メーカー

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Honeywell International Inc.

- Siemens

- General Electric Company

- International Business Machines Corporation

- Cisco Systems Inc.

- SITA

- Airbus

- The Boeing Company

- Thales

- Lufthansa Technik

- Collins Aerospace

- Panasonic Avionics Corporation

- SAP SE

- Microsoft

- Amadeus IT Group SA

- Palantir Technologies

- Tata Communications Limited

The Global IoT in Aviation Market was valued at USD 1.59 billion in 2024 and is estimated to grow at a CAGR of 21.7% to reach USD 11.27 billion by 2034. The growth is driven by the increasing demand for operational efficiency, cost reduction, and real-time decision-making, aviation stakeholders are embracing IoT to modernize their operations. The implementation of tariffs on electronics and semiconductor components caused a significant uptick in production costs, disrupting IoT device availability and supply chain agility. These increased costs were either absorbed by manufacturers or shifted to end users, slowing widespread adoption. Key aircraft technologies such as avionics hardware, sensors, and connectivity modules were particularly impacted, prompting a shift toward domestic sourcing. Although domestic suppliers offered limited capacity, this transition stimulated short-term friction but eventually encouraged self-reliant innovation in the U.S. market. The disruption highlighted the challenges and strategic advantages of localizing production in critical technology sectors.

Real-time sensor technology allows aircraft operators to monitor onboard systems, optimize flight paths, and manage fuel consumption more effectively. Predictive maintenance enabled by IoT reduces downtime and enhances safety by tracking engine health, structural integrity, and system performance. Airports and airlines streamline crew planning and baggage logistics using automation powered by connected technologies, cutting operational costs and improving reliability. Enhanced passenger services delivered through IoT also foster stronger brand loyalty among travelers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.59 Billion |

| Forecast Value | $11.27 Billion |

| CAGR | 21.7% |

The hardware segment reached USD 714.9 million in 2024, driven by demand for sensors, actuators, and communication modules that enable robust data flow between aircraft systems and control centers. RFID and beacon technology support baggage tracking and inventory control, while avionics-grade modules ensure uninterrupted connectivity in flight. Edge computing solutions installed onboard process critical data locally, minimizing latency and dependency on external networks. These technologies enable safer operations and better in-flight and ground service efficiency.

The aircraft health and predictive maintenance application segment was valued at USD 426 million in 2024. This area uses sensor data and advanced analytics to evaluate component wear, engine performance, and system diagnostics in real-time. Predictive modeling helps reduce unexpected breakdowns, allows better planning of maintenance tasks, and extends the operational lifespan of aircraft assets.

United States IoT in Aviation Market was valued at USD 433.1 million in 2024. The country maintains a leading role owing to the extensive integration of connected technologies across its aviation infrastructure. Major aerospace companies including GE Aviation, Cisco Systems Inc., Siemens, Honeywell International Inc., and International Business Machines Corporation have spearheaded the development of IoT systems for aircraft and airport operations. U.S. aviation advancements in smart cabin environments, maintenance automation, and airport optimization have pushed the country to the forefront of global IoT adoption in aviation.

To strengthen their competitive edge, leading companies in the IoT aviation sector are focusing on scaling R&D investments in sensor innovation, real-time analytics, and edge computing. Strategic collaborations with aerospace manufacturers and airport authorities allow faster deployment of IoT systems across new and existing fleets. These firms prioritize cybersecurity to ensure safe data transmission in flight-critical systems. Additionally, companies are investing in AI-integrated IoT frameworks to deliver predictive diagnostics and streamline passenger and cargo operations, further solidifying their market leadership.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis (Hardware)

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.1.3 Impact on the industry

- 3.2.1.3.1 Supply-side impact

- 3.2.1.3.1.1 Price volatility

- 3.2.1.3.1.2 Supply chain restructuring

- 3.2.1.3.1.3 Production cost implications

- 3.2.1.3.2 Demand-side impact

- 3.2.1.3.2.1 Price transmission to end markets

- 3.2.1.3.2.2 Market share dynamics

- 3.2.1.3.2.3 Consumer response patterns

- 3.2.1.3.1 Supply-side impact

- 3.2.1.4 Key companies impacted

- 3.2.1.5 Strategic industry responses

- 3.2.1.5.1 Supply chain reconfiguration

- 3.2.1.5.2 Pricing and product strategies

- 3.2.1.5.3 Policy engagement

- 3.2.1.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Enhanced operational efficiency and cost savings

- 3.3.1.2 Improved passenger experience and personalization

- 3.3.1.3 Advancements in predictive maintenance and safety

- 3.3.1.4 Growth of smart airports and connected ecosystems

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High implementation costs

- 3.3.2.2 Cybersecurity vulnerabilities

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Solution, 2021 - 2034 (USD million)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 (USD million)

- 6.1 Key trends

- 6.2 Supply chain & logistics

- 6.3 Airport & ground operations

- 6.4 Passenger experience & connectivity

- 6.5 Flight operations & fleet management

- 6.6 Aircraft health & predictive maintenance

- 6.7 Aircraft manufacturing & assembly

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD million)

- 7.1 Key trends

- 7.2 Airlines

- 7.3 Airports

- 7.4 Mro providers

- 7.5 Aircraft manufacturers

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Honeywell International Inc.

- 9.2 Siemens

- 9.3 General Electric Company

- 9.4 International Business Machines Corporation

- 9.5 Cisco Systems Inc.

- 9.6 SITA

- 9.7 Airbus

- 9.8 The Boeing Company

- 9.9 Thales

- 9.10 Lufthansa Technik

- 9.11 Collins Aerospace

- 9.12 Panasonic Avionics Corporation

- 9.13 SAP SE

- 9.14 Microsoft

- 9.15 Amadeus IT Group SA

- 9.16 Palantir Technologies

- 9.17 Tata Communications Limited