|

市場調査レポート

商品コード

1755219

シングルモード光ファイバーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Single-Mode Optical Fiber Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| シングルモード光ファイバーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月30日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

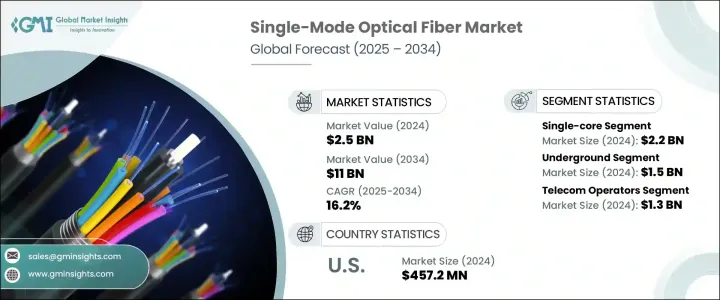

シングルモード光ファイバーの世界市場規模は、2024年に25億米ドルとなり、CAGR 16.2%で成長し、2034年には110億米ドルに達すると推定されています。

この急激な増加は、5Gネットワークの世界の導入と、クラウドコンピューティングとIoTの拡大によるデータトラフィックの爆発的な増加によって促進されています。ネットワーク・インフラがより高速で広いカバレッジを要求する中、通信事業者は、信号損失を最小限に抑えながら長距離のデータ伝送が可能なシングルモード・ファイバーに注目しています。次世代デジタル接続へのシフトは、スマートシティ、自律型システム、ハイパースケールデータセンターなど、帯域幅を必要とするアプリケーションが信頼性の高い大容量ファイバーネットワークに依存している業界全体の採用を促進しています。

特定の輸入品に対する関税など、過去の貿易制限は国内メーカーの競争力向上のために導入されたものであったが、その結果はまちまちでした。国内生産を支援する一方で、国際的なサプライチェーンを混乱させ、光ファイバの輸入コストを押し上げました。このため、光ファイバー・ネットワークの展開に遅れと不確実性が生じた。にもかかわらず、5Gネットワークの急速な展開は、基地局とデータセンター間のより高速で低遅延な接続を可能にするシングルモード光ファイバーの世界の需要の主要な原動力であることに変わりはないです。この技術は長距離、大容量のデータ伝送に適しているため、世界中のモバイルおよび固定ブロードバンドインフラの拡大に不可欠です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 25億米ドル |

| 予測金額 | 110億米ドル |

| CAGR | 16.2% |

シングルコアセグメントは、2024年に22億米ドルを生み出し、支配的なカテゴリーとなりました。この成長を支えているのは、主に既存の世界通信インフラとの幅広い互換性です。シングルコアSMFは、分散と減衰特性が低いため、長距離ネットワークやメトロネットワークに広く組み込まれています。通信プロバイダーがアップグレードを進める中、これらのファイバーは、レガシーシステムを交換する必要なく、高性能な拡張を可能にします。FTTHの導入ペースが速く、5G接続が拡大していることから、地域全体でエンドユーザーへの迅速かつ信頼性の高いサービス提供を可能にするシングルコア設計の役割がさらに強化されています。

地下展開セグメントは2024年に15億米ドルを生み出しました。密集した都市景観における隠蔽され保護されたインフラへのニーズが、地下設置への動向を引き続き後押ししています。都市開発とスマートシティ構想は、美観を維持し外部損傷から保護するため、通信事業者に地下ケーブルシステムの採用を促しています。このような導入は、各国のブロードバンド戦略にも合致しており、環境要因に耐えうる弾力性のある大容量インフラが求められています。地下ネットワークは、メトロや都市間のデータ伝送にますます不可欠になっており、データセンター、エンタープライズパーク、アクセスリングに信頼性の高いパフォーマンスを提供しています。

米国シングルモード光ファイバー市場は2024年に4億5,720万米ドルを生み出し、2034年まで成長すると予測されています。全国的な5G展開では、低遅延と高速データ転送をサポートするため、より大きなファイバーバックホール容量が求められています。連邦政府の資金援助イニシアティブは、ブロードバンド拡大に強い勢いを生み出し、高度な長距離光ファイバネットワークの需要を促進しています。ハイパースケールデータセンターインフラの成長により、さまざまな施設を結ぶ広帯域幅ファイバー接続の需要が増加し続けており、国内展開におけるシングルモードファイバーの採用をさらに後押ししています。

シングルモード光ファイバーの世界市場における主な業界企業には、コーニング、コムスコープ、プライスミアン、LSケーブル・アンド・システム、長江光ファイバ・ケーブル、住友電気工業、ヒューマネティックス、HTGD、ネクサンス、フジクラ、ビルラ古河、古河電工などがあります。シングルモード光ファイバー企業は、より強固な市場ポジションを確保するため、技術革新、コスト効率、地理的拡大を優先しています。多くの企業は、5G、FTTH、ハイパースケールデータネットワークなどの進化するアプリケーションに理想的な、減衰が少なく伝送容量の大きいファイバーを開発するために研究開発に多額の投資を行っています。通信事業者やインフラ・プロバイダーとの戦略的パートナーシップにより、各地域でより迅速な製品導入が可能になっています。メーカーはまた、リードタイムとロジスティクス・コストを削減するため、生産プロセスを最適化し、新興市場における施設のフットプリントを拡大しています。さらに、材料調達の多様化とサプライチェーンの強靭性強化も重要な戦略となっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 主要部品の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- クラウドサービスとIoTからのデータトラフィックの増加

- 5Gネットワークの世界展開

- FTTH(光ファイバー回線)の需要増加

- スマートシティとインフラプロジェクト

- 産業オートメーションとインダストリー4.0への移行

- 業界の潜在的リスク&課題

- 都市環境における複雑な設備

- 激しい市場競争と価格圧力

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:コア別、2021年~2034年

- 主要動向

- シングルコア

- デュアルコア

- マルチコア

第6章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- 地下

- 水中

- 電柱

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 政府/防衛

- 通信事業者

- クラウドプロバイダー

- 石油・ガス

- 産業オートメーション

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- AFL

- Birla Furukawa

- CommScope

- Corning Incorporated

- Exail

- Fujikura

- Furukawa

- HTGD

- Humanetics

- LS Cable &System

- Nexans

- Optical Cable Corporation

- Prysmian Group

- Sr. Indus Electro Systems Pvt. Ltd

- STL Tech

- Sumitomo Electric Industries, Ltd.

- Yangtze Optical Fiber &Cable

- ZTT

The Global Single-Mode Optical Fiber Market was valued at USD 2.5 billion in 2024 and is estimated to grow at a CAGR of 16.2% to reach USD 11 billion by 2034. This sharp increase is being fueled by the global implementation of 5G networks and the explosion of data traffic driven by cloud computing and IoT expansion. As network infrastructure demands faster speeds and broader coverage, telecom providers are turning to single-mode fibers for their ability to transmit data over extended distances with minimal signal loss. The shift toward next-gen digital connectivity is propelling adoption across industries, where bandwidth-intensive applications like smart cities, autonomous systems, and hyperscale data centers rely on reliable high-capacity fiber networks.

Past trade restrictions, such as tariffs on certain imports, were introduced to improve competitiveness for domestic manufacturers but had mixed results. While they supported local production, they also disrupted international supply chains and pushed up the cost of importing optical fibers. This led to delays and uncertainty in fiber network deployments. Despite this, the rapid rollout of 5G networks remains the key driver of global demand for single-mode optical fiber, enabling higher speed and lower latency connectivity between base stations and data centers. The technology's suitability for long-distance, high-volume data transmission makes it essential for expanding mobile and fixed broadband infrastructure worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 Billion |

| Forecast Value | $11 Billion |

| CAGR | 16.2% |

The single-core segment generated USD 2.2 billion in 2024, making it the dominant category. This growth is primarily supported by its broad compatibility with existing global telecom infrastructure. Single-core SMFs are widely integrated into long-distance and metro networks because of their low dispersion and attenuation characteristics. As telecom providers push forward with upgrades, these fibers enable high-performance expansion without the need for replacing legacy systems. The fast pace of FTTH deployment and growing 5G connectivity further reinforce the role of single-core designs in enabling rapid and reliable service delivery to end users across regions.

The underground deployment segment generated USD 1.5 billion in 2024. The need for concealed and protected infrastructure in dense urban landscapes continues to drive the trend toward underground installation. Urban development and smart city initiatives are encouraging telecom operators to adopt underground cable systems to maintain aesthetics and safeguard against external damage. These deployments also align with national broadband strategies in various countries, calling for resilient and high-capacity infrastructure capable of withstanding environmental factors. Underground networks are increasingly essential for metro and intercity data transport, offering reliable performance for data centers, enterprise parks, and access rings.

U.S. Single-Mode Optical Fiber Market generated USD 457.2 million in 2024 and is projected to grow through 2034. National 5G deployments are demanding greater fiber backhaul capacity to support low latency and high-speed data transfers. Federal funding initiatives have created strong momentum in broadband expansion, driving demand for advanced long-distance optical fiber networks. Growth in hyperscale data center infrastructure continues to increase demand for high-bandwidth fiber connections linking various facilities, further boosting single-mode fiber adoption in domestic deployments.

Key industry players in the Global Single-Mode Optical Fiber Market include Corning, CommScope, Prysmian, LS Cable and System, Yangtze Optical Fiber and Cable, Sumitomo Electric, Humanetics, HTGD, Nexans, Fujikura, Birla Furukawa, and Furukawa. To secure a stronger market position, single-mode optical fiber companies are prioritizing innovation, cost efficiency, and geographic expansion. Many are heavily investing in R&D to develop fibers with lower attenuation and higher transmission capacity, making them ideal for evolving applications like 5G, FTTH, and hyperscale data networks. Strategic partnerships with telecom operators and infrastructure providers are enabling faster product adoption across regions. Manufacturers are also optimizing production processes and expanding facility footprints in emerging markets to reduce lead times and logistics costs. In addition, diversification of material sourcing and strengthening supply chain resilience have become crucial strategies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing data traffic from cloud services & IoT

- 3.3.1.2 Global rollout of 5G network

- 3.3.1.3 Growing demand for FTTH (fiber to the home)

- 3.3.1.4 Smart city and infrastructure projects

- 3.3.1.5 Shift towards industrial automation and industry 4.0

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Complex installation in urban environments

- 3.3.2.2 Intense market competition and price pressure

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Core, 2021 – 2034 (USD Million & Megameter)

- 5.1 Key trends

- 5.2 Single-core

- 5.3 Dual-core

- 5.4 Multi-core

Chapter 6 Market Estimates and Forecast, By Deployment, 2021 – 2034 (USD Million & Megameter)

- 6.1 Key trends

- 6.2 Underground

- 6.3 Underwater

- 6.4 Utility poles

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Million & Megameter)

- 7.1 Key trends

- 7.2 Government/defense

- 7.3 Telecom operators

- 7.4 Cloud providers

- 7.5 Oil & gas

- 7.6 Industrial automation

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Megameter)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AFL

- 9.2 Birla Furukawa

- 9.3 CommScope

- 9.4 Corning Incorporated

- 9.5 Exail

- 9.6 Fujikura

- 9.7 Furukawa

- 9.8 HTGD

- 9.9 Humanetics

- 9.10 LS Cable & System

- 9.11 Nexans

- 9.12 Optical Cable Corporation

- 9.13 Prysmian Group

- 9.14 Sr. Indus Electro Systems Pvt. Ltd

- 9.15 STL Tech

- 9.16 Sumitomo Electric Industries, Ltd.

- 9.17 Yangtze Optical Fiber & Cable

- 9.18 ZTT